A foreign employer identification number is a standard nine digit EIN issued by the IRS to a foreign person, foreign company, or foreign owned US entity that has a US tax obligation but does not hold a Social Security Number.

What Is a Foreign Employer Identification Number?

A foreign employer identification number is the same nine digit Employer Identification Number that the IRS issues to domestic US businesses, applied specifically to foreign individuals, foreign companies, and foreign owned US entities that have a US tax reporting obligation.

Let me be direct about something right away.

The phrase “foreign employer identification number” gets used in two slightly different ways, and the confusion between those two meanings causes real problems for people trying to navigate the IRS system. So I want to separate them clearly before we go any deeper.

The first meaning refers to an EIN that a foreign entity obtains from the IRS for its own US tax purposes. A Canadian holding company that owns a Delaware LLC needs a US EIN. A German GmbH with US employees needs a US EIN. A Singapore based investor who forms a Wyoming LLC needs a US EIN. In every one of those cases, the foreign entity is applying to the IRS and receiving an American nine digit tax identification number, formatted as XX-XXXXXXX. That number is what most people mean when they search for “foreign employer identification number.”

The second meaning refers to a foreign country’s own tax identification number assigned to a business by a non-US government. When a US financial institution asks you to provide a “foreign tax identification number” or “FTIN” on a withholding form, they are asking for the number your home country assigned your business, not a US number. This comes up constantly on W-8BEN-E forms, and it trips up a lot of people.

I am going to cover both meanings thoroughly in this guide because both matter and both appear in real situations you will face when operating internationally.

The Employer Identification Number itself is a federal tax ID number issued by the Internal Revenue Service. It functions as a business’s tax identity in the US system the same way a Social Security Number functions as an individual’s tax identity. You use it to open US bank accounts, hire US employees, file US tax returns, apply for business licenses, and establish credit in the US financial system.

According to the IRS, any entity that has a US federal tax filing or reporting requirement needs an EIN. That requirement does not care where the entity was formed or where its owners live. A foreign company with US sourced income needs one. A foreign person who is the sole owner of a US LLC needs one for that LLC. A foreign trust with US assets needs one.

And here is the part that surprises most people who contact me with questions about this topic.

You do not need a Social Security Number to get one. Full stop.

Who Qualifies as a Foreign Person for an EIN?

A foreign person for EIN purposes is any individual, company, trust, or estate that is not a US citizen, US permanent resident, or domestic entity under US tax law.

The IRS uses specific language here. The term non-resident alien (NRA) describes a foreign individual who is not a US citizen and does not meet the substantial presence test or the green card test for US tax residency. That distinction between resident alien and non-resident alien matters enormously because it determines how your US income gets taxed.

But for EIN eligibility specifically, the question is simpler. Can you legally form or own a US entity, or do you have a direct US tax obligation? If yes, you can get an EIN.

EIN Responsible Party for Non-US Citizens

The responsible party is the single most important concept in any EIN application. This is the person the IRS holds accountable for the entity’s tax obligations. They must be a real human being. Since January 2014, the IRS no longer accepts another entity as the responsible party for most EIN applications.

Here is exactly where non-US citizens run into trouble.

On IRS Form SS-4, Line 7b asks for the responsible party’s Social Security Number, ITIN, or EIN. If a non-US citizen has none of those, the IRS instructs them to write the word “Foreign” in that field. That single word is your workaround. It is not a trick or a loophole. It is the official IRS instruction, documented in the Form SS-4 instructions themselves.

The EIN responsible party who is a non-US citizen must still provide identifying information. Their name, their title within the entity, and their foreign country of residence are all captured on the form. The IRS accepts a foreign passport number or foreign national ID number as supplementary identification when processing these applications by phone or fax.

So to be direct about who qualifies: foreign nationals, non-resident aliens, foreign corporations, foreign LLCs formed in other countries, foreign trusts, foreign estates, and foreign partnerships with US nexus can all obtain a US EIN. The residency and citizenship of the owner does not bar you from getting the number.

What matters is that there is a legitimate reason for the EIN to exist, meaning a real US tax obligation or a legally formed US entity that will have one.

Can a Non-US Resident Get an EIN?

Yes. A non-US resident can absolutely get a US Employer Identification Number. The IRS provides specific application methods for international applicants who cannot use the standard online system.

This is one of the most searched questions in the entire EIN topic space, and the answer is a clean yes. But the path to getting it is slightly different from what a US resident experiences.

US residents with a Social Security Number can apply for an EIN entirely online at IRS.gov and receive their number instantly. The online system is fast, free, and available around the clock.

Non-US residents without an SSN or ITIN cannot use that online system. The IRS restricts online EIN applications to people who have an SSN or ITIN. But three alternative methods are fully available and the IRS processes them routinely.

I am going to give you the complete breakdown of each method in the application section of this guide. But the core point here is this: being a non-US resident creates a different process, not a barrier to getting the EIN.

The IRS has been issuing EINs to foreign nationals for decades. The system exists specifically because foreign investment in the US is enormous and economically significant. The IRS is not trying to make this impossible. The agency simply requires that you use a specific channel based on your situation.

One thing I want to flag here because it genuinely confuses people who reach out to me after going in circles online.

There are two separate questions that get mixed together constantly.

Question one: Can a non-US resident form a US LLC or corporation? Answer: Yes, in most US states, foreign nationals can form US entities. Delaware, Wyoming, and New Mexico are the most commonly used states for this purpose.

Question two: Can that non-US resident then get an EIN for that US entity? Answer: Yes. Once the entity is legally formed and registered with the appropriate state, the EIN application can be filed.

Those two steps happen in sequence. You form the entity first. Then you apply for the EIN. The IRS will not issue an EIN for an entity that does not yet legally exist.

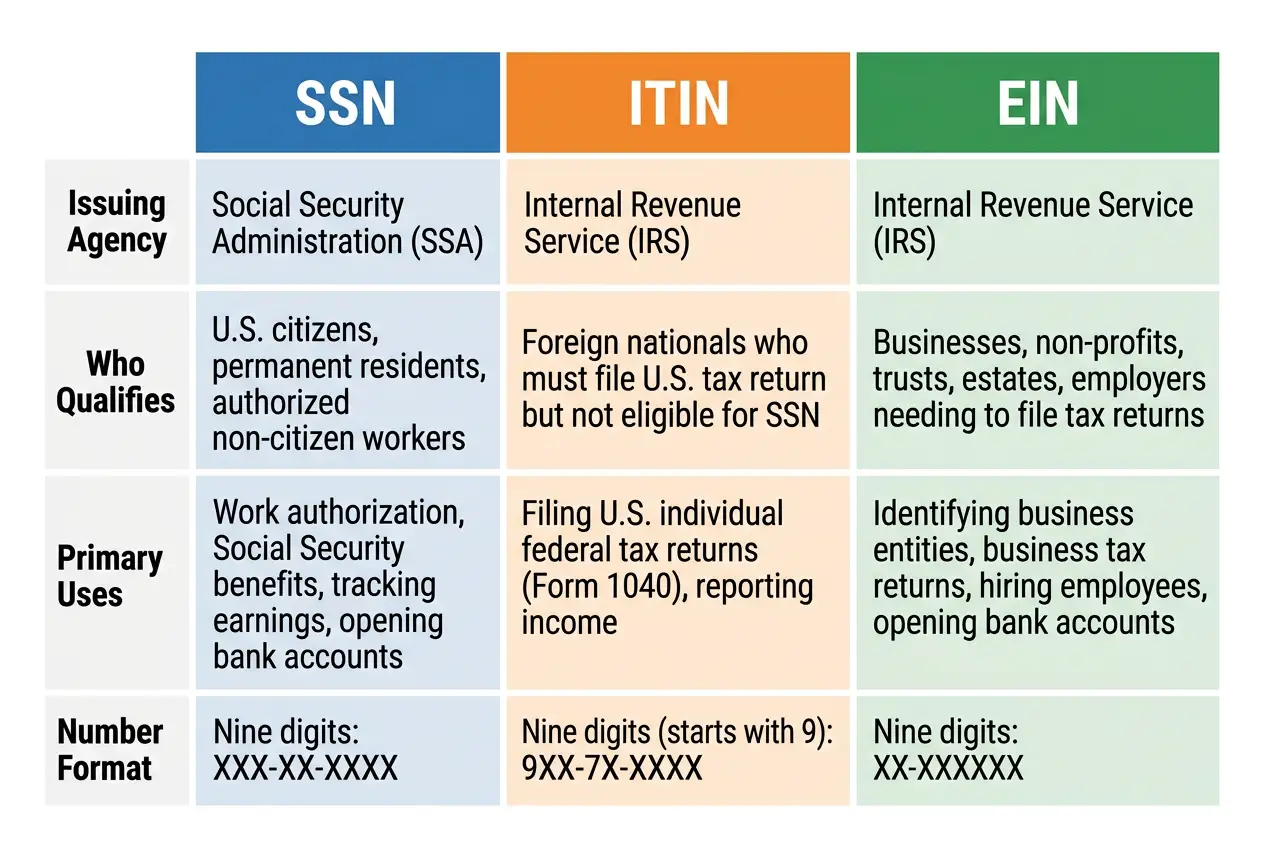

ITIN vs EIN for Foreigners: What Is the Difference?

An ITIN is a personal tax identification number for foreign individuals with US tax obligations who cannot get an SSN, while an EIN is a business tax identification number for any entity with US tax filing requirements.

This is one of the highest confusion points I see, especially on forums like Reddit’s r/llc and in TurboTax community threads where people are genuinely trying to understand which number they need and in what order.

Let me break this down as plainly as I can.

SSN (Social Security Number): Issued by the Social Security Administration. For US citizens and work-authorized residents only. Used for personal income tax filing and employment records.

ITIN (Individual Taxpayer Identification Number): Issued by the IRS via Form W-7. For foreign individuals who have a US tax obligation but cannot get an SSN. Used on personal tax returns (Form 1040-NR), W-8BEN forms, and certain other individual tax documents. An ITIN does not authorize work in the US and does not replace an SSN for employment purposes.

EIN (Employer Identification Number): Issued by the IRS via Form SS-4. For businesses, LLCs, corporations, trusts, partnerships, and other entities. Used for business tax filings, payroll, bank accounts, and business credit.

So the question “which one do I need as a foreigner” depends entirely on what you are trying to do.

If you are a foreign individual filing a US personal tax return because you earned US sourced income, you need an ITIN.

If you are a foreign individual or company that owns or operates a US business entity, you need an EIN for that entity.

And here is the critical piece that answers the question I get most often: do you need an ITIN before applying for an EIN?

Not necessarily. You can apply for an EIN for a US entity without having an ITIN. As I explained above, the Form SS-4 allows foreign responsible parties to write “Foreign” in the field that asks for an SSN or ITIN. The IRS processes it without requiring you to have either.

But there are situations where having an ITIN first is genuinely useful. If you plan to open a US business bank account as the sole proprietor (not through an LLC or corporation), some banks will accept an ITIN plus EIN combination for account opening. If you are going to file a US personal tax return alongside your business return, you will need an ITIN for the personal return.

The EIN vs ITIN difference for foreigners ultimately comes down to the level at which you are operating. Personal tax identity needs an ITIN. Business entity tax identity needs an EIN. Many foreign business owners eventually need both, but for different purposes.

Does a Foreign Company Need an EIN to Operate in the USA?

Yes. Any foreign company that hires US employees, opens a US bank account, withholds US taxes, or has a US tax filing requirement must obtain a US Employer Identification Number.

This question shows up frequently in both Quora discussions and Reddit threads, and the answers out there range from accurate to dangerously wrong. Let me give you the complete picture.

A foreign company that simply sells products to US customers from abroad, with no US employees, no US office, no US bank account, and no formal US business registration, may not need an EIN immediately. Their US tax obligations would generally be handled through withholding by US payers or through treaty provisions.

But the moment a foreign company crosses into any of the following situations, an EIN becomes necessary.

Hiring US employees. Any employer, domestic or foreign, that pays wages to US employees must have an EIN for payroll tax purposes. There are no exceptions.

Opening a US bank account in the company’s name. Every US bank that I have worked with requires an EIN for business account opening. Some banks accepting foreign-owned entity accounts will also require additional documentation, but the EIN is always on the list.

Filing a US tax return. Foreign corporations with effectively connected income in the US file Form 1120-F. That form requires an EIN. Foreign-owned US LLCs file Form 5472 as part of their Form 1120 filing. That requires an EIN.

Withholding taxes from US sourced payments. If a foreign company is acting as a withholding agent, making payments of US sourced income to others, the company must have an EIN to remit the withheld amounts to the IRS.

Operating a US subsidiary or branch. Any formal US business presence, a subsidiary corporation, a branch office, or a registered US entity owned by a foreign parent, needs its own EIN.

The short version: if you are a foreign company doing real business in the United States in any formal capacity, you need a US EIN. The application is free. The process is manageable. And avoiding it creates serious compliance problems that are far more expensive to fix later than they would have been to prevent upfront.

How to Apply for an EIN Without a Social Security Number

You can apply for a US EIN without a Social Security Number by using one of three IRS approved methods: phone application via the IRS international line, fax submission of Form SS-4, or mail submission of Form SS-4.

This is the core practical question that everyone with a foreign identifier needs answered. So I am going to walk through each method with complete detail, including the exact numbers, addresses, and form fields that matter.

Method 1: Apply by Phone (IRS International Line)

This is the fastest option. Full stop.

Call the IRS international EIN line at +1-267-941-1099. This line is open Monday through Friday, 6:00 AM to 11:00 PM Eastern Time. It is a dedicated line for international EIN applicants.

Before you call, have the following ready:

- The legal name of the entity applying for the EIN

- The type of entity (LLC, corporation, partnership, trust, etc.)

- The state where the entity was formed (for US entities) or the country of formation (for foreign entities)

- The reason for applying for an EIN (new business, banking purposes, hired an employee, etc.)

- The responsible party’s full legal name, title, and foreign identification details

- The entity’s principal business address (foreign address is fine)

- The nature of the business or primary business activity

- Whether the entity has or expects to have US employees, and if so, how many

The IRS representative will ask you a series of questions based on Form SS-4 content. They will complete the form on their end based on your verbal answers. At the end of the call, if everything checks out, they will give you your EIN number verbally over the phone.

You will also receive a written confirmation. But you have the number immediately.

One important note I want to flag based on real experiences people have shared in Reddit’s r/llc forum. Wait times on this line can be significant. Some callers report waiting 30 to 45 minutes or longer during peak periods, especially in Q1 and early Q2. Call earlier in the week and earlier in the day for the best chance of a shorter wait.

Also: you do not need to be the responsible party yourself to call. If you have authorized a representative to apply on your behalf, they can call and answer the questions, as long as they have all the entity and responsible party information available.

Method 2: Apply by Fax

To fax your SS-4 to the IRS as an international applicant, use fax number +1-304-707-9471. This is the IRS fax number specifically designated for international EIN applications.

If you include a return fax number on your SS-4 form, the IRS will fax your EIN confirmation back to you in approximately 4 business days.

If you do not include a return fax number, the IRS will mail the confirmation, which takes longer. Always include your return fax number when faxing from abroad.

The fax method is more reliable than a phone call for people who struggle with time zone differences for the IRS phone line hours. Prepare your Form SS-4 completely, fax it to the international number, and wait for the return fax.

Faxing from outside the US: You will need a fax service that can send to US numbers internationally. Many online fax services handle this. Wise, HelloFax, and similar services all work. Make sure to include the international dialing prefix for the US (+1) before the fax number.

Method 3: Apply by Mail

Mail your completed Form SS-4 to:

Internal Revenue Service

Attn: EIN International Operation

Cincinnati, OH 45999

USA

Mail applications take the longest. The IRS estimates approximately 4 to 5 weeks for processing of mailed applications. During periods of high volume, particularly in Q1, this timeline can stretch to 6 to 8 weeks.

I only recommend the mail method when fax is not available and the phone method is not feasible due to time zone constraints or language barriers. If you can fax or call, do one of those instead.

IRS Form SS-4 Instructions for Foreign Applicants

IRS Form SS-4, Application for Employer Identification Number, is the document you submit to request an EIN. Foreign applicants follow the same form but with specific instructions for certain fields.

You can download Form SS-4 directly from IRS.gov at no cost. The form is two pages. The instructions document that accompanies it is longer and worth reading, but I want to highlight the specific fields that trip up foreign applicants.

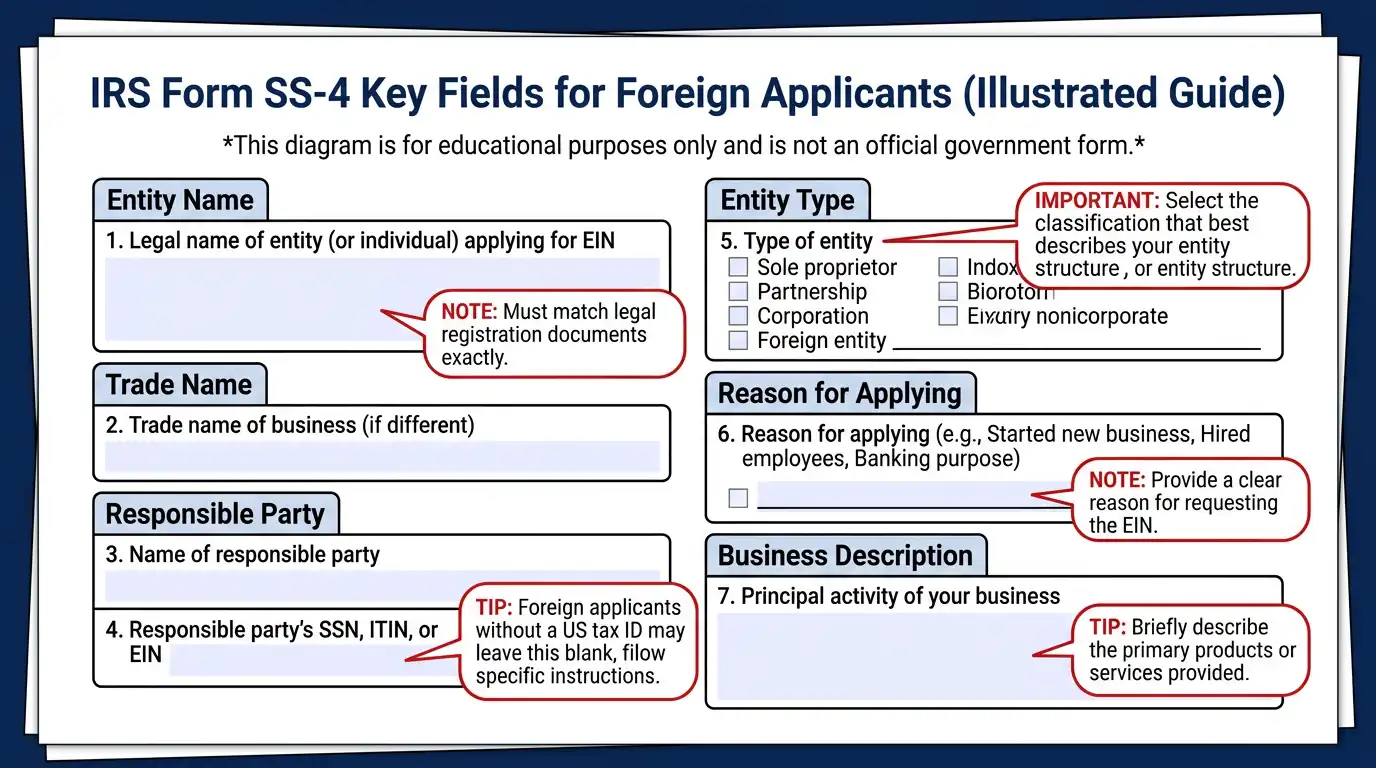

Line 1: Legal name of entity. Enter the exact legal name. For a US LLC, this is the name as registered with the state. For a foreign company, this is the exact legal name in your home country, even if it includes non-English characters.

Line 2: Trade name. Enter only if different from Line 1. Many foreign entities skip this.

Line 3: Executor, trustee, care of name. Used for trusts and estates. Leave blank if not applicable.

Line 4a and 4b: Mailing address. A foreign address is completely acceptable here. Enter the entity’s actual mailing address.

Line 5a and 5b: Street address of principal place of business. If the principal place of business is outside the US, enter that address. If the entity has a US registered office (which most foreign owned US LLCs do via a registered agent), you may enter that address here.

Line 6: County and state where principal business is located. For foreign entities with no US physical presence, write “N/A” or “Foreign.”

Line 7a: Name of responsible party. Enter the full legal name of the responsible individual.

Line 7b: SSN, ITIN, or EIN of responsible party. This is the critical field. If the responsible party is a foreign individual with no SSN or ITIN, write “Foreign” in this field. That is the official IRS guidance. Do not leave it blank.

Line 8a: Entity type. Select the appropriate box: sole proprietor, partnership, corporation, S corporation, personal service corporation, church, estate, trust, LLC, or other. For a standard single member LLC owned by a foreign national, select LLC and enter “1” in the number of members field.

Line 8b: If LLC, number of members. Enter the number of LLC members.

Line 8c: If LLC, check state of formation. If a US LLC, enter the state. If a foreign LLC, indicate the country.

Line 9a: Reason for applying. Check the appropriate box. Most foreign national business owners check “Started new business” or “Banking purpose.”

Line 10: Date business started. Enter the date the entity was legally formed or the date you expect to first pay wages.

Line 11: Closing month of accounting year. Most entities use December (calendar year). Enter the last month of your fiscal year.

Line 12: First date wages will be paid. Leave blank if the entity will not have employees initially.

Lines 13 through 15: Employment and excise tax related questions. Many foreign owned entities with no employees leave these blank or enter zero.

Line 16: Principal activity. Describe what the business does in a few words. Be specific. “Retail e-commerce” or “software consulting” or “real estate investment” are all acceptable.

Line 17: Specific products or services. Add detail about what you sell or provide.

Line 18: Check whether you have applied for an EIN before. Most foreign applicants check “No.”

Signature line: The responsible party or an authorized representative signs here. For a faxed or mailed application, a physical signature is required.

EIN Application Process for Non-Citizens Explained

Non-citizens apply for an EIN using the same Form SS-4 that any US business uses, but they must apply by phone, fax, or mail rather than online, and they write “Foreign” in the field that asks for a Social Security Number.

I want to address something specific here that I see cause confusion on forums repeatedly.

Some non-citizens believe they need to hire an attorney or paid EIN service to get a number because the process seems too complicated to handle alone. That is not true for the majority of straightforward situations.

A single member LLC formed by a foreign national, with one responsible party who has no SSN or ITIN, can be handled via a phone call to the IRS international line. It takes one call, usually completed within an hour including wait time, and the EIN arrives immediately or within 4 days by fax.

Where professional help becomes genuinely valuable is in situations involving:

A foreign trust with US beneficiaries, which triggers complex reporting obligations beyond the EIN application itself. An EIN for a foreign trust is just the beginning of a longer compliance structure.

A foreign corporation with US operations, where the EIN is part of a larger US tax nexus setup including Form 5472 obligations, branch profit tax considerations, and potential treaty elections.

A multi-member LLC with foreign owners spread across multiple countries, where ownership structure, operating agreements, and withholding obligations all interact in ways that require professional judgment.

For the straightforward foreign owned single member LLC situation that represents the majority of inquiries I see, you can handle this yourself. Use the IRS phone line. Have your Form SS-4 information prepared. Call, answer the questions, get your EIN.

One thing that genuinely matters: make sure your US LLC is actually legally formed and registered with the state before you call. The IRS will ask for confirmation that the entity exists. If you call before your LLC formation documents are filed and accepted by the state, the IRS may decline to issue the EIN or issue it under incorrect entity information.

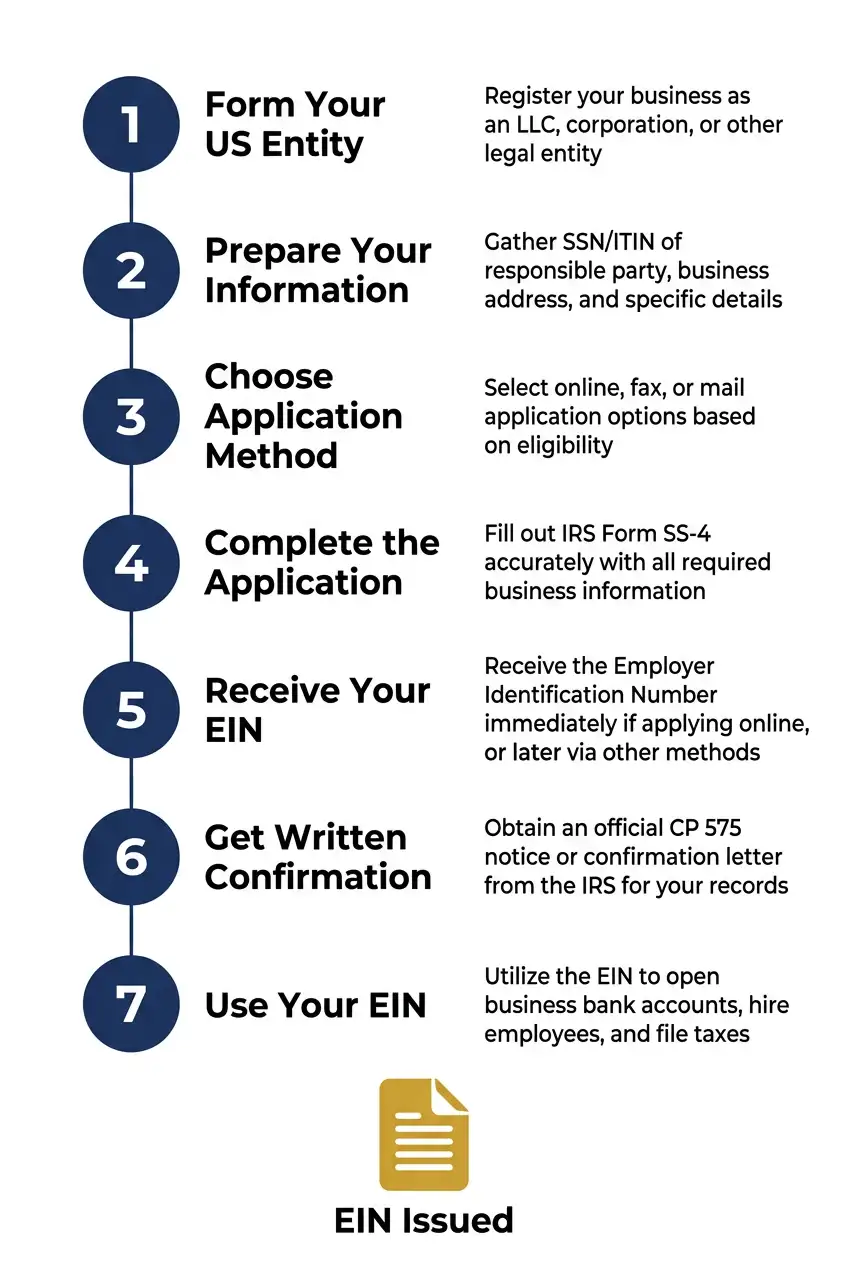

Step by Step: Applying for an EIN as a Foreign National

Here is the complete step by step process for a foreign national to obtain a US Employer Identification Number using the phone method, which is the fastest available option.

I am going to walk through this exactly as it happens in practice, not as an abstract checklist.

Step 1: Form your US entity first.

Go to the Secretary of State website for your chosen state (Delaware, Wyoming, and New Mexico are the most common for foreign nationals, for different reasons) and complete the LLC or corporation formation process. You will need a registered agent in that state. Registered agent services start at around $50 per year and are required for foreign owned entities in virtually every state.

Once your Articles of Organization or Articles of Incorporation are accepted and you have received your state formation documents, you are ready for the EIN application.

Step 2: Prepare all your information.

Write down the following before calling or faxing:

The exact legal name of your entity. The state of formation. The date of formation. The purpose of the business. The name, address, and title of the responsible party. Whether the entity will have US employees and if so, when the first payroll date will be. The principal business activity. The fiscal year end month.

Step 3: Choose your application method.

If time zone and language are not barriers, call +1-267-941-1099 during IRS international line hours. If you cannot call during those hours, complete Form SS-4 and fax to +1-304-707-9471 with a return fax number included.

Step 4: Complete the application.

By phone: Answer the representative’s questions. They work through the Form SS-4 fields with you. When they reach Line 7b, tell them the responsible party is a foreign national with no SSN or ITIN. They will note “Foreign” in that field and continue.

By fax: Write “Foreign” clearly in Line 7b. Complete all other fields accurately. Sign the form. Fax to the international number.

Step 5: Receive your EIN.

By phone: You receive it verbally at the end of the call. Write it down. The representative will also spell it out. Confirm it before hanging up.

By fax: The IRS faxes back a CP 575 or EIN confirmation within approximately 4 business days to the return fax number you provided.

Step 6: Get the written confirmation.

The IRS will mail a formal CP 575 notice to the address on your Form SS-4. This letter is your official EIN confirmation document. Keep it permanently. Some banks, state agencies, and partners will ask to see the original CP 575 when you set up accounts or enter into certain agreements.

Step 7: Use your EIN immediately.

Once you have the number, you can use it for bank account applications, vendor onboarding, contract documentation, and tax filings. The EIN is active from the moment it is issued.

How Foreign Companies Obtain a US EIN from the IRS

A foreign company obtains a US EIN by submitting Form SS-4 via phone or fax to the IRS, designating a responsible party, and writing “Foreign” in the SSN field if the responsible party has no US taxpayer identification number.

For foreign corporations specifically, there are a few additional considerations beyond what a simple foreign owned US LLC faces.

A foreign corporation that is registered and operates entirely outside the US but earns US sourced income files Form 1120-F with the IRS. That filing requires an EIN. The responsible party for the EIN application is typically an officer of the corporation, such as the CEO or director, who is authorized to act on the company’s behalf.

For a foreign corporation with US employees, the EIN application should note on Line 12 the date of first payroll. The IRS will set up the entity’s payroll tax obligations accordingly. Payroll tax deposits for foreign employers with US workers follow the same schedule as domestic employers, using EFTPS (the Electronic Federal Tax Payment System).

The EIN for a foreign corporation also matters for banking purposes. Many US correspondent banks that handle international wire transfers will require the foreign company to provide an EIN when setting up payment relationships with US financial institutions. This is increasingly true in the post-FATCA compliance environment.

Form 5472 is a form I want to flag specifically for foreign owned US corporations. If a US corporation has 25% or more of its stock owned by a foreign person, and if reportable transactions occurred between the corporation and its related foreign parties, Form 5472 must be filed. The penalty for failing to file Form 5472 is $25,000 per form per year, and the IRS enforces this aggressively. The EIN is required for this filing.

Getting an EIN for Your International Business in the US

Foreign nationals starting or expanding an international business in the US need an EIN to open bank accounts, hire employees, sign contracts, and comply with IRS reporting requirements.

I want to talk about foreign owned LLC EIN situations specifically because this is by far the most common scenario I see among people building international businesses with US operations.

The single member LLC owned entirely by one foreign national is a disregarded entity for US federal tax purposes by default. That means the IRS treats it as a pass-through. The income and expenses of the LLC flow directly to the owner’s personal tax return.

But here is what makes this more complex for foreign owners.

A single member LLC with a foreign owner is treated as a disregarded entity, yes, but it still has its own EIN and it still has its own filing obligations. Specifically, it must file Form 5472 (Information Return of a 25% Foreign-Owned US Corporation or a Foreign Corporation Engaged in a US Trade or Business) as an attachment to a pro forma Form 1120.

This is not optional. The IRS introduced this requirement in 2017 and it catches many foreign LLC owners completely off guard. Even if the LLC made no money in the year. Even if it had no transactions whatsoever. If it is a foreign-owned disregarded entity, the Form 5472 requirement applies.

The penalty for not filing: $25,000. Per form. Per year.

I am not trying to alarm you. I am trying to save you from a mistake that I have seen cost people real money.

Get the EIN. File the Form 5472. Keep records of all transactions between you personally and your LLC. This is manageable when you know it exists.

For foreign owned LLCs choosing to be taxed as an S Corporation: Be aware that S Corporation status is generally not available to non-resident aliens. The IRS restricts S Corp shareholders to US citizens and resident aliens. If you are a non-resident alien, your LLC can be taxed as a C Corporation or as a partnership (if multi-member), but not as an S Corporation.

For the EIN for foreign trust scenarios: A foreign trust with US beneficiaries or US grantor involvement has its own EIN and its own set of reporting obligations, including Form 3520 and Form 3520-A. This is genuinely complex territory and falls squarely into “talk to a CPA” territory.

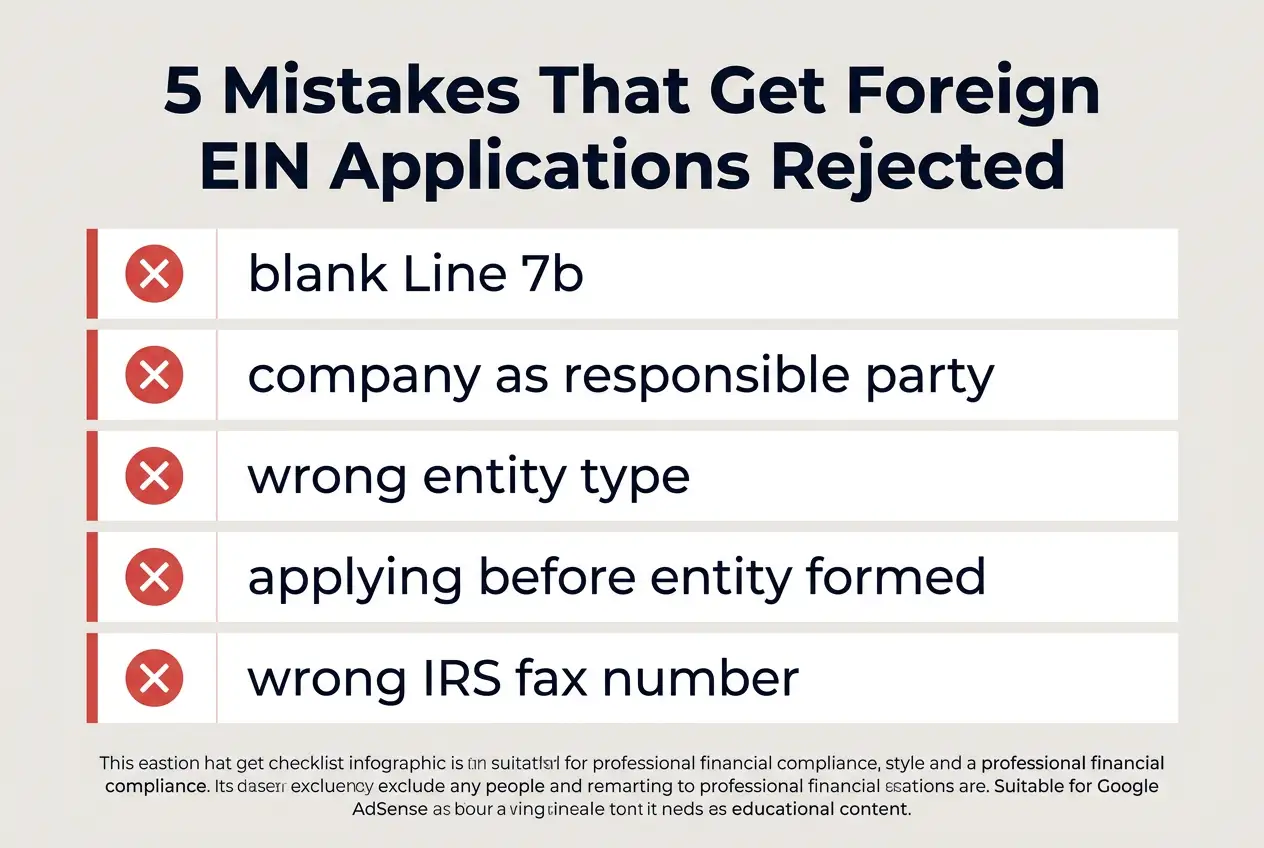

Common Mistakes That Get Foreign EIN Applications Rejected

The most common reasons foreign EIN applications are rejected or delayed include errors in the responsible party field, applying before the US entity is formed, and selecting the wrong entity type on Form SS-4.

Let me go through the specific mistakes I see repeatedly and how to avoid each one.

Incorrect Responsible Party Information

Writing nothing in Line 7b instead of the word “Foreign.” The IRS needs something in that field. If the responsible party has no SSN or ITIN, write the exact word “Foreign.” A blank field creates a processing delay because the IRS will often return the application for completion.

Listing a company or another entity as the responsible party. Since 2014, the IRS requires a real human being as the responsible party for most entity types. Listing your foreign parent company as the responsible party will result in rejection.

Wrong Entity Type Selection

Checking “sole proprietor” when you actually formed an LLC. These are different things. A sole proprietor has no legal entity. An LLC is a legal entity. Checking the wrong box creates a mismatch between your state formation records and your IRS records, which causes problems later when you file tax returns.

Checking “corporation” for a foreign company that has not registered in any US state. A foreign company that has not formed a US subsidiary is not a US corporation. If you need an EIN for the foreign company itself (for withholding purposes, for example), select “other” and describe the entity type.

Applying Before Your US Entity Is Formed

This is perhaps the most common mistake I see among people who are excited to move fast with their US business setup. The IRS issues EINs for entities that exist. If you apply before your state formation documents are approved, you risk the EIN being issued under incorrect information, or the IRS denying the application entirely.

Wait for your Articles of Organization or Articles of Incorporation to be accepted and stamped by the state before filing the SS-4.

Missing or Wrong Business Description

Being too vague in Line 16 and Line 17. “Business services” is not adequate. “Digital marketing consulting services for e-commerce brands” is adequate. The IRS uses this information to assign the correct industry classification, which affects how your returns are processed and cross-referenced.

Wrong Fax Number

This sounds simple, but it is genuinely a problem. The IRS has different fax numbers for domestic and international EIN applicants. The domestic fax number is 855-641-6935. The international fax number is +1-304-707-9471. Using the wrong number means your application goes to the wrong processing center and either gets lost or returned with a significant delay.

How Long Does It Take to Get a Foreign EIN?

Getting a foreign EIN takes anywhere from immediate (by phone) to 4 to 5 weeks (by mail), depending on the application method you use.

Phone Application Timeline

Immediate. You call the IRS international line, complete the verbal application, and receive your EIN number before you hang up. The written CP 575 confirmation letter follows by mail within 4 to 6 weeks, but the number itself is yours on the day of the call.

This is the single clearest reason to use the phone method when at all possible.

Fax Application Processing Times

Approximately 4 business days if you include a return fax number. The IRS faxes back an EIN confirmation to your provided fax number within that window during normal processing periods.

During peak periods (January through April), this can extend to 7 to 10 business days. Plan accordingly if you are applying during tax season.

Mail Processing Times

4 to 5 weeks under normal conditions, 6 to 8 weeks during peak periods. The IRS mails the CP 575 notice to the address on the SS-4. There is no way to speed up a mailed application once it is submitted.

If you have a deadline, whether for a bank account opening or a contract requirement, mail is not your friend. Use the phone or fax method.

EIN verification for a foreign entity after the number is issued can be done in a few ways. The CP 575 letter is your primary verification document. You can also call the IRS Business and Specialty Tax Line at +1-800-829-4933 (US callers) to verify an EIN. Third parties like banks may conduct their own verification through IRS e-services if they have authorization.

What to Do After You Receive Your Foreign EIN

After receiving your foreign EIN, your next steps are to store the CP 575 letter securely, open a US business bank account, set up any required tax accounts, and understand your ongoing filing obligations.

The CP 575 Confirmation Letter

The CP 575 notice is your official EIN confirmation document. It is issued by the IRS and contains your entity name, your EIN, and the date it was assigned. Some banks and state agencies will ask to see the original CP 575 or a copy of it during account opening or licensing processes.

If you lose your CP 575, you can request a 147C letter from the IRS, which serves the same confirmation purpose. Call the IRS Business and Specialty Tax line to request one.

Opening a US Bank Account with Your EIN

This is often the primary reason foreign entities need an EIN open a separate bank account in the first place. Most US banks require an EIN for business account opening. The process varies by bank, but generally requires:

Your EIN (via CP 575 or verbal confirmation from the IRS call)

Your state formation documents (Articles of Organization or Articles of Incorporation)

Your operating agreement (for LLCs)

The responsible party’s passport or government-issued ID

In some cases, a US address (your registered agent address works for this purpose)

Mercury, Relay, and several other fintech banks have more streamlined processes for foreign owned US entities than traditional banks. I mention this because traditional bank branches in the US often require in-person visits, which is obviously challenging for someone who lives abroad.

Setting Up EFTPS for Tax Payments

If your entity will have any US tax payment obligations, payroll taxes, estimated corporate taxes, or withholding remittances, you need to enroll in EFTPS (Electronic Federal Tax Payment System). You can enroll at eftps.gov using your EIN. The process takes a few days because the IRS mails a PIN to your address.

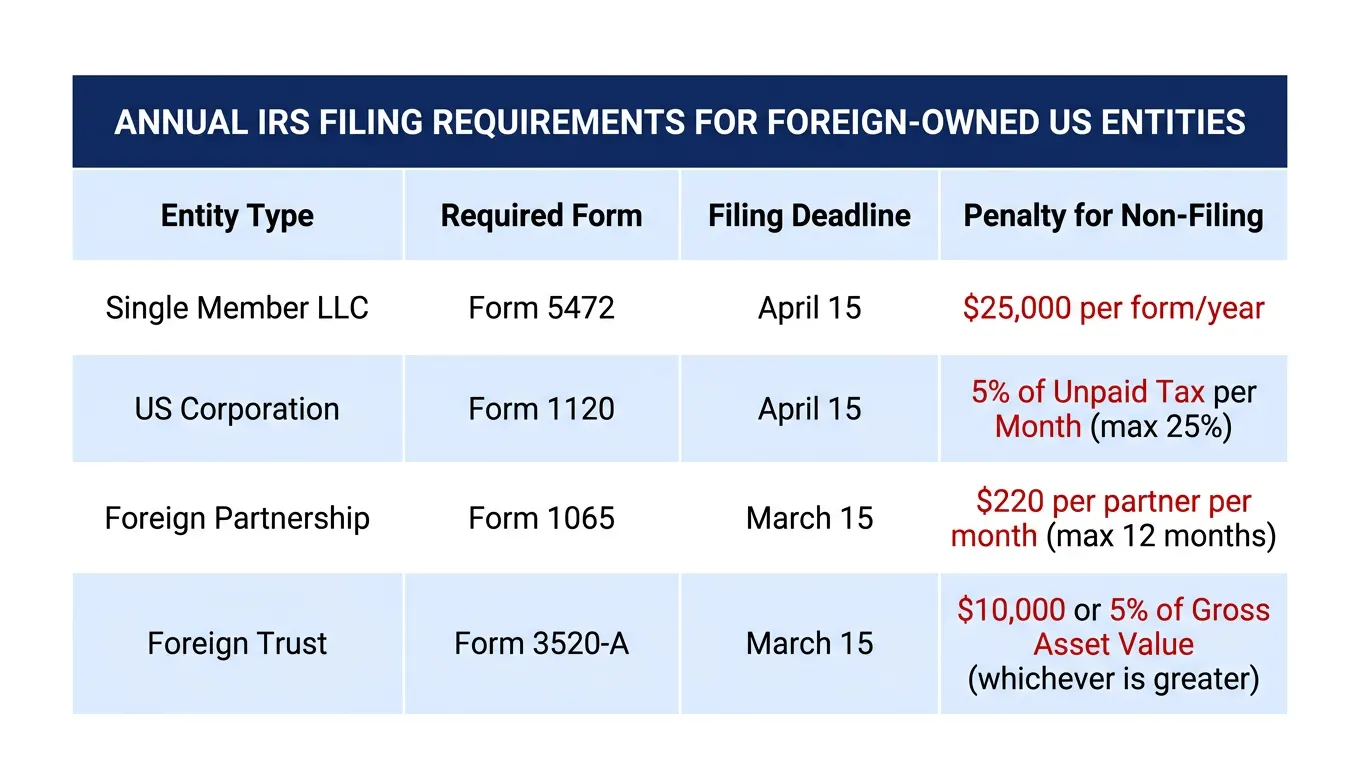

Understanding Your Annual Filing Obligations

This is the piece most people underestimate when they first get their EIN and feel like they are done with the bureaucracy.

A foreign owned single member LLC must file a pro forma Form 1120 with Form 5472 attached, annually.

A foreign owned US corporation files Form 1120 (or 1120-F for the foreign parent).

A foreign partnership with US partners files Form 1065.

A foreign trust with US beneficiaries files Form 3520-A annually.

Get clear on which category your entity falls into before year end of your first year of operation. The deadlines, the forms, and the penalty structures are all different.

FinCEN BOI Reporting Requirements Every Foreign Owner Must Know

As of 2024, most US entities including those owned by foreign nationals are required to file a Beneficial Ownership Information (BOI) report with FinCEN (Financial Crimes Enforcement Network) under the Corporate Transparency Act.

This is brand new territory for many foreign owners, and it is separate from anything the IRS manages.

The FinCEN BOI report requires most US LLCs and corporations to disclose information about their beneficial owners: the real human beings who own or control the entity. For a standard single member LLC with one foreign owner, that means reporting the owner’s full legal name, date of birth, address, and a copy of their passport or government-issued ID.

Who must file: Most US LLCs, corporations, and similar entities. There are 23 categories of exempt entities (large operating companies, publicly traded companies, regulated financial institutions, and others), but most small foreign-owned LLCs do not qualify for any exemption.

When to file: For entities formed before January 1, 2024, the original deadline was January 1, 2025. For entities formed in 2024, the deadline was 90 days after formation. For entities formed in 2025 and beyond, the deadline is 30 days after formation.

Important: The BOI reporting situation has been subject to ongoing litigation and regulatory changes. I strongly recommend checking the current status at fincen.gov before relying on any deadline information in this or any other guide, because court orders have at various points paused and reinstated these requirements.

The penalties for failing to file when required are significant: up to $500 per day of ongoing violation for civil penalties, and potential criminal penalties for willful violations.

Your EIN is not sufficient for BOI filing. The FinCEN system is completely separate from the IRS. You file directly at boiefiling.fincen.gov, not through any IRS portal.

FAQs

Can a foreign person apply for an EIN number?

Yes. A foreign person can apply for a US Employer Identification Number by calling the IRS international line at +1-267-941-1099, faxing a completed Form SS-4 to +1-304-707-9471, or mailing Form SS-4 to the IRS international operations address in Cincinnati, Ohio. No Social Security Number is required.

How do I get a federal tax ID number without a Social Security Number?

You apply using IRS Form SS-4 via phone, fax, or mail. In Line 7b, which asks for your SSN or ITIN, write the word “Foreign.” The IRS processes these applications routinely and issues the EIN without requiring a Social Security Number from foreign applicants.

What is the difference between EIN and ITIN for foreigners?

An EIN is a business tax identification number for entities (LLCs, corporations, trusts, partnerships). An ITIN is a personal tax identification number for individuals who have US tax obligations but cannot get an SSN. Foreign business owners often need both, but for different purposes.

Can a non-US citizen be the responsible party on an EIN?

Yes. A non-US citizen can be designated as the responsible party on an EIN application. When the Form SS-4 asks for the responsible party’s SSN or ITIN, a foreign national writes “Foreign” in that field. The IRS accepts this and processes the application normally.

How long does it take to get an EIN as a foreign national?

By phone (IRS international line): immediate. By fax with return fax number provided: approximately 4 business days. By mail: 4 to 5 weeks under normal conditions, 6 to 8 weeks during peak tax season.

How to apply for EIN without SSN or ITIN?

Download Form SS-4 from IRS.gov. Complete all fields. In Line 7b, write “Foreign” where it asks for an SSN, ITIN, or EIN. Submit by faxing to +1-304-707-9471 (international applicants) or by calling +1-267-941-1099 to complete the application verbally.

Where do I fax my SS-4 form for foreign applicants?

International applicants fax Form SS-4 to +1-304-707-9471. Include a return fax number on the form so the IRS can fax your EIN confirmation back to you within approximately 4 business days.

Can a foreign owner open a US LLC and get an EIN?

Yes. A foreign national can form a US LLC in most US states (Delaware, Wyoming, and New Mexico are the most commonly chosen) and then apply for an EIN for that LLC using Form SS-4 via the IRS international line or fax. The online EIN application is not available to applicants without an SSN or ITIN, but the phone and fax methods accomplish the same result.

Do I need an ITIN before applying for an EIN as a foreigner?

No. You do not need an ITIN before applying for an EIN. The two numbers serve different purposes. An EIN application for a business entity can be completed by writing “Foreign” in the SSN field on Form SS-4. You can apply for an ITIN separately if you also need to file a personal US tax return.

What is IRS Form SS-4 and how do foreign applicants use it?

Form SS-4 is the IRS application form for an Employer Identification Number. Foreign applicants complete the same form as domestic applicants but write “Foreign” in Line 7b if the responsible party has no SSN or ITIN, and they submit by fax or phone rather than online, since the online portal requires a US taxpayer identification number to access.

What happens after I receive my foreign EIN?

After receiving your EIN, store the CP 575 confirmation letter permanently. Use the EIN to open a US business bank account, set up EFTPS for tax payments if needed, and register with any required state tax agencies. Also determine your annual IRS filing obligations, including whether Form 5472 applies to your entity if it is a foreign-owned disregarded entity.

Is there an EIN lookup tool for foreign entities?

The IRS does not provide a public EIN lookup database for privacy reasons. If you have lost your EIN, the fastest way to retrieve it is to call the IRS Business and Specialty Tax Line and request a 147C letter. Alternatively, if you previously filed any IRS correspondence or tax documents, the EIN will appear on those documents.

What is the IRS phone number for international EIN applications?

The IRS dedicated international EIN line is +1-267-941-1099. It operates Monday through Friday, 6:00 AM to 11:00 PM Eastern Time. This line is specifically for international applicants who cannot use the standard online EIN application because they lack an SSN or ITIN.

Does a foreign company need an EIN to hire US employees?

Yes. Any entity, domestic or foreign, that pays wages to US based employees must have a US Employer Identification Number for payroll tax purposes. The EIN is required before the first payroll date. There is no exemption for foreign companies that happen to hire US workers.

What is the difference between a foreign employer identification number and a foreign tax ID number (FTIN)?

A foreign employer identification number generally refers to the US EIN obtained by a foreign entity from the IRS. A foreign tax identification number (FTIN) is the tax ID number assigned by a foreign government to a business or individual in that country. These are different numbers from different governments. US financial institutions requesting an FTIN on withholding forms (like the W-8BEN-E) are asking for your home country’s tax number, not a US EIN.

A Final Word on Getting This Right From the Start

The foreign employer identification number process is genuinely manageable for most situations once you understand what the IRS actually requires and how the application methods work for non-residents.

The phone call takes less than an hour. The fax takes four days. The form itself, once you know which field to write “Foreign” in, is not complicated.

What trips people up is not the application itself. It is everything that comes after the EIN: the annual filing obligations, the Form 5472 requirements for foreign-owned disregarded entities, the FinCEN BOI reporting, and the interplay between the EIN and other compliance requirements like banking, state tax registration, and payroll.

Get the EIN right. Use it correctly. And if your situation involves a foreign trust, a multi-country ownership structure, US employees, or significant US-sourced income, bring in a CPA legal professional who specializes in international tax from the start.

For authoritative official guidance on EIN applications and international tax requirements, visit the IRS International Taxpayers page at https://www.irs.gov/individuals/international-taxpayers the primary official resource for everything covered in this guide.

This article is for informational purposes only and does not constitute legal or tax advice. Consult a qualified tax professional for guidance specific to your situation.

{kind=link}