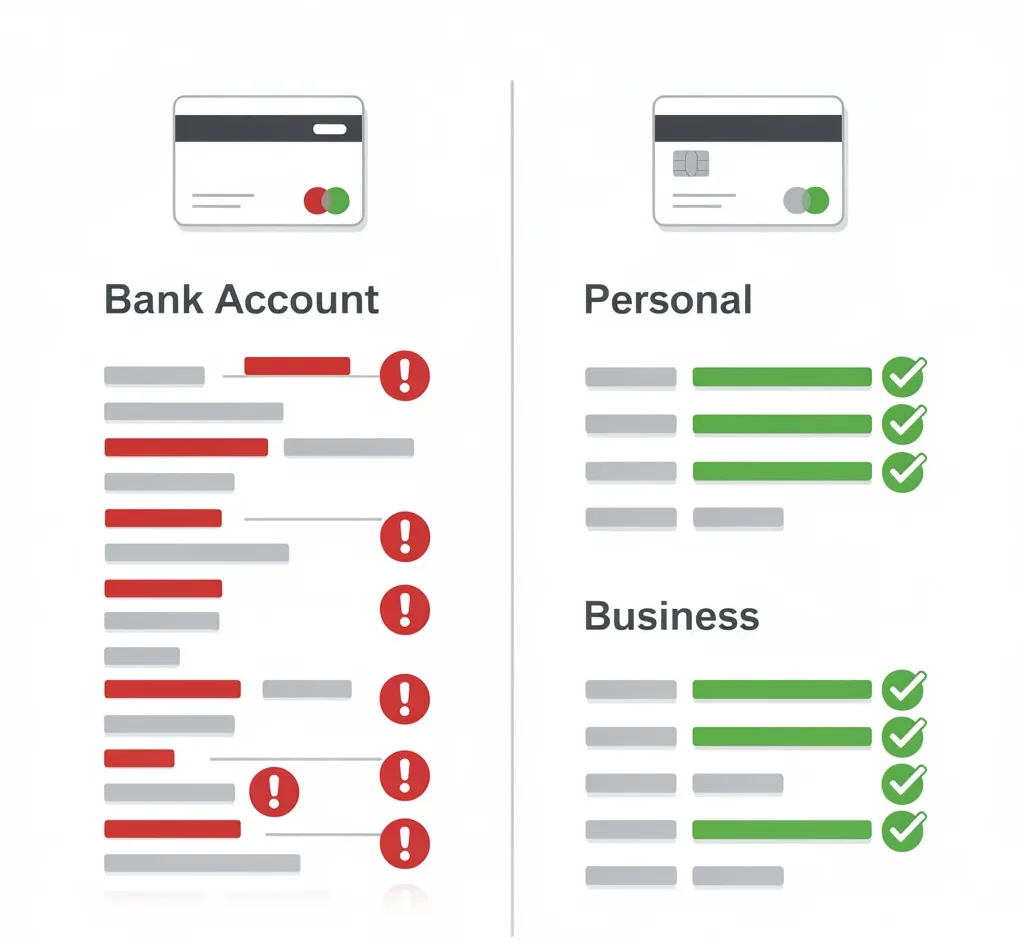

Setting up a separate bank account for your freelance business is honestly one of the smartest moves you can make as a self employed person. It sounds simple. It sounds boring. But the moment you actually do it, you will wonder why you waited so long.

Most freelancers start out tossing everything into one personal account. Client payments come in. Netflix charges go out. DoorDash orders mix with software subscriptions. And by the time April rolls around, you are sitting at your kitchen table at 11pm trying to figure out which $14.99 charge was for a stock photo site and which one was that random streaming service you forgot to cancel.

That is a miserable way to run a business. And you do not have to do it that way.

This guide covers everything you need to know about opening a separate bank account freelance business, which accounts are actually worth your time, what documents you need, and the mistakes most freelancers make that you can completely avoid.

Why Every Freelancer Needs a Separate Bank Account for Their Business

Let’s start with the honest truth. You do not legally need a separate business bank account if you are a sole proprietor. The IRS does not require it. Nobody is going to come knocking on your door.

But here is what actually happens when you keep everything in one account.

You lose track of your income. You miss deductible expenses. You stress out every tax season. You look less professional to clients. And if you ever get audited, you are in serious trouble trying to prove what was business and what was personal.

A dedicated business bank account fixes all of that in one move.

You Finally Know What Your Freelance Business Is Actually Making

This seems obvious. It really is not.

When every client payment drops into your personal account, it disappears into the flow of regular life. It becomes rent money, grocery money, weekend money. You genuinely lose the signal of what your business is producing.

The moment you separate your accounts, you can open the app and see in about ten seconds exactly how much came in, what went out for business expenses, and what is left. That clarity changes how you make every financial decision going forward.

No more guessing. No more rough estimates. Just actual numbers.

Tax Season Stops Being a Four Hour Nightmare

Filing taxes as a freelancer is already more complicated than it is for salaried employees. You are dealing with self employment tax, quarterly estimated tax payments, and tracking every single deductible expense yourself.

When all of that lives inside your personal account mixed with personal spending, you are creating a massive amount of unnecessary work. Every transaction becomes a puzzle. Was this Amazon charge a business book or a birthday gift? Was this coffee a client meeting or a Tuesday morning habit?

With a clean, separate business checking account, you pull up the transactions and hand them to your accountant. Everything in that account is business related. Done.

Most freelancers go from hours of tax prep work down to about 20 minutes once they make this switch.

If You Have an LLC, This Is Not Optional

This part is important enough that it deserves its own bold statement.

If you formed an LLC, you must have a separate business bank account.

Here is why. An LLC gives you a legal separation between your personal assets and your business liabilities. If your business ever gets sued or runs into serious debt, that structure is supposed to protect your personal savings, your car, your home.

But that protection only holds if you actually maintain the separation. Lawyers call the failure to do this piercing the corporate veil. When you run business and personal money through the same account, you blur the line so badly that a court may not respect the distinction between you and your business at all.

The legal protection you paid to create simply evaporates.

Open the account. Keep them separate. That is the whole job.

Clients Take You More Seriously

This one might feel like a small thing. It is not.

When a client sends payment to a business account in the name of your company or your business entity, it signals something. You are running an actual operation. Not a side gig. Not a hobby with a PayPal link.

One of the freelancers in a finance community I follow mentioned that a long term corporate client specifically told them that receiving invoices from a proper business account reduced friction in their internal accounting department. The client’s accounts payable team processed it faster because it looked like a legitimate vendor transaction.

Small signal. Real impact on getting paid on time.

Business Credit Starts Building From Day One

You might not care about business credit right now. That is fine.

But the day you want a business credit card, a small business loan, or a line of credit to cover a slow month, your business banking history matters. Lenders and card issuers look at how long your business account has been active and how consistently it has been used.

Every month your business account sits open and active is a month of history you are building. Start now. Thank yourself in three years.

Before You Open a Business Bank Account: Answer These Questions First

Most guides skip this part. That is a mistake. Spend five minutes here and save yourself from opening the wrong account.

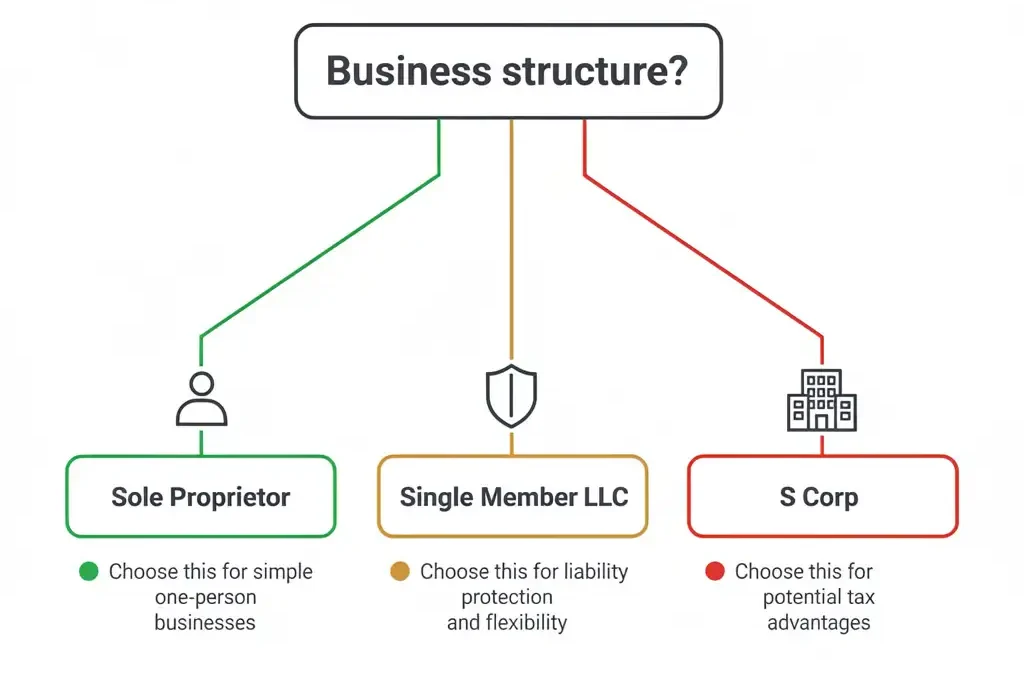

What Is Your Business Structure?

Sole Proprietor: This is the default for most freelancers who have not registered anything formally. You and your business are legally the same entity. No paperwork was required. Most freelancers are here.

As a sole proprietor, you can technically use a second personal account exclusively for business. But a free dedicated business checking account is cleaner, comes with better features, and costs nothing.

Single Member LLC: You registered an LLC. You absolutely need a real business account. This is not a suggestion.

Multi Member LLC or Partnership: You need a business account and probably a full accounting system. This guide is your starting point. Talk to an accountant.

S Corp: You have additional tax benefits because of how you structured things. Separate banking is completely non negotiable at this level.

How Much Are You Earning Right Now?

This does not change whether you should open an account. You should regardless.

But it does affect which account makes the most sense. If you are earning under $50,000 per year, a free online business account like Lili, Novo, Found, or Relay will serve you perfectly. No branch visits needed.

If you are earning more and starting to think about separating tax savings, operating expenses, and investment funds, you want something with more structure.

Do You Work With International Clients?

Not all business accounts handle international wire transfers or multi currency payments cleanly. If clients pay you in British pounds, euros, or any currency outside of USD, you need an account that handles this without charging you a fortune in conversion fees.

Wise Business is the strongest option here. More on that below.

What Accounting Software Are You Using?

If you already use QuickBooks, FreshBooks, Wave, or any other accounting software for freelancers, look for a bank account that integrates directly with it. Most modern freelance banking apps do. That integration alone saves real time every single month.

The Different Types of Accounts You Can Open

Here is where freelancers get confused. There are several categories to understand before you choose.

A Personal Account Used Only for Business

This is the bare minimum version of separation. You open a second personal checking account and you commit to using it only for business income and expenses.

Who it works for: Sole proprietors just getting started, earning very little, who want the simplest possible arrangement.

The downsides: No business specific features. Does not look as professional. Does not satisfy the separation requirement for LLCs.

It is better than mixing everything together. But it is not the best option for most people.

Free Online Business Checking Accounts

This is what I recommend for most freelancers, full stop.

Banks and fintech platforms like Novo, Lili, Found, and Relay offer free or extremely low cost business checking accounts built specifically for freelancers and solopreneurs. They include everything a solo business owner actually needs.

Here is what you typically get with these accounts:

- No monthly fees (or fees that are easily waived)

- Mobile check deposit

- Free ACH transfers

- Built in invoicing tools

- Direct integrations with QuickBooks, Xero, and FreshBooks

- Expense categorization features

- Tax savings automation on some platforms

These accounts open entirely online in under 15 minutes. No branch visit. No minimum balance. No complicated paperwork.

If you are a solo freelancer, one of these free accounts is almost certainly all you need.

Traditional Bank Business Checking

Banks like Chase, Bank of America, and Wells Fargo all offer business checking accounts. They come with the obvious advantage of physical branches and a name people recognize.

The tradeoffs are real though. Expect monthly fees of $10 to $30, minimum balance requirements to waive those fees, and product designs built for businesses with employees and payroll rather than solo operators.

Chase Business Complete Banking is the strongest traditional bank option for freelancers who genuinely need branch access. The fee is waivable with qualifying activity, and you get access to thousands of ATMs and branches nationwide.

But if you never deposit cash and do everything digitally, you probably do not need a traditional bank account at all.

Specialty Freelance Finance Platforms

Found and Lili deserve a special mention here because they go beyond a simple bank account. They function more like complete financial management systems built for self employed people.

Found automatically calculates your estimated quarterly tax liability every time income comes in and sets it aside. If you have ever hit April and thought “I owe how much right now,” this feature alone might be worth the switch. The free tier is fully functional, and the paid tier at $149 per year is competitive with what you would pay for accounting software anyway.

Lili does something similar with automatic tax savings and adds spending insights, expense tagging, and a premium tier with deeper tax optimization tools.

These platforms are genuinely useful if you are the type of person who spends first and stresses about taxes later.

Wise Business for International Freelancers

If a meaningful part of your client base pays you in currencies other than USD, Wise Business is in a completely different category.

Technically it is a Money Services Business rather than a bank, but it functions like one for almost every practical purpose. You get local bank account details in multiple currencies simultaneously. Your UK client can pay you like a standard UK bank transfer. Your European client pays via SEPA. The money arrives in the correct currency, you hold it, and you convert when you choose at Wise’s exchange rates.

I use Wise Business specifically for international client payments. The savings compared to what a traditional bank charges in conversion fees are real and consistent.

How to Open a Separate Bank Account Freelance Business: Step by Step

Let’s walk through the actual process. I am going to use Novo as the main example because it is one of the most widely used free options for freelancers, but the steps are almost identical across most online business accounts.

Step 1: Choose Your Account

Based on everything above, pick one account to start. If you are a sole proprietor who wants something free and clean, Novo, Lili, or Found are all solid first choices. If you need branch access, look at Chase. If you have international clients, add Wise Business to your setup.

Do not overthink this. You can always switch or add accounts later. The best account is the one you actually open today.

Step 2: Gather Your Documents

For Sole Proprietors:

- Government issued photo ID (driver’s license or passport)

- Social Security Number

- Home address

- Your DBA (Doing Business As) name if you operate under a business name that is not your own name

You typically do not need an EIN (Employer Identification Number) as a sole proprietor, though getting one is strongly recommended. It is free, takes five minutes at IRS.gov, and lets you use it in place of your Social Security Number for all business purposes. Less exposure of your most sensitive identifier is always better.

For LLCs:

- Government issued photo ID

- EIN (required, not optional)

- Your LLC’s Articles of Organization

- Your operating agreement (not always required but frequently requested)

For S Corps or Corporations:

- Everything above

- Corporate resolution authorizing the account

- Certificate of good standing from your state if required

Most solo freelancers are sole proprietors. Your ID and Social Security Number are basically all you need to get started.

Step 3: Complete the Online Application

For online accounts like Novo, Lili, Found, Relay, and Bluevine, the entire process happens in a browser or their mobile app. You create your account, enter your personal and business information, upload a photo of your ID, and verify your identity.

The whole process takes 10 to 20 minutes.

You will be asked for:

- Business name

- Business type (sole proprietorship, LLC, etc.)

- Industry or type of work you do

- Expected monthly deposits

- How long the business has been operating

Answer all of these honestly. There is no wrong answer for a legitimate freelance business.

Step 4: Complete Identity Verification

Most online banks use automated identity verification. You upload a photo of your ID and sometimes take a brief selfie for facial matching. This usually resolves in seconds.

Occasionally an account gets flagged for manual review, which takes a few business days. This is completely normal and nothing to worry about. It happens to legitimate applicants regularly.

Step 5: Fund the Account If Required

Some accounts require a small opening deposit of $50 to $100. Many free accounts require nothing at all.

If funding is required, you transfer a small amount via ACH from your existing personal account. Simple and fast.

Step 6: Set Up Everything Before You Use It

This is the step most guides skip entirely. Do not skip it.

Before you start routing client payments to the new account, spend 20 minutes setting things up properly.

Update your invoice template with the new routing and account numbers.

Connect your accounting software right now. Not later. The integration takes about five minutes and saves hours of manual work over the months ahead.

Set up expense categories in the app so transactions are already organized when you go to review them.

Turn on mobile push notifications for every transaction. You want real time awareness of what is moving in and out. This also helps you catch unauthorized activity fast.

Order your debit card if the account offers one. This becomes your dedicated card for all business purchases.

Step 7: Redirect All Business Income to the New Account

Contact regular clients who pay via bank transfer and give them your new account details. Update your PayPal, Stripe, and other payment platform settings to deposit into the business account.

This transition might take a pay cycle or two to complete fully. Start early so you are not manually rerouting things under deadline pressure.

Step 8: Commit to the Business Only Rule

This is the single most important rule in the entire guide. Nothing personal ever goes through this account.

No groceries. No streaming services. No splitting dinner with a friend. Not even once as a temporary thing you will fix later.

The entire value of a separate account comes from maintaining the discipline of actual separation. The moment you start mixing transactions, you have recreated the exact problem you were trying to solve.

Keep a dedicated debit card or business credit card for all business spending. Keep everything else completely out of the business account.

Building a Complete Freelance Banking System

Once you have your main account running, many experienced freelancers eventually move to a more structured setup. You do not need this from day one. But it is worth knowing about.

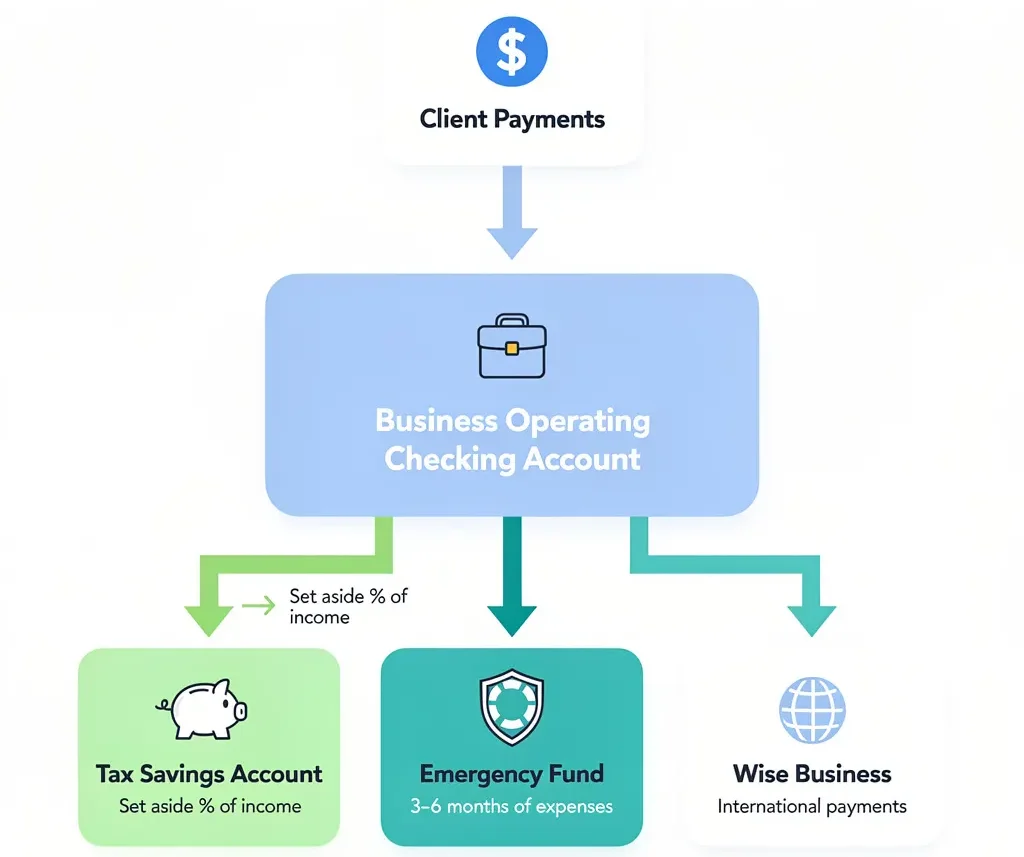

Account 1: Business Operating Checking (Novo or Relay)

This is the main account. All client income arrives here. All business expenses leave from here. Your business debit card connects to this account.

Account 2: Tax Savings Account

Every time client income arrives, transfer 25 to 30% into a dedicated tax savings account immediately. This money has one purpose: paying your quarterly estimated taxes and your annual tax bill.

I cannot overstate how much this single habit reduces financial stress. When April comes, you already have the money set aside. Tax season becomes a transaction rather than a crisis.

Account 3: Wise Business for International Payments

If you have clients paying in foreign currencies, they pay into your Wise Business account. You convert and transfer USD into your main operating account periodically.

Account 4: Business Emergency Fund

A high yield savings account holding two to three months of typical business expenses. Freelance income is inherently irregular. This buffer means a slow month does not become a financial emergency.

Start with Account 1. Add Account 2 as fast as you can. Build from there.

The Tax Side of Having a Separate Bank Account Freelance Business

I am not an accountant and this is not tax advice. But these are things I have learned from years of freelancing that are genuinely worth knowing.

You Are Responsible for Every Dollar of Your Taxes

When you work for an employer, they handle income tax withholding and the employer portion of Social Security and Medicare. As a freelancer, none of that happens automatically.

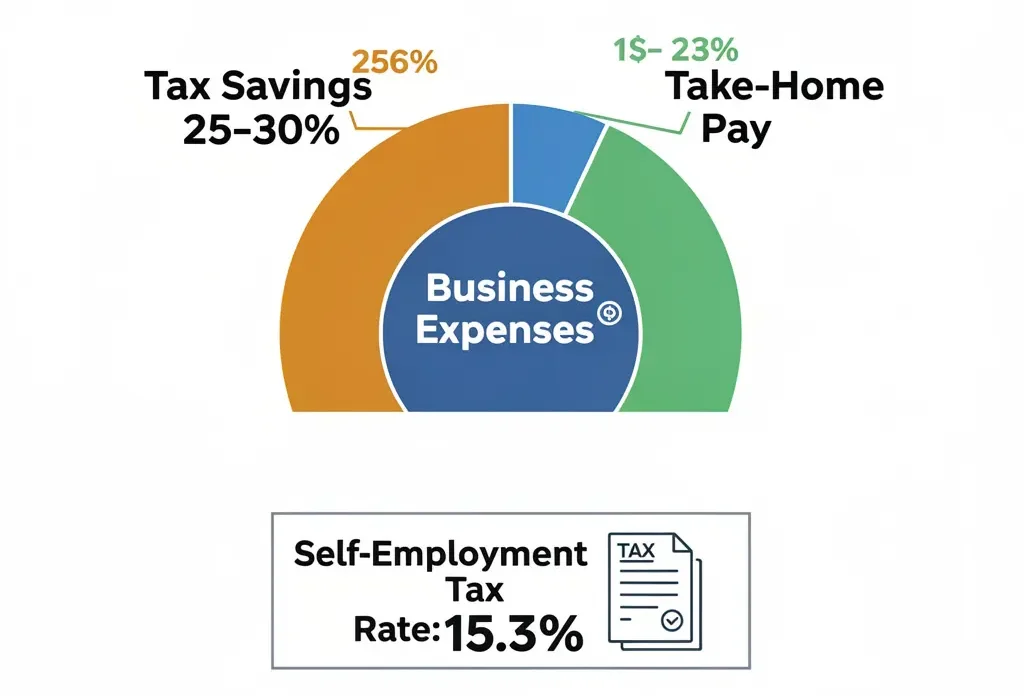

You pay self employment tax at 15.3% on your net self employment income up to the annual threshold, on top of your regular income tax rate. The IRS expects quarterly estimated payments in April, June, September, and January.

Many new freelancers get completely blindsided by this the first time they file. A large unexpected bill plus potential underpayment penalties is a genuinely rough experience.

Setting aside 25 to 30% of every payment for taxes is the standard freelancer rule of thumb. Your actual rate depends on your total income, your deductions, and your state. An accountant can give you a precise number for your specific situation.

What Counts as a Deductible Business Expense?

Once your accounts are separate, you will start actually tracking business expenses for the first time. It helps to know what qualifies.

Common deductible expenses for freelancers:

- Software subscriptions you use for work (Adobe Creative Cloud, Figma, Notion, Slack, Zoom, and similar tools)

- Equipment including computers, cameras, monitors, external drives, and microphones

- Home office deduction using either the simplified or regular method

- Internet service for the business use portion

- Phone bill for the business use portion

- Professional development including online courses, books, and industry conferences

- Health insurance premiums if you pay your own

- Retirement contributions to a SEP IRA or Solo 401k

- Business insurance

- Accountant and bookkeeper fees

- Bank fees

Every expense needs to be ordinary and necessary for your specific type of work. A dedicated account makes reviewing all of this at tax time completely straightforward.

IRS Publication 334 Actually Recommends This

This is not just advice from personal finance bloggers. IRS Publication 334, the official Tax Guide for Small Business, explicitly recommends keeping separate business accounts for record keeping purposes.

If you are ever audited, clean and separate business banking records are your strongest defense. Everything is documented. Every transaction is categorized. Your accountant can walk through the entire record clearly and quickly.

For further reading on self employment taxes and proper record keeping, the IRS Small Business and Self Employed Tax Center is the most authoritative resource available on this topic.

Common Mistakes Freelancers Make With Their Business Bank Accounts

Mistake 1: Waiting Until It Feels Necessary

The most expensive mistake on this list. Every month you wait is another month of mixed records that will eventually need to be untangled. That cleanup costs time and accountant billing hours you did not budget for.

Open the account now. Even if you are just starting out. Even if it feels premature. Early setup is always cheaper than retroactive cleanup.

Mistake 2: Choosing an Account With Unexpected Fees

The first business account I ever opened came with a $15 monthly fee waivable only by maintaining a $1,500 average balance. During a slow month the balance dipped. The fee hit. I transferred money to cover it. My tax savings calculation got disrupted.

It was completely preventable. Free online accounts built specifically for freelancers exist and they are genuinely better designed for solo operator needs. There is no reason to pay monthly banking fees as a solo freelancer.

Mistake 3: Skipping the Tax Savings Setup

This is the one that actually hurts people financially.

When I first started freelancing, I spent what came in and told myself I would handle taxes when the time came. That time came in April of my second freelance year as a $4,000 bill that went on a credit card.

Set aside a percentage of every single payment for taxes. Open a second account specifically for this purpose. Automate it if the platform supports automation. Never touch that money for anything else.

Mistake 4: Treating the Business Account Like a Personal Slush Fund

During slow stretches it is tempting to pull from the business account to cover personal shortfalls. The plan is always to put it back when the next payment arrives.

This disrupts your tax savings allocation, muddies your records, and recreates the exact problem the separate account was supposed to solve. Business money stays in the business account. Build a personal emergency fund instead so lean months do not force these decisions.

Mistake 5: Not Reconciling Monthly

I once went four months without properly reviewing my business account. I was busy. Payments were arriving. Everything felt fine.

When I finally sat down for a real review, I found a vendor had double charged me, there was an international wire fee I had not anticipated, and a subscription I had canceled was still running.

Set a recurring calendar event on the first Friday of every month. Fifteen minutes. Review every transaction. Confirm everything looks correct. This catches problems before they compound.

Mistake 6: Not Getting an EIN Early

For a long time I used my Social Security Number for every business related form. Every 1099. Every contractor agreement. Every vendor account.

Your Social Security Number is your most sensitive financial identifier. An EIN (Employer Identification Number) is free to get at IRS.gov and takes about five minutes to obtain. Use it for every business purpose instead of your Social Security Number. Fewer parties holding your most sensitive information means meaningfully less risk.

Real Scenarios Where a separate bank account freelance business Makes a Visible Difference

Scenario 1: A New Client Asks for a W 9

You land a new US based client and they need a W 9 form before they can process payment. The form asks for either your Social Security Number or your EIN.

With an EIN and a proper business setup, you fill it out in 30 seconds and send it back looking completely professional. Without one, you are giving your Social Security Number to a company whose data handling practices you have no visibility into.

Scenario 2: You Get Audited

Tax audits are uncommon for freelancers but they do happen, especially when income or deduction patterns look unusual. In an audit, the worst outcome is not that you made a mistake. The worst outcome is that you cannot prove you did not.

A clean, separate business bank account with consistent categories and zero personal transactions mixed in means your accountant can document every transaction clearly and completely. Without that separation, you are at a significant disadvantage even when everything you did was entirely legitimate.

Scenario 3: You Apply for a Business Credit Card

You want a no fee business credit card to earn cash back on business purchases and start building business credit history. The application asks for your business banking details and often reviews account history.

An established account with consistent transaction history makes this application straightforward. Without it, you are starting from zero.

Scenario 4: A Client Pays Late

A client was supposed to pay on the 15th. It is now the 22nd. You need to know quickly whether you can cover upcoming software renewals and business expenses before chasing the payment.

With a dedicated account, you check the app and have a complete answer in about ten seconds. With a mixed personal account, you are doing math across a statement full of grocery runs and coffee shops.

Scenario 5: You Bring in a Subcontractor

Your workload is growing and you want to hire another freelancer to help on a project. You need to pay them properly and you may need to issue a 1099 if you pay them more than $600 in a calendar year.

Payments from a dedicated business account make contractor records perfectly clean. Doing this from a mixed personal account is a compliance headache you do not need.

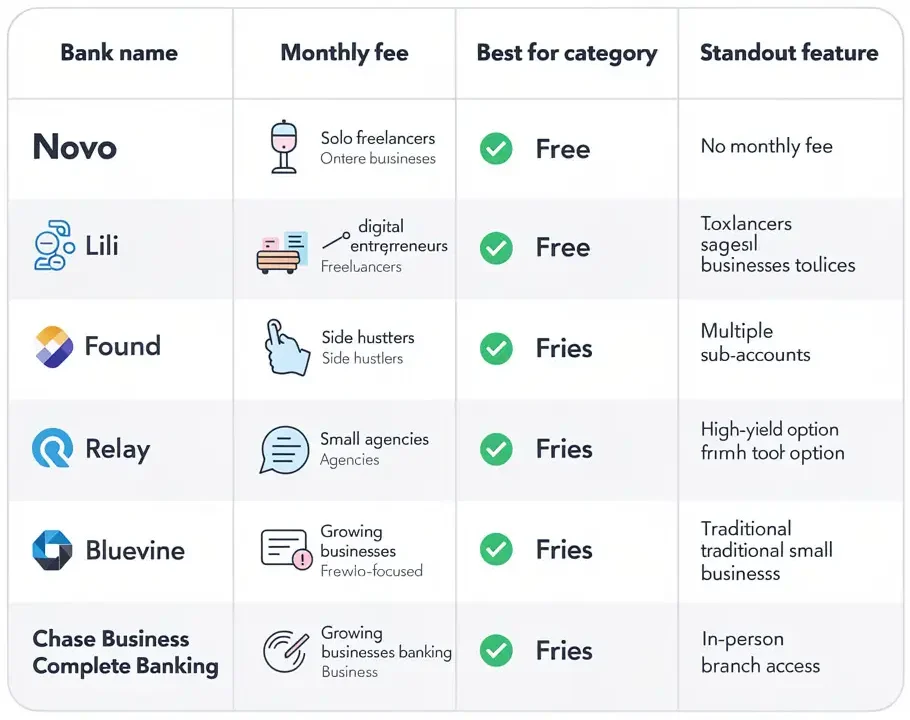

The Best Bank Accounts for Freelancers in 2026: An Honest Breakdown

Novo: Best for Simplicity and Zero Fees

Novo is completely free with no minimum balance requirements. The interface is clean and straightforward. It integrates directly with Stripe, Shopify, QuickBooks, and several other platforms. It also offers reserve accounts, which are essentially labeled sub accounts where you can earmark portions of your balance for specific purposes like taxes, a project fund, or upcoming equipment purchases.

The built in invoicing tool is genuinely functional, not just a box to check.

One limitation worth knowing: no cash deposit option and no APY on your balance.

Lili: Best for Freelancers Who Want Tax Help Baked In

Lili’s free tier is genuinely solid. Where it shines is the paid tiers at approximately $17 to $35 per month. These include automatic tax expense categorization, detailed expense reporting, and automatic tax savings that moves a percentage of every deposit into a dedicated tax sub account without you having to think about it.

If disciplined tax saving is not your natural strength, Lili essentially removes the requirement for that discipline. The system handles it automatically.

Found: Best for the Most Automated Tax Experience

Found is the most tax focused freelance banking platform on the market. It tracks deductible expenses automatically, calculates your estimated quarterly tax payments in real time as income arrives, and can file your quarterly Schedule C. The free tier is fully functional. The paid tier at $149 per year is competitive with what you would pay for standalone accounting software.

If tax management is the part of freelancing you find most stressful, Found addresses it more directly than any other option on this list.

Relay: Best for Financially Organized Freelancers Who Want a Multi Account System

Relay lets you create up to 20 separate checking accounts under a single login, each with its own debit card and its own label. This is ideal for the multi account setup described earlier in this guide. You can have your operating account, your tax savings account, your emergency fund, and any project specific accounts all visible in one dashboard.

The interface is clean and the integrations with QuickBooks and Xero are reliable.

Bluevine: Best for Freelancers Who Keep Larger Balances

Bluevine pays a competitive APY on business checking balances, currently in the range of 1.5 to 2% with qualifying monthly activity. For freelancers who consistently keep several thousand dollars in a business account, this generates meaningful passive income over time.

The platform is free, stable, and includes solid invoicing and accounts receivable management tools.

Chase Business Complete Banking: Best for Freelancers Who Need Branch Access

If you deposit cash, receive payments by check, or simply prefer the reliability of a major institution, Chase is the mainstream option that holds up well for freelancers. The $15 monthly fee is waivable with qualifying activity. You get access to thousands of branches and ATMs across the country.

It is not designed specifically for freelancers the way the fintech options are, but it is reliable and widely recognized.

Working With International Clients: The Multi Currency Banking Solution

If clients pay you from outside the United States, this section is important.

When a UK client sends you GBP to a standard US business account, your bank receives the wire, converts the currency at their own exchange rate (reliably worse than the actual mid market rate), and charges you an incoming wire fee of $15 to $35. This happens every time.

Over a year of regular international payments, those fees and conversion markups add up to real money you are simply giving away.

Wise Business solves this directly. You receive actual local banking details in multiple currencies simultaneously. Your UK client sends a standard domestic transfer in GBP. Your European client pays via SEPA in EUR. The money arrives in the original currency, you hold it, and you convert when you choose at Wise’s rates.

For freelancers with even one or two regular international clients, the platform typically pays for itself within a few months of consistent use.

Payoneer is the other widely used option for international freelancers. It integrates directly with major freelance platforms like Upwork and is particularly strong for clients in the Middle East, Southeast Asia, and Eastern Europe.

Building Good Monthly Habits After You Open the Account

Opening the account is the start. These habits are what make it actually valuable.

Weekly (5 minutes):

- Check your account balance

- Confirm expected client payments have arrived

- Flag any charges that look unfamiliar

Monthly (15 to 20 minutes):

- Review every transaction from the month

- Fix any auto categorization that landed in the wrong category

- Transfer any amount above your operating buffer to savings

- Verify your tax savings account received the correct percentage

Quarterly (1 to 2 hours):

- Calculate your estimated tax payment due

- Pay it through IRS Direct Pay or EFTPS, both of which are free and fully online

- Review your income and expense patterns for the quarter

Annually:

- Full review with your accountant

- Complete your tax filing

- Assess whether your current banking setup still fits where your business is now

Business Credit Cards: The Natural Next Step

Once your business account is running smoothly, many freelancers eventually add a business credit card to the mix.

This is not the right move for everyone. Credit cards create problems when spending discipline is not strong. But for freelancers who consistently pay in full every month, the advantages are real.

A no fee business credit card lets you earn cash back or points on business purchases, provides better fraud protection than a debit card, builds business credit history faster, and creates a completely clean record of business spending separate from your checking account.

Cards like the Chase Ink Business Cash, the Capital One Spark Cash, and the American Express Blue Business Cash are consistently popular in freelance communities for good reason. They carry no annual fee, offer solid cash back rates, and integrate well with accounting software.

The rule is non negotiable: Pay the balance in full every single month. Never carry a balance forward. The card is a tracking and rewards tool, not a credit facility.

When to Upgrade From a Free Account

Most freelancers stay on free tiers for years. That is completely appropriate.

But a few signals suggest it might be time to move to something more feature rich.

You are consistently earning over $75,000 per year. Your tax situation has real complexity now, and the cost of better tools pays for itself easily.

You want to hire contractors regularly. You need clean payment records and the ability to issue 1099s efficiently.

You are transitioning from sole proprietor to LLC or S Corp. This is a natural moment to revisit your entire banking structure.

You are keeping significant balances in an account that earns nothing. Switching to a platform like Bluevine that pays APY on balances becomes a straightforward financial decision at meaningful balance levels.

You are spending more than an hour per month on financial administration. Investing in a paid tier or better integration pays for itself in your own time.

People Also Ask: Common Questions About Freelance Business Bank Accounts

Do I Need a Separate Bank Account for Freelancing?

You are not legally required to have one as a sole proprietor. But you absolutely should have one. Mixing personal and business finances creates tax problems, makes deduction tracking nearly impossible, and can create serious legal issues if you operate as an LLC. The free online options make this a zero cost decision with immediate practical benefits.

Can I Use a Personal Account for Freelance Income?

Technically yes, if you are a sole proprietor. But this is genuinely a bad idea in practice. You lose visibility into your actual business income, you create an enormous amount of unnecessary work at tax time, and you miss deductible expenses that you could have easily tracked. Just open a free business account.

What Happens if I Mix Personal and Business Money?

Several things happen and none of them are good. You lose track of deductible expenses and pay more in taxes than you should. You create messy records that are painful to reconstruct later. If you are an LLC, you risk losing your personal liability protection entirely. And if you ever get audited, you are starting from a very weak position.

Do I Need an EIN to Open a Business Bank Account?

Most online banks do not require an EIN for sole proprietors. Your Social Security Number is typically sufficient. But getting an EIN is free, takes five minutes at IRS.gov, and removes the need to give out your Social Security Number for business purposes. Get one regardless.

How Many Bank Accounts Should a Freelancer Have?

At minimum, one dedicated business checking account completely separate from your personal finances. Ideally, two: your main operating account and a dedicated tax savings account. As your business grows, adding a high yield savings account for your emergency fund and a platform like Wise Business for international payments creates a genuinely strong financial infrastructure.

Is a Business Bank Account Worth It if I Am Only Making a Little?

Yes, completely. The free options cost nothing. There is no income level at which this stops making sense. Clean financial records and professional habits are valuable from the very first client payment you receive.

What Is the Best Free Business Bank Account for Freelancers?

Novo is the best choice for simplicity and zero fees. Found is the best for automated tax management. Lili is the best if you struggle with setting aside tax savings consistently. Relay is the best if you want a structured multi account system. The right answer depends entirely on which features match how you naturally think about money.

Can Freelancers Get Business Loans?

Yes, and having an established business banking history meaningfully improves your chances of approval. Banks and alternative lenders typically review how long your account has been open, your average monthly deposits, and the consistency of your transaction history. Starting your business account early builds this history over time.

What Is the Difference Between a Business Account and a Personal Account for Freelancers?

A business account is registered in your business name or business entity name, comes with features designed for commercial use (invoicing, expense tracking, accounting integrations), and establishes a legal separation between your business and personal finances. A personal account is registered in your individual name and carries none of those commercial features or legal distinctions.

Do Freelancers Need to Pay Quarterly Taxes?

Yes. If you expect to owe $1,000 or more in federal taxes for the year, the IRS expects quarterly estimated tax payments. These are due in April, June, September, and January. A separate bank account with a dedicated tax savings sub account makes managing this straightforward instead of stressful.

Final Thoughts: Just Open the Account This Week

A separate bank account for your freelance business is not an exciting thing. It does not feel like progress. There is no moment where everything changes dramatically.

What actually happens is quieter than that.

Tax season stops being a crisis and becomes a process. Your income becomes visible instead of abstract. Your financial records stop being a source of stress and start being a source of information. The professionalism you project to clients goes up without any extra effort.

The four hours of transaction archaeology every April becomes 20 minutes of downloading statements. The wondering whether your business is actually profitable gets replaced by simply knowing, because you can see the numbers clearly.

These are not dramatic improvements. They are quiet, cumulative ones. The kind that make a real difference over years.

If you have been putting this off, block out 20 minutes this week. Pick one account from the list above. Fill out the application. Open it.

You do not need to build the whole system today. You do not need to figure out LLC structures, quarterly taxes, and multi account setups all at once. Just get the account open, start routing your freelance business income there, and the rest builds naturally over time.

The hardest part is starting. The starting takes about 20 minutes.

Do it before the next tax season is the reason you finally did.

If you’re looking for more real world insights and practical tips to level up your freelancing journey, make sure to check out our website. We regularly share simple, actionable content to help you land better clients, protect your time, and confidently grow your freelance career.

{kind=link}