How do i collect unpaid invoices: 7 Proven Steps (2026)

Why Collecting Unpaid Invoices Feels So Uncomfortable (And Why You Need to Get Over It)

I’ll be honest with you. The first time I had to chase down a client for an overdue payment, my palms were sweating. I kept rehearsing what I’d say, worried I’d sound desperate or ruin the relationship. That uncomfortable feeling in your stomach when you need to ask for money you’ve already earned? I know it well, and if you’re reading this, you probably do too.

Collecting unpaid invoices often feels uncomfortable because we’ve been culturally conditioned to avoid talking about money. We worry we’ll come across as pushy, greedy, or difficult to work with. But here’s the truth I had to learn the hard way: asking to be paid for work you’ve already completed isn’t begging. It’s business.

I remember talking to Annie, a service business owner who put it perfectly. She told me she had to shift her entire mindset. “I’m a service professional, not a beggar,” she said. “I expect to be paid for work already completed.” That one statement changed how I approached invoice collection forever. You’re not asking for a favor. You’re not being unreasonable. You delivered value, and payment is the agreed-upon exchange.

The real problem is that many of us think following up on late payments will damage our business relationship with the client. Marc, a voice actor I spoke with, deals with this all the time. He told me, “Don’t be afraid to approach a client about late payment. Thinking that following up will lose you a client is a mindset issue that hinders business growth.” He’s maintained a near-perfect payment record for years, and it’s not because he avoids difficult conversations. It’s because he handles them professionally.

When you don’t follow up on unpaid invoices, you’re actually teaching clients that your time and expertise have no real value. You’re sending the message that deadlines are optional and that you’re willing to work for free. No successful business operates that way.

The clients worth keeping will respect you for being professional about payment. They’ll appreciate clear communication and won’t think less of you for expecting what you’re owed. The ones who get angry or dismissive when you ask for payment? Those are the clients you don’t want anyway.

Think about it this way. If you hired a plumber to fix your sink, you’d pay them when the work was done. If they sent you a polite reminder that payment was due, you wouldn’t think they were being pushy. You’d probably apologize for forgetting and pay immediately. Your clients should treat you with the same respect.

Following up on unpaid invoices is not about being confrontational. It’s about maintaining professional standards and protecting your business. The strategies I’m about to share with you work because they’re respectful, systematic, and proven. They help you get paid while preserving the business relationship, assuming the client is worth preserving in the first place.

So before we dive into the step-by-step system for how to collect unpaid invoices, I need you to commit to one mindset shift. You are a professional. Your work has value. Getting paid on time is not a favor your clients grant you. It’s a fundamental part of the agreement you both entered into. Once you internalize that, the actual invoice collection process becomes much easier to execute.

Let’s get you paid.

The Real Cost of Unpaid Invoices (Why This Isn’t Just Annoying It’s Dangerous)

Unpaid invoices aren’t just a minor inconvenience. They’re a serious threat to your business survival. Most business owners understand intellectually that late payments cause problems, but until you experience the cascade of consequences yourself, you don’t realize how quickly unpaid invoices can destabilize everything you’ve built.

Let me put this in perspective with a number that should concern you. Nearly 50 percent of U.S. business invoices are currently overdue. That’s not a small percentage of struggling companies. That’s almost half of all invoices across the country sitting unpaid right now. If you’re wondering how to collect unpaid invoices, you’re dealing with something that affects millions of business owners simultaneously.

The damage extends far beyond just the money sitting in limbo. When a client doesn’t pay on time, your cash flow takes a hit. Cash flow is the lifeblood of any business. It’s what lets you pay your own bills, cover payroll, purchase inventory, and invest in growth. I watched this play out directly with Annie, who runs a service business. She told me that before she had employees, unpaid invoices were frustrating but manageable. Then she brought two people onto her payroll. Suddenly, late payments from clients became a crisis because she couldn’t pay her team if her clients weren’t paying her. Her employees still expected their paychecks on Friday, regardless of whether a client’s check had arrived.

When accounts receivable backs up, you’re essentially financing your client’s business with your own cash. You’re the one covering the gap between when you deliver the service and when you finally get paid. That’s capital that could be working for you, and instead it’s sitting in someone else’s pocket.

There’s another cost that people rarely discuss openly. The time you spend chasing overdue payments is time you’re not spending on growth, strategy, or meaningful work. You’re not writing, creating, selling, or building. You’re sending reminder emails, making phone calls, and managing spreadsheets of delinquent accounts. That’s wasted energy that drains your motivation.

I talked with Sarah, an accountant who works with small businesses, and she shared something that stuck with me. “The longer an invoice remains unpaid, the harder it becomes to collect,” she said. “Failing to collect means you worked for free.” Think about that for a moment. If you deliver a thousand dollars worth of work and never collect payment, you just gave away a thousand dollars. Your business doesn’t magically absorb that loss. You absorb it.

The psychological cost matters too. Unpaid invoices create stress and uncertainty. You’re checking your bank account wondering if payment will arrive. You’re second-guessing the client’s intentions. You’re worried about confrontation. That mental load affects your ability to do good work for clients who do pay on time.

Accounts receivable management directly impacts how your business functions financially. The longer invoices sit unpaid, the worse your receivables turnover becomes, which makes your business look less healthy to lenders, investors, or anyone evaluating your financial performance. It also means your actual profit margin is much lower than it appears because the money isn’t in your bank account where you can use it.

Here’s what I want you to understand. Unpaid invoices aren’t just about the money you’re owed. They’re about cash flow problems that force difficult decisions, time wasted on collection instead of growth, stress that affects your wellbeing, and a business that’s always financially uncertain. Collecting unpaid invoices quickly isn’t about being demanding or difficult.

It’s about protecting your business’s survival and your ability to invest in your future. The good news is that once you implement a proper system for how to collect unpaid invoices, most of these problems disappear. But you have to take action now, because every day an invoice sits unpaid makes recovery harder.

When Your Customer Isn’t Paying: What’s Really Happening on Their End

Most of the time, a customer not paying your invoice isn’t personal or malicious. They’re likely caught in a process you can’t see, and understanding what’s actually happening on their end changes how you approach collection.

Here’s something that shifted my entire perspective on unpaid invoices. I used to assume that if someone didn’t pay, they were avoiding me or didn’t value my work. Then I learned what actually happens inside a client’s organization when your invoice arrives. The reality is far more mundane, and honestly, a lot more forgivable once you understand it.

Think about it from the client’s perspective for a moment. When your invoice lands in their inbox, it doesn’t immediately turn into a check. Especially if they’re a larger company, your invoice enters a complex approval workflow. It gets verified against the original purchase order you agreed on. Someone checks that the quantity and pricing match what was actually delivered. In some cases, the client’s receiving department has to confirm they actually got what you sent before finance will approve payment.

This accounts payable process on the client’s side isn’t designed to delay you. It’s designed to protect them from fraud and overpayment. But it means your invoice doesn’t move directly from email to the payment queue. It bounces around different departments. The accounts payable manager might be waiting for approval from a department head. That department head might be in meetings. The payment deadline you’re expecting might come and go while your invoice is still waiting for a signature.

I spoke with someone who works in corporate accounts payable processing, and they explained something called two-way and three-way matching. Two-way matching means the client compares your invoice against the purchase order to make sure everything matches. Three-way matching adds one more step: they also compare both of those against their receipt of goods to confirm they actually received what they paid for. These aren’t steps a client takes because they’re being difficult. They’re standard business practice for managing cash and preventing errors.

One of the most common reasons a customer isn’t paying your invoice is simply that they forgot about it or it got lost in their email. The invoice landed in their inbox among hundreds of other emails that day. Someone meant to process it but got distracted. The email got flagged for later and buried under new messages. It happens constantly.

Marc, who has maintained nearly perfect payment records with his clients, reminded me of something important. “Rule number one,” he said, “never assume a client is trying to screw you. People get busy, invoices get lost, checks are already in the mail.” Most of the time, that’s the reality. Your client isn’t plotting to avoid payment. They’re just overwhelmed.

The Innocent Reasons Payments Get Delayed

The majority of late payments happen for reasons that have nothing to do with you or your work quality.

Your invoice might have landed in the client’s spam folder. I can’t tell you how many times this happens. You send the invoice, they never see it, and you’re both confused about why payment hasn’t arrived. Their contact information changed. The person who normally handles payments left the company. Your email address ended up on a distribution list that filters to a folder they don’t check daily.

They’re genuinely waiting for internal approval. The payment deadline you expected might have come and gone while someone’s signature was stuck in an approval queue. The client’s finance manager might be on vacation. Their system might require three approvals for invoices over a certain amount, and one of those approvers is slammed.

Payment follow up becomes necessary not because the client is avoiding you, but because your invoice is stuck in a legitimate process. When you send that first reminder, you’re not being pushy. You’re reminding them that the invoice exists and needs attention. Most of the time, that reminder is all it takes. The client realizes they missed it, locates it in their system, and processes payment immediately.

The invoice due date you set is real in your mind, but it might not have registered on their end. Maybe they interpreted your terms differently. Maybe they thought they had thirty days from when they received the goods, not from the invoice date. These are simple misunderstandings that a gentle reminder clears up.

The Problem Reasons (That You Can Still Fix)

Sometimes the delay is due to legitimate issues on the client’s side that they should have communicated but haven’t.

The client has cash flow problems. This isn’t your fault, but it affects you. They genuinely want to pay, but they’re waiting for their own clients to pay them. Their business is tight right now. In these situations, you have options. You can offer a payment plan. You can work with them. This is a problem you can address with a conversation.

They’re dissatisfied with your work but haven’t said anything. This is frustrating because you had no opportunity to fix it. They’re holding payment until they feel comfortable accepting the deliverable. Here’s where a direct question helps. Ask them if there’s something they’re not happy about. Give them a chance to communicate. Many times, the issue is small and fixable. Once you resolve it, they pay immediately.

A payment dispute creates a standoff where both sides are waiting for the other to move. The client thinks you delivered something different from what they paid for. You think you delivered exactly what was agreed. This is exactly why having a clear statement of work before the project starts is so important — it gives both sides a written reference point to return to. Rather than arguing, suggest a conversation or mediation. These problems are usually resolvable when both parties actually talk.

The Red Flag Reasons (Intentional Non-Payment)

Not every late payment situation is fixable, and you need to recognize when you’re dealing with someone who isn’t playing by the rules.

Some clients are chronic non-payers. They delay payment on purpose, using your invoice as free financing. They’re betting you won’t pursue collection aggressively because it’s not worth your time. These clients often have a pattern of late payments across multiple vendors. If you’re dealing with someone like this, don’t work with them again.

Then there are the outright scammers. These are the clients trying to get your services for free. They might dispute the invoice falsely. They might ignore you completely, hoping you’ll eventually give up. They might claim they never received the services even though they did. These are rare, but they happen.

Sometimes a client’s business is failing. They’re heading toward bankruptcy. In that situation, even if they want to pay, they might not be able to. You might never collect that invoice regardless of how hard you chase it. It’s not about your work. It’s about their business’s viability.

The key is distinguishing between the innocent delays and the real problems early on. That’s why starting with empathy and assuming good intent works. Most of the time, you’ll be right, and a simple reminder fixes everything. When you’re wrong and dealing with a legitimate problem or red flag, you’ll discover it during your follow-up conversations. Then you can respond appropriately.

The Collection Timeline: Exactly When to Do What (Day-by-Day)

The biggest mistake most business owners make is waiting too long to follow up on unpaid invoices. Without a clear collection timeline, you might send one reminder and then do nothing for weeks. Or you might follow up constantly and seem desperate. What separates business owners who successfully collect unpaid invoices from those who struggle is a systematic approach that removes guesswork and emotion from the process.

I discovered something powerful when I learned about the “dunning process” from someone who studies payment behavior. The dunning process is the series of reminders and escalations you use to collect overdue payments. The most effective dunning process isn’t aggressive. It’s consistent and methodical. When you follow a clear timeline, you remove the guesswork and emotion from collection.

Here’s the number that should grab your attention. Research consistently shows that implementing a structured collection timeline decreases late payments significantly and reduces the need for formal collections by more than two-thirds. That’s not a small improvement. That’s a transformation in how quickly you get paid.

The timeline I’m about to share removes the uncertainty. You’ll know exactly what day to send which message. You won’t wonder if you’re being too pushy or not pushy enough. You’ll just follow the system.

Day -2 to Day 0 (Before Payment Is Due)

Start your payment reminder before the due date arrives. Most clients will pay on time if you simply remind them the payment deadline is approaching.

Send a friendly payment reminder two days before the invoice due date. This isn’t a demand. It’s a helpful nudge that says, “Hey, just so you have it on your radar, payment is due in two days.” This approach works because you’re giving the client time to arrange payment before they slip into being late.

Marc, who maintains nearly perfect payment records with his clients, explained that most people are simply busy. They’re juggling multiple priorities. A courteous advance reminder helps them prioritize your invoice before other urgent items demand their attention. This single message catches many potential late payments before they happen.

Day 1-7 (Just Past Due)

If payment hasn’t arrived by day one past due, send your first polite reminder immediately. Most of the time, this single message resolves the issue.

This is where consistency matters. Don’t wait five days hoping the check arrives. Don’t assume they’re being difficult. Send a friendly email that reminds them the payment deadline has passed and asks if they need anything from you. Attach the original invoice so they don’t have to search for it.

In my experience working with business owners on collections, roughly 90 percent of the time, this first reminder is all it takes to get payment. The client realizes they missed the deadline, locates the invoice, and processes it immediately. They weren’t avoiding you. They just needed the reminder.

Day 7-14 (Getting Serious)

If you haven’t received payment by day seven, it’s time to escalate from email to a phone call.

Email is easy to ignore. A phone conversation is harder to avoid. Call during their business hours and ask politely if they received your invoice and if there’s anything preventing payment. Be prepared for the answer. Maybe they didn’t get the email. Maybe they have a question about the invoice. Maybe there’s a legitimate reason for the delay.

This is still in the friendly zone. You’re not threatening anything yet. You’re just making personal contact and opening a dialogue. Many times, this conversation surfaces a small problem that’s easy to fix, and payment follows quickly.

Day 14-30 (Escalation Zone)

By day fourteen, your tone shifts from friendly to formal. Send a written notice that clearly states the invoice is past due and that late fees will be applied if payment isn’t received by a specific date.

This is when you mention that a late fee will be charged if payment doesn’t arrive. Be specific about the fee amount and the deadline. This isn’t being harsh. It’s being professional. Late fees are standard business practice. They motivate faster payment and compensate you for the time your money is tied up.

Include the invoice clearly in this communication. Make it impossible for them to say they can’t find it or don’t understand what’s owed. State the exact amount and the exact due date for payment to avoid the late fee.

Day 30-60 (Final Internal Efforts)

At this point, you’ve given the client multiple opportunities to pay. Now it’s time to consider offering a payment plan or sending a final notice before external collection.

If the client hasn’t responded to multiple reminders and phone calls, ask directly if there’s a problem you can solve. Maybe they’re having cash flow issues. Maybe they’re dissatisfied with your work and didn’t want to say so. Offer a payment plan that works for their situation. Often, a client will accept a plan when faced with the alternative of having their debt sent to a collection agency or to small claims court.

If they don’t respond to this offer or if they’ve indicated they simply won’t pay, send a final notice. State clearly that you’re about to escalate this to external collection or legal action if payment isn’t received by a specific date. This is your last chance to resolve it internally before things get serious.

Day 60-90+ (External Options)

If internal efforts haven’t worked by day sixty, it’s time to involve outside help. You can send the debt to a collection agency, file in small claims court, or pursue other legal remedies depending on the amount and your location.

At this stage, you’ve done everything reasonable as a business owner. The client has had ninety days to pay or communicate about the problem. They’ve received multiple reminders and escalations. You’ve offered solutions. If they still haven’t paid, they’re not going to voluntarily.

A collection agency takes over from here and handles further collection efforts. You stop chasing and let professionals handle it. This removes the emotional burden and usually results in payment within weeks or months.

Following this collection timeline removes the emotional guesswork and gives you a clear action plan. You’re not being too harsh or too lenient. You’re being systematically professional. Most invoices get paid during the first two stages. Those that don’t move through the remaining stages until resolution.

Step 1: Send Your First Payment Reminder (Day 1-7)

Your first payment reminder is the single most important step you can take, and it works about 90 percent of the time. This is where most unpaid invoices get resolved. You don’t need aggressive tactics or legal threats. You just need to send a professional, friendly reminder that reminds your client the payment is due.

The key is timing and tone. You want to send this reminder on day one or day two after the payment deadline passes. Don’t wait a week thinking they’ll figure it out on their own. Don’t assume they’re being difficult. Just send the reminder assuming they forgot or missed the email.

Accounting professionals consistently point out that the single best practice for avoiding unpaid invoices is to send reminders consistently and automatically. Business owners who use software to automate their payment reminders report significantly lower rates of overdue invoices compared to those who handle reminders manually. This automation works because consistency and timing are powerful behavioral motivators.

The reason your first payment reminder works so well is that most clients genuinely just forgot. They’re busy. Your invoice landed in their inbox among a hundred other emails that day. They meant to process it but got distracted. Someone at their company was supposed to handle it but never got the message. Your reminder brings the invoice back to the top of their priority list at exactly the right moment.

The tone of your reminder matters enormously. You want to be helpful, not accusatory. You’re not saying, “You didn’t pay me.” You’re saying, “I want to make sure you have everything you need to process this payment.” That subtle difference changes how the client receives your message.

Always attach the original invoice as a PDF to your reminder email. Don’t make your client search for it. Don’t assume they saved the first email. Include the invoice in your reminder so they can process payment immediately without having to dig through their email or filing system. Removing friction from the payment process matters more than you’d think.

Friendly Reminder Email Template (Copy and Paste)

Use this template as your payment reminder. Customize it with your specific details, but keep the tone and structure the same. Copy the entire email, fill in the bracketed sections with your information, and send it.

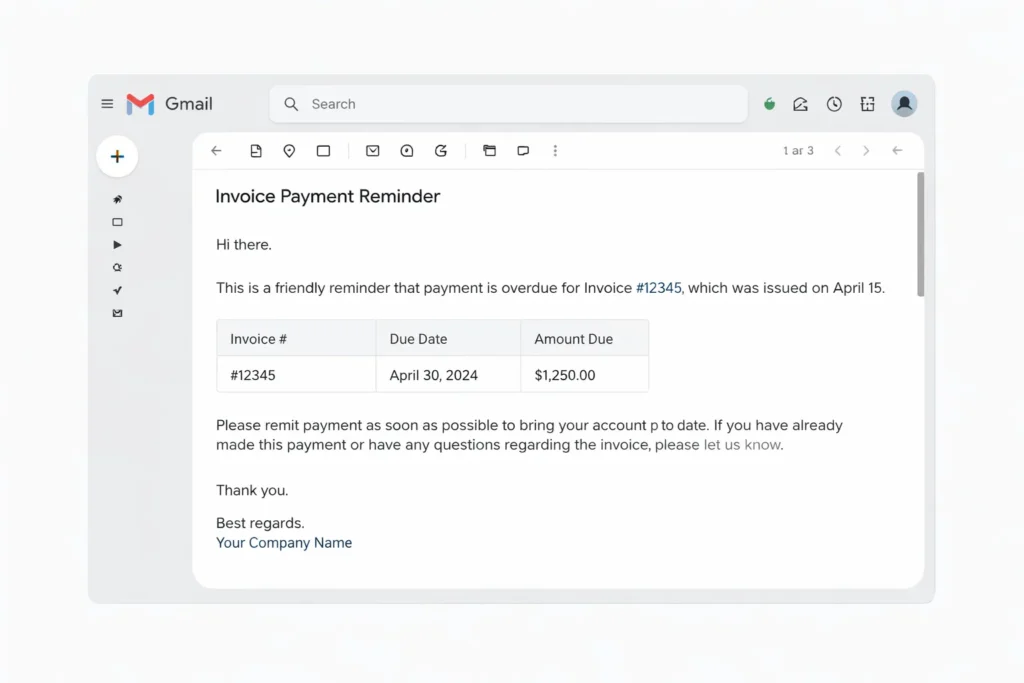

Subject: Friendly Reminder: Invoice [Invoice Number] Now Due

Hi [Client Name],

I hope you’re doing well. I wanted to reach out with a friendly reminder that invoice [Invoice Number] is now due for payment.

Here are the details:

Invoice Number: [Invoice Number]

Invoice Date: [Invoice Date]

Amount Due: [Amount]

Due Date: [Due Date]

I’ve attached a copy of the invoice to this email so you have all the information in one place.

You can process payment using any of these methods:

- Direct bank transfer to [your bank details]

- Credit card payment at [your payment portal/link]

- Check mailed to [your mailing address]

- PayPal to [your PayPal email]

If you have any questions about this invoice or if there’s anything preventing payment, please let me know. I’m happy to help clarify anything.

Thank you for your business, and I appreciate your prompt payment.

Best regards,

[Your Name]

[Your Business Name]

[Your Contact Information]

Why this template works:

It’s friendly and assumes good intent. It includes all the necessary information without forcing the client to search. It offers multiple payment methods so cost or technical barriers don’t prevent payment. It explicitly invites them to reach out if there’s a problem. It closes on a positive note that preserves the business relationship.

Send this reminder via email, not text or phone call. Email creates a written record. It gives the client time to process the reminder and take action without feeling pressured by a real-time conversation. It’s also easier for them to forward to the right department in their organization if they need approval.

If you’re managing multiple clients, automate this. Use accounting software like QuickBooks or Wave to send automatic reminders on day one and day three past due. Automation removes the emotional burden of following up. It also ensures you never forget to send a reminder because the system handles it for you.

Most of the time, your client will respond to this first reminder within two or three days. They’ll either send payment or reach out with an explanation. Either way, you’ve moved forward. You’ve established that you take payment seriously, and you’ve given them a clear, easy way to pay.

If they don’t respond within a week, move to step two and make a phone call. But honestly, you probably won’t need to. This friendly reminder does the job the vast majority of the time.

Step 2: The Phone Call That Gets Results (Day 7-14)

If your email reminder didn’t produce payment after a week, it’s time to pick up the phone. A voice-to-voice conversation has power that email doesn’t. It’s harder to ignore a real person calling than it is to delete an email. It also gives you a chance to uncover what’s really going on and solve problems that email can’t address.

I was hesitant about making collection calls at first. I worried I’d sound pushy or desperate. But I learned that a professional phone call handled correctly almost always gets a response. The client either tells you they’ll pay immediately, or they tell you what’s preventing payment. Either way, you move forward.

The phone call is also where you can adjust your approach based on what you learn. Maybe the client is upset with your work. Maybe they have a legitimate cash flow problem. Maybe the invoice got lost and they didn’t even know about it. You can’t discover these things through email. You need a conversation.

Payment follow up through phone calls works because it forces a real-time interaction where avoidance becomes difficult. When you call, the client has to actively decide whether to engage or hang up. Most of the time, they’ll engage. And once you’re talking, you have a chance to resolve the issue.

When to Call (Timing Matters)

Timing your phone call dramatically increases your chances of reaching the decision-maker. Don’t call during the middle of the business day when they’re buried in meetings and other responsibilities.

Call before regular business hours or after them. Try calling at 8 a.m. or 5 p.m. When people aren’t in the full chaos of their day, they’re more accessible and more willing to take an unscheduled call. They’re also more likely to have a genuine conversation instead of rushing you off the phone.

If you call during peak business hours, you’re competing with a hundred other things demanding their attention. They’re mentally scattered. They’re thinking about the meeting that just ended or the one coming next. But catch them at 7:45 a.m. or 4:45 p.m., and they’re often in a better headspace for an actual conversation.

Avoid calling on Monday mornings when everyone is drowning in weekend backlog, and avoid Friday afternoons when people are checked out. Tuesday through Thursday mid-morning or early afternoon works reasonably well if off-hours don’t work for your schedule.

How to Get Past the Gatekeeper

The receptionist or administrative assistant is your ally, not your obstacle. They control access to the decision-maker, but they’re not trying to block you. They’re just doing their job.

When you reach the receptionist, be friendly and respectful. Don’t demand to speak to the person who owes you money. Instead, ask for their help. Say something like, “Hi, I need to reach [Name] about a payment matter. I really need to speak with them. Do you know when they might be available or the best time to call back?”

You’ve just done something clever. You’ve made the receptionist your ally instead of your adversary. You’ve acknowledged that they have information you need and asked for their advice. Most receptionists will help you if you treat them with respect and make their job easier.

If the person isn’t available, ask the receptionist when they typically return or when they’re usually in the office. Ask if you should call back at a specific time. Get their name and use it next time you call. Building a relationship with the receptionist means they’ll actually help you reach the person instead of screening you out.

When you call back, greet the receptionist by name and say something like, “Hi [Name], it’s [Your Name] again. Is [Decision-Maker] available now?” The receptionist remembers you. They appreciate that you remembered them. They’re much more likely to put you through.

Phone Script for Collecting Payment

Here’s exactly what to say when you reach your customer. This script is friendly and professional. It assumes good intent and gives them an easy way to acknowledge the issue and move toward payment.

Opening

“Hi [Name], this is [Your Name] from [Your Company]. Do you have a quick minute to talk? I wanted to reach out about invoice [Invoice Number] for [Amount]. The payment was due on [Due Date], and I wanted to check in and see if there’s anything I can help with.”

Listen to their response. They’ll probably say one of three things. They forgot. Something’s wrong. Or they’ll make an excuse.

If they say they forgot:

“No problem, it happens all the time. You’re busy. I just wanted to make sure it was on your radar. Can I help you process that payment today? I’ve got the invoice details right here.”

Then provide the payment methods and make it easy for them to pay immediately.

If something’s wrong (missing invoice, question about the work, billing dispute):

“Got it. I totally understand. Here’s what I can do. I can [resend the invoice/answer your question/clarify the billing]. Once that’s cleared up, we’ll get payment processed. When would be a good time to follow up?”

If they’re avoiding the issue or not committing to payment:

Here’s where the psychological question from professional negotiators comes in. Ask this calmly and genuinely:

“Is there something I should know about? Is there a problem with the service, or is something preventing payment right now?”

This question forces them to respond honestly. They either admit there’s a problem you can solve, or they have to admit there isn’t a problem, which means payment should happen. Either way, you’ve moved the conversation forward.

Another powerful question if you sense dissatisfaction:

“Is there something about the work that you’re not completely happy with?”

This opens the door for them to voice concerns without you being accusatory. Often, clients are withholding payment because they’re unhappy but didn’t want to say so. Once they voice the concern, you can address it.

Closing

“Okay, so here’s what I’m hearing. [Summarize what they said]. Here’s what I need from you. I need payment by [specific date]. Can you commit to that?”

Make them commit to a specific date. Don’t accept vague promises like “soon” or “next week.” Get a date.

End the call:

“Perfect. I’ll send you a follow-up email confirming what we discussed. Thank you for taking the time to talk with me, and I appreciate your business.”

The power of this script is that it stays friendly and professional while moving toward a solution. You’re not threatening. You’re not angry. You’re being a professional who needs to collect a payment they owe you. Most clients respect that approach.

The psychological questions work because they create pressure without aggression. The client can’t just ignore you or hide. They have to engage with the question and either admit there’s a problem or admit there isn’t one. Both paths lead to payment.

After this phone call, most customers either pay within a few days or commit to a specific payment date. If they commit to a date and miss it, you escalate to the next step. But usually, the personal connection made during a phone call is enough to get payment moving.

Step 3: The $4,000 Question That Got Paid in 10 Minutes

Sometimes a single question changes everything. I learned about a technique from professional negotiators that sounds almost too simple to work, but it has an extraordinary track record for breaking through client avoidance and getting payment moving.

The technique comes from the book “Never Split the Difference” by Chris Voss, a former FBI hostage negotiator. Voss discovered that certain questions create psychological pressure that makes it nearly impossible for someone to ignore you or continue avoiding a conversation. The pressure isn’t aggressive or threatening. It’s just uncomfortable enough that the other person has to respond honestly.

A service business owner named Annie Yang used these negotiation questions to collect payments that had been stuck for months. Her results shocked me when I first heard them. One client owed her a thousand dollars for five months without responding to any standard reminders. She asked one specific question, and suddenly the client wrote five paragraphs explaining what was really going on. They resolved the underlying issue, and payment came through immediately.

Even more impressive was another client who owed her four thousand dollars and had completely stopped responding to anything. This wasn’t a communication problem. This was someone actively avoiding her. She asked the right question, and the client responded with a direct deposit payment within ten minutes.

These psychological questions work because they force the client to make a choice, and both choices lead to payment. They can either admit there’s a problem you can solve, or they have to admit there isn’t a problem, which means they should pay. There’s no middle ground. There’s no way to stay silent.

Question #1: “Is There Something You’re Not Happy About?”

Use this question when a client has been silent for a long time and you suspect they might be dissatisfied with your work but haven’t said anything.

Here’s exactly how to ask it. Don’t soften it. Don’t add extra explanation. Just ask: “Is there something about the work that you’re not happy about that you’re not communicating to me?”

The power of this question is that it directly invites them to complain. You’re giving them permission to tell you what’s wrong. Most clients who are unhappy with your work don’t want to start a fight. They just want to avoid the confrontation. So they ghost you instead. This question removes that option.

When you ask this question, you’re signaling that you’re willing to listen and fix whatever’s wrong. You’re not being defensive. You’re being solution-oriented. The client suddenly has a path forward. They can tell you what the problem is, and you can work together to resolve it.

The beauty of this question is that if there actually is a problem, you now know what it is and can fix it. If there isn’t a problem, the client has to admit that, which means the conversation shifts immediately to “so when can we get payment processed?”

Annie’s thousand-dollar case played out exactly this way. She asked the question. The client admitted they weren’t fully satisfied with part of the deliverable. Annie offered to revise it. The client accepted. Payment happened. The relationship survived and even strengthened because Annie was willing to fix the problem instead of just demanding money.

When you ask this question on a phone call or in an email, pause and wait for their response. Don’t fill the silence. Silence is uncomfortable, and uncomfortable silence often produces honest answers. That moment of discomfort forces them to actually think about the question instead of giving you an automatic deflection.

Question #2: “Did I Offend You?”

Use this question when a client is chronically avoiding you and you’ve exhausted standard collection attempts. This question works especially well with clients who ignore emails, avoid phone calls, and seem to have completely shut you out.

Ask it this way: “Is there something I said or did that offended you?”

This question reframes non-payment as a personal issue rather than a financial one. It shifts the conversation from “you owe me money” to “did I hurt you somehow?” The client’s defenses drop because you’re not attacking them about the debt. You’re asking about your own behavior.

Most chronic avoiders aren’t avoiding because of the money. They’re avoiding because they’re uncomfortable or annoyed about something. Maybe your communication style bothered them. Maybe you said something that came across wrong. Maybe they had a bad experience and couldn’t face telling you. This question opens the door for them to tell you what’s really going on.

Here’s what happened with Annie’s four-thousand-dollar client. This person had completely ghosted her. No response to anything. She asked if she’d offended them. The client immediately responded and sent payment within ten minutes. The client had felt hurt about something, and once Annie acknowledged that possibility, the barrier dissolved.

When you ask this question, you’re showing emotional intelligence and vulnerability. You’re saying, “I know something’s wrong, and I’m willing to look at my own role in it.” That’s powerful. It disarms people. It makes them want to engage with you instead of hide from you.

The question works because it removes blame and opens a space for honesty. The client no longer feels attacked. They feel heard. And once someone feels heard, they’re usually willing to move forward toward payment.

Use both of these questions strategically. Save them for situations where standard collection methods haven’t worked. They’re too powerful to waste on routine follow-ups. But when you’re stuck with a client who’s completely checked out, these questions often unlock the situation in minutes.

The reason these questions work is rooted in psychology. They create what’s called a “black mirror” moment where the client has to see themselves and their behavior clearly. They can’t hide behind avoidance anymore. They have to engage. And engagement, in almost every case, leads to payment.

This formal notice should clearly state the following consequences:

Step 4: Formal Past Due Notice and Late Fees (Day 14-30)

By day fourteen, your tone needs to shift from friendly to formal. You’ve given the client multiple chances to pay. You’ve sent a polite reminder. You’ve made a phone call. You’ve tried to understand what’s going on. Now it’s time to make clear that this is serious, and there will be consequences if payment doesn’t arrive soon.

- Additional late fees will be applied at [Late Fee Rate] per day/week/month

- This debt will be referred to a collection agency, which will negatively impact your credit report

- Legal action may be pursued to recover the full amount owed plus court costs and attorney fees

This is where many business owners hesitate. They worry that charging late fees will make them look greedy or damage the relationship further. But here’s the reality: late fees are standard business practice. Your utility company charges them. Your credit card company charges them. Your internet provider charges them. Charging a late fee isn’t unusual or unreasonable. It’s actually expected in professional business relationships.

Late fees serve two purposes. First, they compensate you for the time your money is tied up and the cost of collection efforts. Second, they create financial motivation for the client to prioritize your payment over other bills. A client might ignore a past-due invoice without consequences, but once a late fee kicks in, suddenly paying you becomes more urgent.

The key is establishing late fee language in your original agreement before any invoice ever goes out. If you didn’t do that initially, you can still add late fees to current overdue invoices, but it’s stronger if it was already in your terms. Going forward, include late payment penalty language in every contract and invoice you send.

I recommend stating late fees clearly and specifically. Don’t be vague. Say something like “A late fee of 1.5 percent per month will be applied to all invoices not paid within thirty days of the invoice date” or “Late payments will incur a penalty fee of ten percent after fourteen days.” Be specific about the amount and the trigger date.

Past Due Invoice Email Template (Formal Tone)

This template is stronger than your initial friendly reminder. The language is direct and professional. You’re no longer assuming oversight. You’re stating facts and outlining consequences.

Subject: URGENT: Past Due Invoice [Invoice Number] – Action Required

Dear [Client Name],

I am writing to formally notify you that invoice [Invoice Number] for [Amount Due] remains unpaid as of [Current Date], which is [number] days past the due date of [Original Due Date].

Despite previous reminders sent on [dates of previous reminders], payment has not been received. This matter requires immediate attention.

Invoice Details:

Invoice Number: [Invoice Number]

Original Amount Due: [Amount]

Amount Due With Late Fees: [Original Amount + Late Fee Amount]

Original Due Date: [Original Due Date]

Current Status: [Number] Days Past Due

Next Steps:

Payment must be received by [Specific Date, typically 5-7 days from now]. If payment is not received by this date, the following will occur:

- Additional late fees will be applied at [Late Fee Rate] per day/week/month

- This debt will be referred to a collection agency, which will negatively impact your credit report

- Legal action may be pursued to recover the full amount owed plus court costs and attorney fees

How to Pay:

Please process payment immediately using one of these methods:

[List all payment methods]

If there are extenuating circumstances preventing payment or if you dispute this invoice, you must contact me within 48 hours to discuss a resolution. Without communication, collection proceedings will move forward.

I value our business relationship and prefer to resolve this matter directly. However, I cannot allow this invoice to remain unpaid indefinitely.

Please confirm receipt of this notice and your commitment to payment by [Specific Date].

Sincerely,

[Your Name]

[Your Business Name]

[Contact Information]

This template is firm but professional. You’re not threatening. You’re stating business facts. You’re giving them one more clear deadline with real consequences outlined. Most clients respond to this email by either paying or reaching out to discuss a payment plan.

Should You Charge Late Fees?

Yes, you should charge late fees, and you should include them in your original contract before any invoice goes out. Late fees are not optional extras. They’re a standard business protection.

Late fees have two effects. First, they remind the client that delaying payment has a cost. This creates urgency. A client ignoring a standard past-due notice might suddenly prioritize your invoice once they realize a late fee will compound the amount owed. Second, late fees compensate you for the real costs of late payment, including the time you spend chasing the invoice and the cost of borrowing money to cover your own expenses while waiting for payment.

How much should you charge? Industry standard late fees typically range from 1 to 2 percent per month or between 10 and 15 percent of the original invoice for a single late fee after a certain period. Some businesses charge a flat fee like $50 or $100 after thirty days. Whatever you choose, state it clearly and consistently.

Check your local laws before implementing late fees. Most jurisdictions allow reasonable late fees, but some have limits. In the United States, late fees are generally allowed as long as they’re reasonable and not designed as a penalty. In some states, there are caps on how much interest you can charge. Research your specific location to ensure compliance.

The most important thing is that you state your late fee policy clearly in your original contract and on every invoice. Clients can’t claim they didn’t know about it. They can’t argue you’re being unreasonable. It’s written right there in the original agreement they signed.

Communicating late fees is straightforward. Include them on every invoice in a visible location. State the exact fee amount and the trigger date. Include them in your payment terms section. Make it impossible for a client to claim surprise when a late fee appears.

When you charge a late fee, you’re not being difficult or greedy. You’re being professional. You’re protecting your business and creating an incentive for clients to pay on time. Most clients respect that approach.

Step 5: Offering a Payment Plan (When Flexibility Makes Sense)

If a client has genuinely communicated that they’re facing cash flow problems, offering a payment plan is often better than pushing them toward collection or legal action. A payment plan isn’t about being soft. It’s about pragmatism. Getting paid half now and half later is better than getting paid nothing.

The key word here is “communicated.” If a client is avoiding you and you have no idea what’s going on, you don’t offer a payment plan. But if a client calls you and says, “I want to pay this, but I can’t do it all at once right now,” that’s a different situation entirely. That’s someone being honest with you. That honesty deserves flexibility in return.

I’ve learned that clients who communicate their problems are usually worth working with. They’re not trying to cheat you. They’re having a legitimate cash flow issue. Maybe they’re waiting for a large client to pay them. Maybe they had an unexpected expense. Maybe they’re experiencing seasonal slowness in their business. These situations are temporary, not permanent.

A payment plan recovers your revenue over time while actually strengthening the business relationship. The client sees that you’re willing to work with them during a difficult period. They feel respected instead of attacked. When their cash flow improves, they remember that you helped them through a tough time. They’re more likely to hire you again and refer you to others.

The structure of the payment plan matters. You want it to be achievable for the client but fast enough that you’re not waiting six months to collect. A typical structure is to break the total amount into three or four installments spread over thirty to sixty days.

When to Offer a Payment Plan

Offer a payment plan only when specific conditions are met. You’re not being generous to everyone. You’re being strategic about who deserves flexibility.

First, the client must be communicative. They’ve reached out and explained their situation. They’re not ghosting you. They’re not avoiding the problem. They’re facing it head-on and asking for help. That communication is the green light that tells you they’re a good candidate for a plan.

Second, the client must have a legitimate reason for the delay. Cash flow problems, waiting for another client to pay them, unexpected expenses, seasonal slowness. These are real business challenges. Chronic non-payers trying to get out of paying entirely are different. Offer plans to clients with legitimate problems, not to chronic avoiders.

Third, the client should have a track record with you. If this is a new client, be cautious. If the client has paid you on time before and is now having a temporary problem, that’s a much better candidate for a plan than a client who’s always been slow.

Don’t offer payment plans to clients who are ignoring you, disputing the legitimacy of the invoice, or clearly trying to avoid payment. Those situations require different approaches. Payment plans are for clients who want to pay but genuinely can’t right now.

Payment Plan Agreement Template

Get any payment plan in writing. Verbal agreements are vague and unenforceable. A simple written agreement protects both of you and clarifies expectations.

PAYMENT PLAN AGREEMENT

This payment plan agreement is made between [Your Business Name] (Creditor) and [Client Business Name] (Debtor) on [Current Date].

Outstanding Debt:

Original Invoice Number: [Invoice Number]

Original Amount Due: [Original Amount]

Current Total Amount Due (including any accrued late fees): [Total Amount]

Payment Plan Terms:

The debtor agrees to pay the outstanding debt of [Total Amount] according to the following schedule:

Payment 1: [Amount] due on [Date]

Payment 2: [Amount] due on [Date]

Payment 3: [Amount] due on [Date]

Payment 4: [Amount] due on [Date]

Each payment should be made to [Your Business Name] via [Payment Method] and sent to [Payment Address/Contact].

Late Payments:

If any scheduled payment is not received by its due date, a late fee of [Amount or Percentage] will be applied. If two or more payments are missed, the entire remaining balance becomes immediately due.

Full Agreement:

By signing below, both parties agree that this payment plan supersedes any previous collection efforts and that the debtor commits to making all payments on time. The creditor agrees to cease collection activities as long as payments are made on schedule.

Signatures:

Creditor: _________________________ Date: _________

[Your Name]

Debtor: _________________________ Date: _________

[Client Representative Name]

This agreement is simple and clear. It outlines exactly what’s owed, when payments are due, and what happens if payments are missed. It’s enforceable because both parties have signed it. It protects you because it establishes that the client agreed to the plan and understands the consequences of missing payments.

Email the agreement to the client, have them sign it digitally, and keep a copy for your records. This written agreement transforms a verbal arrangement into a legal obligation.

When a client signs a payment plan agreement, they’ve made a commitment. They understand they can’t just disappear if they change their mind. They know that missing payments triggers additional consequences. This accountability helps ensure they follow through.

Most clients who enter into payment plans honor them. They’re relieved to have a manageable path forward. They’re grateful that you’re willing to work with them instead of sending them to collection. Honor that goodwill by being flexible and professional throughout the payment schedule.

Step 6: The Final Demand Letter (Last Stop Before Legal Action)

A formal demand letter is your last internal effort before escalating to a collection agency or filing a lawsuit. This is the point where you’re telling the client directly that legal action will follow if they don’t pay. It’s not a suggestion. It’s a formal notice that you’re serious about collecting what you’re owed.

The demand letter serves a specific purpose. It creates a documented record that you made a final attempt to collect before pursuing legal action. If you do end up in court, the judge will want to see that you gave the client reasonable opportunity to pay. A formal demand letter demonstrates that you did exactly that.

I recommend sending a demand letter via certified mail with return receipt requested. This gives you proof that the client actually received the letter. It shows the date they received it. This documentation becomes important if you later need to pursue legal action. A judge will want evidence that the client knew about the demand and chose to ignore it.

The tone of a demand letter is formal and serious. This isn’t the friendly reminder email from day one. This is a legal document. Use professional language. Be direct about what’s owed and what will happen if payment doesn’t arrive. State specific dates and amounts. Leave no room for ambiguity or misunderstanding.

The demand letter gives the client one final chance to pay before things escalate significantly. Most clients who receive a formal demand letter understand that this is the last warning. They either pay or prepare for more serious consequences. Some clients will call you to work out a payment plan or discuss the debt. That’s fine. That’s actually progress. But many will simply pay to avoid the hassle of legal proceedings.

Formal Demand Letter Template

Use this template as your demand letter. Print it on your business letterhead, sign it, and send it via certified mail. Keep a copy for your records.

FORMAL DEMAND FOR PAYMENT

[Date]

[Client Name]

[Client Address]

[City, State ZIP Code]

RE: FORMAL DEMAND FOR PAYMENT OF OUTSTANDING DEBT

Invoice Number: [Invoice Number]

Amount Due: [Total Amount Owed]

Dear [Client Name]:

This letter is a formal demand for immediate payment of the outstanding debt owed by [Client Business Name] to [Your Business Name].

Details of the Debt:

Invoice Number: [Invoice Number]

Invoice Date: [Original Invoice Date]

Original Amount: [Original Amount]

Amount Due Today (including late fees and interest): [Total Amount with all charges]

Original Due Date: [Original Due Date]

Current Status: [Number] Days Past Due

Services/Products Provided: [Brief description of what was provided]

Payment History:

Despite multiple requests for payment, including:

• Email reminder sent on [Date]

• Phone call made on [Date]

• Formal past due notice sent on [Date]

The above-referenced debt remains unpaid and outstanding.

Demand for Payment:

You are hereby formally demanded to pay the full amount of [Total Amount] on or before [Specific Date, typically 10-14 days from letter date].

Payment must be made to:

[Your Business Name]

[Your Address]

[Your Phone Number]

[Your Email]

Payment methods accepted: [List acceptable payment methods]

Consequences of Non-Payment:

If full payment is not received by [Specific Date], the following action will be taken:

- This matter will be referred to a licensed collection agency

- A report will be filed with credit bureaus, negatively impacting your business credit rating

- Legal action will be pursued in [appropriate court], including but not limited to:

• Filing a lawsuit to recover the full amount owed

• Obtaining a judgment against you

• Pursuing post-judgment remedies including wage garnishment, bank levies, and property liens - You will be responsible for all court costs, attorney fees, and collection costs in addition to the original debt

Right to Dispute:

If you dispute this debt or believe you have already paid this amount, you must notify [Your Name] in writing within ten days of receiving this letter. Provide documentation supporting your dispute or proof of payment.

Final Notice:

This is a final demand for payment. Upon receipt of this letter, you have ten days to either:

• Pay the full amount owed, or

• Contact [Your Name] to discuss payment arrangements or dispute the debt

Failure to respond or take action will result in immediate escalation to collection and legal proceedings.

Sincerely,

[Your Signature]

[Your Printed Name]

[Your Business Name]

[Business Address]

[Phone Number]

[Email Address]

CC: [Your business records]

Send this letter via certified mail with return receipt requested. Go to your local post office and ask for certified mail service. The post office will provide you with a tracking number and eventually a receipt showing the date the letter was delivered and who signed for it. Keep all of this documentation for your records.

Why Certified Mail Matters

Certified mail creates legal proof that the client received your demand letter. This matters enormously if you end up in court. You need to demonstrate that the client knew about your demand and had opportunity to comply.

Regular email or regular mail doesn’t provide this proof. The client could claim they never received the letter. They could say it went to spam. They could deny ever seeing it. With certified mail, you have an official postal service record showing the exact date and time the letter was delivered and who signed for it.

This documentation strengthens your legal position significantly. If you file a lawsuit, the court will see that you made a formal demand, gave them a reasonable timeframe to pay, and they ignored it. That creates a clear record of your reasonable attempts to collect before escalating.

The cost is minimal. Certified mail with return receipt usually costs five to ten dollars. It’s the best investment you can make in protecting your legal claim.

Keep the certified mail receipt and the signed return receipt together in a file. If you later need to pursue legal action, provide these documents to your attorney immediately. They’re crucial evidence that you followed proper procedure in attempting to collect.

Step 7: How to Send Someone to Collections (When You’ve Tried Everything)

You’ve sent invoices, made calls, sent payment reminders, and nothing worked. At this point, sending someone to collections might be your best option to actually recover what you’re owed. A collection agency can pursue the debt on your behalf and often succeeds where your own efforts haven’t.

Sending a debt to a collection agency is typically your move when the amount owed exceeds $2,000. Below $2,000, the costs of collection often outweigh what you’ll recover. But for larger debts, a professional collection process can be worth exploring as your final recovery option before writing off the loss entirely.

What You Need Before Contacting a Collection Agency

Before you hand off your case to a collection agency, you need to have your documentation organized and complete. The agency won’t be able to pursue the debt effectively without the right information from you.

Here’s what you absolutely need to provide:

The debtor’s full legal name, current address, and phone number form the foundation of any collection case. Without accurate contact information, the agency can’t even locate the person to begin recovery efforts.

You’ll also need the total amount owed, the exact date the debt was incurred, and ideally a copy of the original invoice or statement that documents the transaction. This paperwork proves the debt actually exists and shows exactly what services or products were provided.

Having clean documentation signals to a collection agency that your case is solid. It also makes the debtor harder to deny or dispute their obligation. The more complete your file, the more seriously the agency will pursue recovery.

How Much Does a Collection Agency Cost?

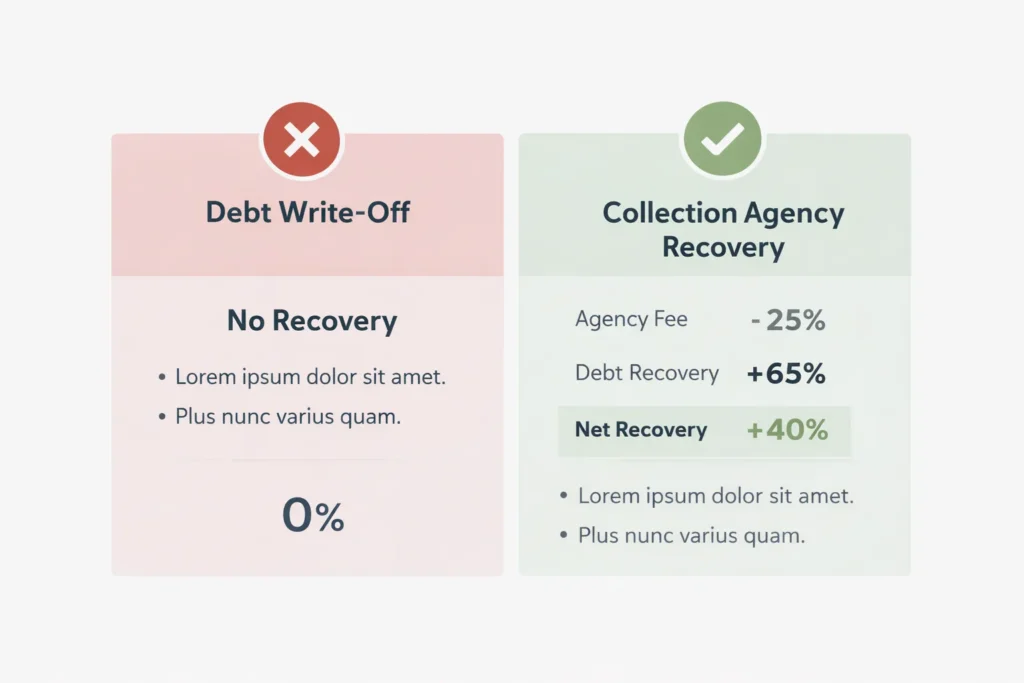

A collection agency doesn’t work for free, and you should know their fee structure before committing to the process. Most agencies operate on a contingency basis, meaning they only get paid if they successfully recover money from your debtor.

Expect to pay between 20 to 25 percent of whatever amount the collection agency recovers on your behalf. So if they collect $10,000, you’d pay them $2,000 to $2,500. You keep the remaining $7,500 to $8,000.

The real question most business owners ask is whether it’s worth it. The answer is usually yes, because collection agencies succeed over 50 percent of the time. That’s a success rate most of us can’t match on our own. Even after paying their commission, you’re recovering money you otherwise wouldn’t see at all.

Compare this to writing off the debt completely, which means you recover zero dollars. A 50 percent recovery rate at a 25 percent cost still leaves you ahead financially. The collection process moves the debt from “lost money” to “recovered revenue,” which changes your entire financial picture.

The $20 Alternative: Going Public with a Business Disputes Register

If the debt amount is lower or you want to try one more approach before formal collection, there’s an unconventional tactic that often surprises people with its effectiveness. You can file a dispute on the Business Disputes Register for just $20, which makes your unpaid invoice public.

This might sound unusual, but it works because most business owners care about their reputation. Once their unpaid debt appears on a public register, the reputational pressure often motivates them to settle quickly to remove the listing from public view. Nobody wants a potential client or partner discovering they have outstanding disputes.

The beauty of this approach is the low cost and simplicity. For $20, you’re creating genuine consequences for non-payment without involving lawyers or formal legal proceedings. Many debtors will settle to protect their business reputation when they realize the alternative is permanent public record of their unpaid obligations.

This tactic works best when the debtor is an established business that values its standing in the community. It’s less effective for individuals or one-person operations that don’t care as much about public image. But as a middle ground between friendly payment reminders and formal collection, the Business Disputes Register offers real leverage at minimal cost.

Legal Options: Small Claims Court vs. Hiring an Attorney

At some point, you might realize that collection agencies and public registers aren’t going to work. When that happens, you’re left with a choice: take the debtor to small claims court yourself or hire an attorney to pursue the case. Understanding which path makes sense for your situation depends on how much money you’re owed and what you’re willing to spend to recover it.

The harsh truth I’ve learned is that winning in court doesn’t automatically mean you’ll get paid. A favorable judgment is just the beginning. The real challenge comes after you win, when you have to actually enforce that judgment and collect the money. This is why it’s critical to understand all your options before spending time and money on legal action.

Small Claims Court (DIY Option)

Small claims court exists specifically for everyday business disputes where the amount involved isn’t large enough to justify hiring an expensive attorney. Most states allow claims between $2,000 and $15,000 in small claims court, though the exact limits vary by location.

The biggest advantage of small claims court is that you can represent yourself without hiring a lawyer. You walk into court, present your case, show your documentation, and let the judge decide. Filing fees are typically modest, usually between $50 and $300 depending on your state and claim amount. Compared to attorney fees, this is incredibly affordable.

The filing process is straightforward. You fill out a simple form describing your claim, pay the filing fee, and serve the defendant with notice of the lawsuit. The debtor then has an opportunity to respond. If they don’t show up to court, you often win by default. If they do show up, both sides present their cases, and the judge makes a decision.

Small claims court works best when your case is clear cut. You have an invoice, they didn’t pay, the amount is documented. The simpler your case, the better you’ll do representing yourself. Judges see hundreds of these cases and can usually spot obvious non-payment situations quickly.

The downside is that small claims decisions are final or have limited appeal rights depending on your state. If you lose, your recovery options are limited. Also, this process takes time. From filing to judgment usually takes several weeks to a few months.

Hiring a Collection Attorney

For claims larger than your state’s small claims limit, you’ll need to file in regular court and work with a collection attorney. This is where legal costs get serious. Attorneys charge either hourly rates, typically $150 to $400 per hour, or contingency fees similar to collection agencies where they take a percentage of what they recover.

An attorney makes sense when the debt is large enough to justify their fees. If you’re owed $50,000 and pursue it through attorney representation, the legal investment is reasonable. But if you’re chasing $5,000, you need to do the math carefully. Attorney fees can easily consume half your recovery or more.

Hiring a collection attorney also signals seriousness to the debtor. Many people will settle quickly once they receive a formal demand letter from a lawyer. The psychological impact of legal involvement motivates payment faster than friendly reminders ever could. After 90 days of late payment, a demand letter from an attorney is often worth the investment because it frequently triggers immediate settlement.

The attorney handles everything from filing to representation in court. You don’t have to appear in person or manage the process yourself. For larger disputes involving breach of contract claims or complex situations, professional legal representation is invaluable.

What Happens After You Win (Post-Judgment Enforcement)

This is the part nobody likes to talk about, but it’s absolutely critical to understand. Winning a judgment and actually collecting money are two entirely different things. I’ve seen plenty of cases where someone won in court and still never saw a dime because they didn’t understand post-judgment enforcement options.

Once you have a favorable judgment, you have several tools to actually collect the money. Wage garnishment allows you to tap directly into the debtor’s paycheck, with a portion going toward your judgment until the debt is paid. This is powerful because the money comes automatically before the debtor ever sees it.

Bank levies let you freeze the debtor’s bank account and claim funds to satisfy the judgment. Property liens attach to real estate or vehicles the debtor owns, preventing them from selling or refinancing without paying you first. These liens create ongoing pressure because the debtor can’t access their assets until they settle with you.

The reality is that enforcement requires additional steps and potentially more costs. You may need to conduct a debtor examination, which is a court process where you question the debtor about their assets and income. This helps you figure out where their money is and how to access it.

Some debtors are judgment proof, meaning they have no accessible assets or income. If someone is unemployed, owns nothing, and has no bank accounts, even a perfect judgment won’t help you recover anything. This is why the cost benefit analysis matters so much before you pursue legal action in the first place.

The statute of limitations determines how long you have to enforce a judgment, usually 7 to 20 years depending on your state. This gives you time to pursue collection options, but it also means you need to stay persistent. A judgment that sits unused loses its power to motivate settlement.

When to Walk Away: Knowing When a Debt Isn’t Worth Chasing

Sometimes the smartest business decision you can make is to stop chasing money that’s costing you more to recover than it’s worth. I know that sounds counterintuitive, but there’s a real point where continuing to pursue a debt becomes a poor investment of your time, energy, and money.

Every dollar you spend on collection efforts, every hour you spend following up, and every ounce of stress you carry over unpaid invoices represents a cost to your business. If you’re spending $500 in collection costs to chase $300, you’ve already lost that battle. The key is recognizing when you’ve hit that threshold and moving on.

The Cost-Benefit Reality

When I look at whether a debt is worth pursuing, I do simple math. If an invoice is under $500 and the client has been unresponsive for 60 days, the odds of recovering that money almost never justify the effort required. You’re better off writing it off, learning from the experience, and protecting your future cash flow by tightening your client screening process.

The longer an unpaid invoice sits, the harder it becomes to collect the money. Time works against you, not for you. After three months of non-payment with no contact, most debtors have already mentally moved on. They’ve spent the money, and pursuing them further often feels like squeezing blood from a stone.

Sometimes a client will file for bankruptcy, which essentially eliminates your creditor rights and any realistic chance of collection. When someone declares bankruptcy, unsecured debts like unpaid invoices fall to the bottom of the priority list. You might recover pennies on the dollar, if anything at all. Fighting a bankruptcy case requires expensive legal work that rarely pays off for small business owners.

Making the Walk Away Decision

The decision to write off a bad debt isn’t admitting defeat. It’s making a rational business choice based on available information. Writing off a debt means you’ve decided the cost of further collection efforts exceeds the potential recovery.

Here’s a practical framework to use. First, estimate the realistic recovery percentage based on the debtor’s situation. If they’re employed and stable, your odds are better. If they’re unemployed or in financial distress, your odds drop significantly. Second, calculate total collection costs including your time at an hourly rate. Third, multiply the debt amount by your realistic recovery percentage, then subtract collection costs. If the result is negative, walking away is the right answer.

One important detail to address with your accountant involves the tax implications of bad debt write-offs. Depending on your business structure and accounting method, you may be able to deduct the unpaid invoice as a business loss on your taxes. This at least provides some recovery value. Consult with a tax professional about your specific situation before writing anything off.

Preventing Future Bad Debts

The real lesson from writing off a debt is preventing it from happening again. Every unpaid invoice teaches you something about your client screening process, your contract terms, or your payment collection procedures. Use that knowledge to tighten your systems going forward.

Require deposits upfront for new clients, especially those you don’t know well. Set clear payment terms in writing before starting any work. Use automated payment reminders and follow up aggressively in the first 30 days when debtors are most responsive. If you notice a pattern of late payment or evasion, stop working with that client immediately. Protecting your future cash flow is worth more than chasing past debts.

Sometimes knowing when to stop is just as important as knowing when to fight. The strongest businesses know the difference.

How to Prevent Unpaid Invoices in the Future (Set It and Forget It)

The best collection strategy is prevention. Once you’ve dealt with the stress and cost of chasing unpaid invoices, you’ll understand why building systems to stop them before they happen is so valuable. The good news is that most unpaid invoice problems stem from easily fixable business practices, not impossible client situations.

I’ve seen businesses cut their overdue invoices by 70 percent with simple changes to when and how they invoice. The same improvements apply whether you’re a freelancer sending one invoice per month or a business managing hundreds of outstanding invoices across dozens of clients. Small adjustments compound into dramatically better cash flow.

Invoice Immediately After Delivery

The biggest mistake I see is waiting to invoice. Many business owners finish a project, then take days or even weeks to send the invoice. By that time, the client’s mind has moved on to other things, and your invoice feels like an afterthought rather than an immediate obligation.

Invoice the moment you complete the work or deliver the product. Same day is ideal. This creates urgency in the client’s mind and establishes that payment is an immediate expectation, not something to handle eventually. One business owner reported a 70 percent reduction in overdue invoices simply by invoicing within 24 hours of delivery instead of waiting a week.

The psychology here matters. When you invoice quickly, payment feels connected to the work they just received. When you invoice weeks later, it feels disconnected and easy to deprioritize. Speed signals professionalism and creates the expectation of prompt payment.

Require Deposits for All New Clients

Deposits are your insurance policy against non-payment. I require a deposit from every client I haven’t worked with before, and it’s changed my business completely. A deposit accomplishes multiple things at once: it ensures you have cash on hand to start work, it filters out clients who aren’t serious, and it dramatically improves payment behavior for the remaining balance.

The deposit amount varies by project size and industry, but typically 25 to 50 percent is standard. For a larger project, consider a 50 percent upfront deposit, then structure the remaining balance as milestone payments. One company achieved 80 percent on-time payments simply by implementing upfront deposits before starting any work.

For a $12,000 project, structure it as 50 percent deposit upfront, 25 percent at intermediate milestones, and 25 percent at final delivery. This approach means you never wait until the very end to receive payment, and you always have partial compensation even if the final payment stalls.

Clients who are willing to pay deposits are signaling that they take the project seriously and have the money available. Clients who balk at deposits are often the same ones who’ll delay payment later. Deposits act as an early screening mechanism.

Make It Easy to Pay: Offer Multiple Payment Options

The easier you make it to pay, the faster people will pay. If your clients have to jump through hoops to send money, payment gets delayed. If payment takes one click, it happens immediately. I’ve seen businesses increase on-time payments by 10 percent simply by expanding their payment options.

Offer multiple payment methods: credit card, PayPal, bank transfer, and ACH payment. If you haven’t already, make sure you have a proper business bank account set up to receive transfers cleanly and keep your business finances separate. Use a payment gateway like Stripe or Square to process cards, and services like GoCardless to handle recurring or one-time bank transfers. Some clients prefer cards, others prefer direct bank transfers. Give everyone an option that feels natural to them.

The payment gateway handles the processing fees, which you might absorb or pass along depending on your industry. Offering PayPal or credit card options costs you 2 to 3 percent in fees, but that cost is worth it if it accelerates payment by weeks. You recover those fees instantly through improved cash flow.

Set Clear Payment Terms (And Make Them Shorter)

Ambiguous payment terms create confusion and delays. Instead of assuming clients know when to pay, spell it out clearly in every invoice and contract. Write “Payment due within 15 days of invoice date” rather than the vague “due on receipt.”

The standard Net 30 payment term has become almost meaningless. Many clients interpret Net 30 as a starting point for negotiation or simply ignore it. Consider using Net 15 payment terms instead, which feels more urgent and gives you faster cash recovery. The tighter your credit terms, the faster your outstanding invoices disappear.

Include payment terms in your written contract before starting work. Don’t leave it to chance or hope that clients understand your expectations. Clear credit terms reduce confusion and make late payment easier to address because you have a written agreement to reference.

Automate Everything with Accounting Software

Manual invoicing and payment tracking is where mistakes happen and follow-ups get missed. Automation removes the guesswork and ensures nothing falls through the cracks. Use accounting software like QuickBooks, FreshBooks, or Wave to handle your AR automation.

These platforms send invoices automatically, track payment status, and can even send automatic payment reminders at specific intervals. You can set up automatic emails that go out three days before payment is due, then again on the due date if payment hasn’t been received. This removes the emotional burden of chasing clients because the system does it for you.

For recurring payments, require autopay with signed authorization. Have clients sign an agreement allowing you to automatically charge their credit card or bank account on a specific date each month. Services like GoCardless make this incredibly simple to set up. After experiencing non-payment, many business owners now require autopay for all future recurring work because it eliminates the variable of client willingness to pay.