Freelancer mortgages are not some rare unicorn product reserved for a lucky few who somehow cracked a secret code.

But if you have ever watched a loan officer’s face shift the moment you said “self-employed,” you already know the system was not exactly built with people like us in mind.

I have been freelancing full time for over six years. I write about personal finance, self-employment, and homeownership because I have lived through every frustrating moment of this process. The confused loan officer. The stack of documents that was never quite enough. The polite rejection that felt anything but polite.

And then, eventually, the mortgage offer sitting in my inbox.

According to the U.S. Bureau of Labor Statistics, more than 16 million Americans currently work for themselves. Yet the traditional mortgage system still treats variable income like a giant red flag. That gap between the number of freelancers and the number who successfully buy homes is not about eligibility. It is about information and knowing where to look.

This guide fixes that.

Whether you are a freelance writer, a graphic designer, an IT contractor, a gig economy worker, or a small business owner running your own show, this article walks you through exactly how freelancer mortgages work in 2026, which lenders are genuinely good for your situation, what documents you need, and the mistakes that kill applications before they even get started.

Let us get into it properly.Which Mortgage Type Is Best for Freelancers

The Legal Documents Freelancers Need for a Mortgage Application And What They Actually Mean

Here is where the mortgage process gets real for most freelancers and where most applications fall apart before they ever reach an underwriter.

A salaried employee walks into a lender’s office with two payslips and a P60. Done. The lender has everything they need to verify income in about five minutes. As a freelancer, you are going to walk in with a folder. A large folder. And every document in that folder has a specific legal purpose that the lender’s underwriting team will evaluate carefully.

Understanding what each document represents legally not just what it is gives you a serious advantage. It means you know exactly what you are submitting, why it matters, and what to do if something is missing or unclear.

Here is what you will typically need, and the legal weight each document carries.

1. Two to Three Years of Self-Assessment Tax Returns (SA302 Forms)

In the UK, your SA302 is the official HMRC record of your declared income for a given tax year. It is the legal proof of what you earned and what you reported to the government. Lenders treat it as the most authoritative income document a self-employed person can provide because it comes directly from HMRC it cannot be altered or fabricated.

In the US, the equivalent is your filed Form 1040 with Schedule C attached. Schedule C is your official profit and loss statement as a self-employed individual. It is what the IRS has on record as your net business income after deductions.

This is where your self-employment tax filing history becomes directly relevant to your mortgage application not just to HMRC or the IRS, but to any lender evaluating your financial stability.

2. Proof of Consistent Contracts or Client Agreements

This one surprises people. Many lenders particularly those offering specialist self-employed mortgage products will ask to see evidence of ongoing client relationships. A current contract with a client that shows a retainer arrangement, a long-term service agreement, or a signed statement of work covering the next six to twelve months can materially strengthen your application.

This is not just financial evidence. It is legal documentation that your income has continuity that you are not a one-project contractor whose income may stop the moment a single client ends a relationship.

If you do not currently use written contracts with your clients, this is one of the most financially costly consequences of that habit. A verbal agreement cannot be presented to a mortgage underwriter. A signed freelance contract can. Getting your client relationships formalised in writing is not just a legal protection it is a financial asset.

3. Business Bank Statements (12 to 24 Months)

Lenders want to see that your freelance income is deposited into a dedicated business account regularly and consistently. Irregular deposits or the mixing of personal and business income in a single account raise red flags during underwriting.

From a legal standpoint, a dedicated business account also demonstrates that you operate your freelance work as a genuine business not a side activity. This distinction matters, particularly if you have set up as a sole trader or limited company, because lenders treat these structures differently when calculating eligible income.

4. An Accountant’s Certificate or Reference Letter

Many lenders especially high street banks assessing self-employed applications will ask for a reference letter from a qualified accountant confirming your income over two to three years. This letter carries legal weight because it comes from a regulated professional who is staking their professional standing on the accuracy of the figures they confirm.

If you do not currently use an accountant, this is worth reconsidering before applying for a mortgage. A certified accountant’s letter can unlock mortgage products that are not available to self-employed applicants without one.

5. Proof of ID and Address The Same as Everyone Else

Passport, driving licence, utility bills. No surprises here. This is standard legal identity verification under anti-money laundering regulations and applies to every mortgage applicant regardless of employment status.

One important note on tax deductions and mortgage applications

This is the part that catches many freelancers completely off guard.

If you have been maximising your self-employment tax deductions which is smart tax planning your net income on your SA302 or Schedule C may look significantly lower than what you actually deposited into your account each month. Lenders typically calculate eligible income based on net profit after deductions, not gross revenue.

This means a freelancer earning £80,000 a year who legitimately deducts £25,000 in business expenses may only have £55,000 of “eligible income” in the lender’s eyes. That gap can affect how much you are offered or whether you qualify for certain products.

Understanding this dynamic before you apply means you can choose between lenders that use gross revenue (some specialist lenders do) and those that use net profit, and position your application accordingly.

The legal paper trail of your freelance business your contracts, your tax returns, your invoices, your business accounts is not just compliance documentation. It is the foundation of your financial credibility. Build it carefully, maintain it consistently, and it will open doors that most lenders make look impossible for freelancers.

Can a Freelancer Get a Mortgage? Here Is the Real Answer for 2026

Yes. Absolutely. Without any question.

Freelancer mortgages exist across every major loan category, including conventional loans, FHA loans, VA loans, and a rapidly growing category called Non-QM loans that were practically invented for people in your exact situation.

The confusion comes from one fundamental problem. Lenders built their systems around W-2 employees. When a loan officer receives a payslip, they multiply it by 12 and arrive at a clean annual income figure. Simple. Neat. Easy to enter into an underwriting system.

Your income does not work like that.

Maybe you earned $65,000 one year and $92,000 the next. Maybe you had a strong quarter followed by a quieter one while you were between big projects. Maybe you write off every legitimate business expense available to you, which brings your taxable income down significantly even though your actual cash flow is healthy and consistent.

None of that makes you a risky borrower. It just means you need a lender who knows how to read your full financial picture rather than just the simplified version that fits on a payslip.

Here is something most articles will never tell you: self-employed borrowers statistically have lower default rates than many other borrower groups. Why? Because anyone who has built a sustainable freelancing income over multiple years has already demonstrated genuine financial discipline. That is exactly the kind of resilience lenders should want.

The challenge is not your creditworthiness. The challenge is knowing which lenders and which loan types actually understand that.

What Makes Freelancer Mortgages Different From Regular Mortgages

A freelancer mortgage is not a separate, specially named loan product sitting in a lender’s catalog between “conventional” and “jumbo.”

A freelancer mortgage is simply a standard residential mortgage applied for by someone who earns income through self-employment rather than a salaried position. The mortgage itself works exactly the same way. What changes is how the lender verifies and calculates your income before deciding whether to approve you.

Here is what shifts when you are self-employed:

Income verification changes completely. Instead of payslips, lenders want tax returns, bank statements, 1099 forms, and sometimes certified profit and loss statements.

Income calculation gets more nuanced. Lenders look at your net income after business expenses rather than gross revenue, or in the case of bank statement loans, your average monthly deposits across 12 to 24 months.

Income stability becomes a central concern. Lenders want to see a pattern of consistent or growing income. Two years of history carries far more weight than one exceptional year with a question mark after it.

Business longevity matters. Most lenders want to see at least two years of self-employment history. Some will work with one year under specific conditions. Very few will go below that threshold without strong compensating factors.

Understanding these differences before you walk into any lender conversation saves you enormous time and prevents the kind of frustration that sends freelancers into a spiral of Googling at midnight.

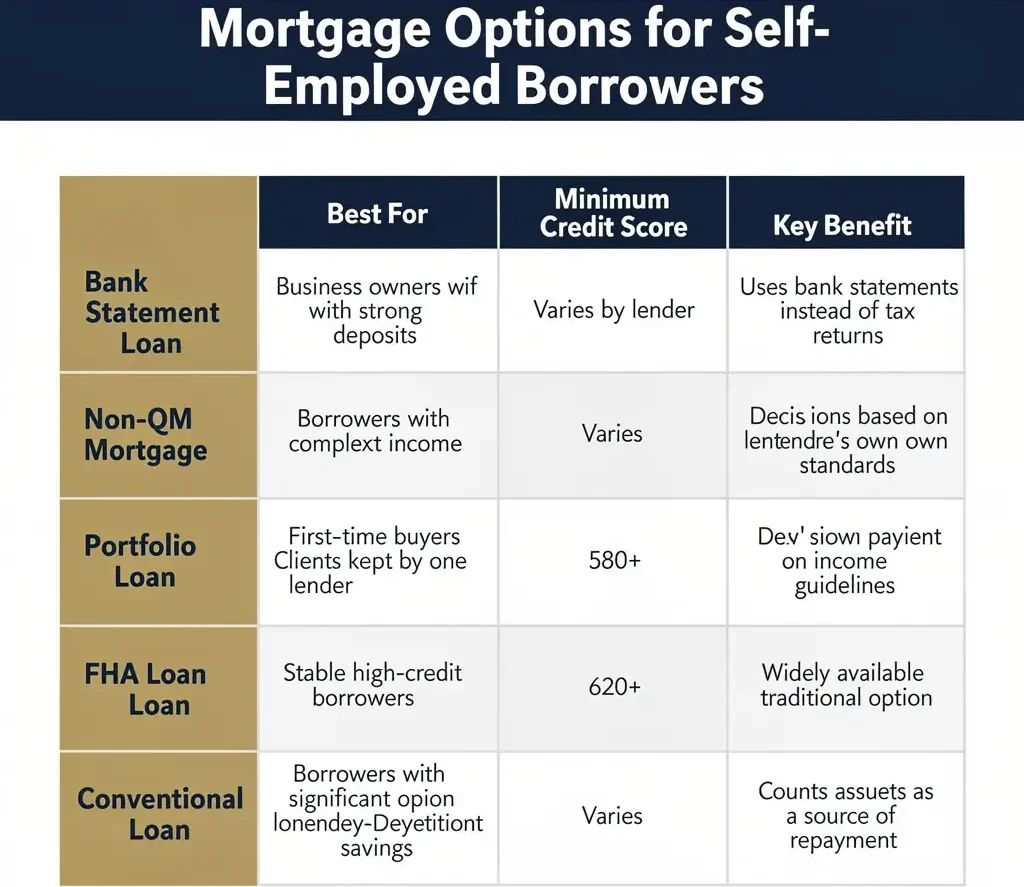

Mortgage for Self Employed Borrowers: Your Full Menu of Loan Options in 2026

This is where a lot of articles fall genuinely short. They talk about one or two loan types and leave you thinking those are your only options. In 2026, the landscape has expanded considerably. You have more paths available than most people realize.

Conventional Loans for Self-Employed Borrowers

Conventional loans remain the most common route for freelancers who have a solid two-year tax history and whose net income after legitimate deductions still paints a strong enough picture for a lender.

Fannie Mae and Freddie Mac, the two government-sponsored entities that back the majority of conventional loans in the US, have specific guidelines for self-employed income verification. Lenders following these guidelines will average your net self-employment income from the last two years of federal tax returns, including all schedules.

If your net income has been consistent or growing over that period, a conventional loan is often your cleanest and most affordable path. If your most recent year was significantly lower than the previous one, some lenders will use the lower figure, which can reduce your borrowing capacity.

What you typically need for a conventional freelancer mortgage:

Two years of personal tax returns with all schedules attached. Two years of business returns if you operate as an LLC or S-Corporation. A credit score of at least 620 for basic eligibility, though 680 or higher puts you in much stronger territory for both approval odds and rate tiers. A down payment of at least 3% for first-time buyers, though bringing 10% to 20% opens up significantly better rate options.

The debt to income ratio matters enormously here. Most conventional lenders in 2026 want your total monthly debt payments, including the new mortgage, to stay at or below 43% to 45% of your gross monthly qualifying income.

FHA Loans: A Strong Option for Freelancers With Lower Credit Scores

FHA loans are government-backed mortgages insured by the Federal Housing Administration, designed to help borrowers who might not qualify for conventional financing due to credit history or down payment limitations.

For freelancers, FHA loans offer a few specific practical advantages that matter in 2026.

The credit score floor is meaningfully lower. Many FHA-approved lenders will work with scores as low as 580 with a 3.5% down payment. The debt to income requirements are sometimes more flexible, with some lenders approving DTI ratios up to 50% in cases where compensating factors are strong.

The income documentation requirements mirror conventional loans. You still need two years of tax returns and will be assessed primarily on your net self-employment income. However, FHA-approved lenders sometimes take a more human approach to complex income situations than automated conventional underwriting systems do.

The tradeoff is mortgage insurance. FHA loans require an upfront mortgage insurance premium of 1.75% of the loan amount plus an annual premium rolled into your monthly payment. Factor this into your full cost calculations before committing to this path.

VA Loans for Freelance Veterans and Service Members

If you are an eligible veteran or active-duty service member who has gone the independent route, VA loans remain one of the most powerful mortgage products available to anyone in the US market.

No down payment requirement. No private mortgage insurance. Competitive interest rates that often beat conventional equivalents. The self-employed income documentation requirements follow similar patterns to conventional loans, with two years of tax returns being the standard expectation.

The distinctive element of VA loans is the residual income requirement. After all debt obligations are accounted for, you need to demonstrate sufficient leftover income each month based on your family size and geographic location. For freelancers with strong, documented income, this requirement is typically straightforward to meet.

Bank Statement Loans: The Real Game Changer for Freelancers Who Write Off a Lot

Here is where things get genuinely interesting for a significant portion of the freelancing community.

Bank statement loans are Non-QM mortgage products that allow lenders to evaluate your qualifying income based on 12 to 24 months of personal or business bank statements instead of tax returns.

This matters enormously because of a tension that most smart freelancers face every year.

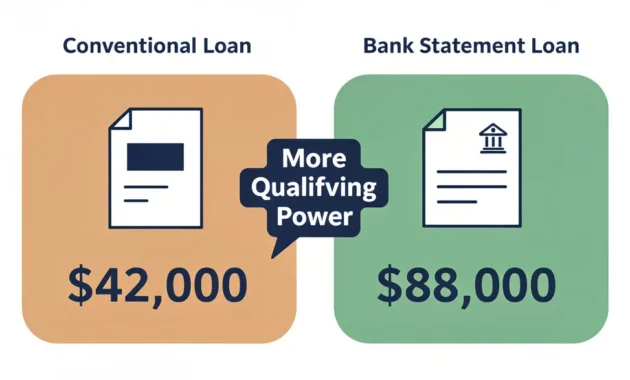

If you are running your business properly, you are claiming every legitimate deduction available to you. Home office. Equipment. Software. Professional subscriptions. Health insurance premiums. Travel with a genuine business purpose. These write-offs reduce your taxable income, which is excellent for your annual tax bill.

But when a conventional lender pulls your tax return and sees $42,000 in net income after all those deductions, they base your mortgage eligibility on $42,000. Even if your bank account shows $88,000 in actual deposits flowing through over the same period.

A bank statement loan solves this problem at the root. The lender looks at your actual verified cash flow, applies an expense ratio typically ranging from 10% to 50% depending on whether they are reviewing personal or business statements, and uses the resulting figure as your qualifying income.

For freelancers whose legitimate write-offs significantly compress their stated net income, bank statement loans can unlock borrowing capacity that conventional products simply cannot reach.

Lenders known for strong bank statement programs in 2026 include:

First National Bank of America (FNBA): Widely referenced among self-employed borrowers as a specialist in Non-QM products including bank statement loans. Their program is specifically designed for contractors, gig workers, and freelancers who do not fit the conventional mold.

Newfi: Built around flexible approaches to freelance and 1099 income, with bank statement programs that have helped borrowers who were turned away by major banks.

Truss Financial Group: Offers mortgage options specifically designed for gig workers and freelancers, with both conventional and Non-QM alternatives depending on your documentation strength.

Angel Oak Mortgage Solutions: One of the larger dedicated Non-QM lenders with established bank statement programs across multiple borrower profiles.

Citadel Servicing: An established Non-QM specialist with programs designed specifically for complex income situations.

Bank statement loans in 2026 typically carry rates 0.5% to 1.5% above comparable conventional products. But for many freelancers, the additional borrowing capacity this path unlocks makes that tradeoff worthwhile, especially since you can refinance into a conventional product later once your tax-documented income better reflects your actual earning power.

1099 Loans: Perfect for Independent Contractors and Consistent Gig Workers

A 1099 loan uses your actual 1099 forms, the tax documents your clients send instead of W-2s, as the primary income verification tool.

Rather than averaging net income from tax returns, the lender looks at your gross 1099 income and applies an expense ratio appropriate to your industry. This approach can produce a qualifying income figure substantially higher than what your net-after-deductions tax return shows.

These are Non-QM products with rate structures similar to bank statement loans. But for the right borrower profile, particularly contractors with consistent 1099 income from multiple clients throughout the year, the qualifying income calculation can be transformative.

Asset Depletion Loans: For Freelancers With Strong Savings and Investments

Less commonly discussed but worth understanding, an asset depletion loan allows lenders to count your liquid assets as a form of qualifying income.

The calculation typically works by dividing your total eligible assets, including savings accounts, investment accounts, and in some cases retirement funds, by the number of months in the loan term to generate a monthly income equivalent.

For example, if you have $480,000 across savings and investment accounts, a lender might divide that by 360 months for a 30-year loan to produce $1,333 per month in qualifying income, which they then add to any actual earned income when calculating DTI.

This is particularly relevant for freelancers who have accumulated significant savings, whose income is genuinely difficult to document cleanly in a given period, or who recently transitioned to freelancing and do not yet have two full years of history.

Self-Employed Mortgage Requirements: What Lenders Actually Need From You

Let us talk about documentation with real specificity, because this is where the majority of freelance mortgage applications either succeed or fall apart in 2026.

The number one mistake I consistently see is freelancers either assuming their situation is too complicated to bother or assuming the process mirrors what their employed friends went through. Both assumptions lead to problems.

Tax Returns: The Foundation of Conventional Loan Approval

Most lenders want the last two years of complete federal tax returns including every schedule.

For sole proprietors and single-member LLCs taxed as sole proprietors, this means Form 1040 and Schedule C, which shows your business profit and loss in detail.

For partnerships, you need your personal Form 1040 plus the partnership return Form 1065 along with your K-1 showing your distributive share of income.

For S-Corporations, you need your personal Form 1040 plus the S-Corp return Form 1120-S along with your K-1.

One critical practical note: make sure your most recent tax year is filed before you apply. If you are applying mid-year and your prior year return has not been filed yet, this creates complications that can delay or derail your application. Some lenders accept extension confirmations as evidence of a filed return, but many require the actual filed document. Plan your application timing around this reality.

SA302 Forms and HMRC Documents: For UK-Based Freelancers

For freelancers based in the United Kingdom reading this guide, the equivalent of US tax returns in a mortgage context is the SA302 form and the accompanying HMRC tax year overview.

The SA302 is your official tax calculation document downloaded directly from the HMRC Government Gateway. It summarizes your income and tax for each tax year and serves as the primary income verification document for UK mortgage lenders.

The tax year overview accompanies your SA302 and confirms that your declared taxes are actually paid or on a payment plan. Lenders in the UK market use these two documents together as the foundation of income verification for self-employed applicants. You can access both directly through your HMRC online account via the Government Gateway portal.

1099 Forms and Income Verification Documents

Gather all 1099 forms for the past two years, covering every client who paid you $600 or more in a calendar year. These serve as critical evidence that your income is real, consistent, and coming from legitimate, verifiable sources.

Lenders cross-reference 1099 totals against your tax returns. If your 1099s show $110,000 in gross payments but your tax return shows $48,000 after deductions, a knowledgeable underwriter can see both figures and understand the underlying dynamic. This also strengthens the supporting documentation for bank statement loan applications.

Bank Statements for Self-Employed Mortgage Applications

For conventional loans, lenders typically want two to three months of personal bank statements to verify your down payment source and available cash reserves.

For bank statement loans, the requirement expands significantly to 12 or 24 months of business and personal statements. Make sure these are complete official statements showing your institution’s name, your account number, and your full transaction history, not just downloaded summaries or screen captures.

If your business and personal finances currently run through the same account, some lenders will work with that arrangement. Others strongly prefer clear separation. Going forward, maintaining separate business and personal accounts is worth doing both for mortgage purposes and for your overall financial hygiene as a freelancer.

Certified Accounts for Mortgage Applications

For limited company directors, LLC owners, and partnership members, lenders typically require certified company accounts prepared and signed by a licensed CPA or accountant, usually for the last two years.

Some specialist lenders will accept accountant-prepared accounts even before they have been formally filed with the relevant government authority, but they will typically request a supporting reference letter from your accountant confirming the accuracy of the figures.

An accountant letter for mortgage purposes is a brief professional statement from your CPA confirming your self-employment status, the nature of your business, the length of your trading history, and in some cases their professional assessment of the sustainability of your income. Some lenders specifically request this as supplementary documentation.

Proof of Contracts and Ongoing Business Activity

This is not always required, but for contractors in particular, providing an active contract or recently completed contract is genuinely powerful supporting documentation.

It demonstrates to an underwriter that you are not between engagements but actively working in your field. A contract with three months remaining is evidence of near-term income stability. Multiple completed contracts over recent years demonstrate consistent demand for your skills.

Business bank account statements showing regular client payments arriving over an extended period serve a similar function for project-based freelancers who do not always operate under formal written contracts.

Freelancer Mortgage Lenders: Who Actually Gets Your Situation in 2026

Finding the right lender is not simply about finding whoever has the lowest advertised rate this week. It is about identifying the lender whose income assessment methodology actually works for your specific income structure and documentation profile.

Here is a breakdown of the lender landscape as it stands in 2026.

Major Lenders With Self-Employed Programs

Rocket Mortgage remains one of the most visited mortgage platforms in the US and handles self-employed applications through both conventional and some Non-QM pathways. Their digital process works reasonably well for straightforward self-employed cases where tax returns show clean, consistent net income. More complex situations often benefit from lenders who offer more hands-on underwriting.

Wells Fargo, Chase, and Bank of America all offer self-employed mortgage programs following standard Fannie Mae and Freddie Mac guidelines. If your tax returns show strong, consistent net income over two years and your debt to income ratio is solid, these institutions are worth considering. If your situation is more complex, their automated underwriting systems can be less accommodating than you need.

Amplify Credit Union has been specifically noted in forum discussions for their practical, human approach to evaluating self-employed buyers. Credit unions in general are worth exploring because they frequently have more flexible underwriting criteria and a genuine relationship-based approach to lending decisions. They often have the ability to make exceptions that larger, more automated institutions cannot accommodate.

Specialist and Non-QM Lenders for Self-Employed Borrowers

These are the lenders who have genuinely built their products around people in your specific situation.

First National Bank of America (FNBA) has established itself as a genuine specialist in the self-employed lending space. Their Non-QM programs are specifically constructed for freelancers, small business owners, contractors, and gig workers. They appear consistently in forum discussions from borrowers who received approvals after conventional lenders passed.

Newfi specializes specifically in mortgage options for freelancers and 1099 earners. Their bank statement loan programs are particularly strong for borrowers whose tax-documented income undersells their actual earning capacity.

Truss Financial Group markets its services directly to gig workers and freelancers with both conventional and Non-QM paths depending on which documentation approach produces the stronger qualifying income figure.

Angel Oak Mortgage Solutions is one of the largest dedicated Non-QM lenders in the US market with established bank statement, 1099, and asset depletion programs serving complex borrower profiles.

Whole of Market Mortgage Brokers: The Most Valuable Resource for Freelancers

Sometimes the most effective path is not approaching lenders directly but working with a whole of market mortgage broker who specializes in self-employed applicants and can shop your application across many lenders simultaneously.

A whole of market broker understands which lenders are currently favorable to which income profiles. They know which automated underwriting systems will likely flag your application and which lenders use manual underwriting processes where a human being actually reads the full picture. They also know which lenders have recently changed their criteria, something that outdated online articles simply cannot reflect in real time.

What to ask any broker before committing:

How many self-employed borrowers did you work with in the past 12 months? Which loan types do you most commonly place for freelancers? Do you have access to Non-QM and bank statement products? Have you worked with borrowers whose income structure looks similar to mine? What does your fee structure look like and how are you compensated by lenders?

That last question matters because brokers earn proc fees from lenders in addition to or instead of direct client fees. Understanding the compensation structure helps you assess whether the products being recommended are the best fit for you or the best fit for the broker’s commission.

How to Get a Mortgage When Self-Employed: A Step by Step Process for 2026

Let me walk you through this the way I actually did it, and the way I would approach it if I were starting from zero today.

Step 1: Pull all three of your credit reports right now.

Visit AnnualCreditReport.com and download your complete reports from Experian, Equifax, and TransUnion. Do not just check your score on one app. Look at the actual detailed reports for errors, incorrect account information, outdated collections, and anything that does not belong there. Dispute every error you find. Start this process at least six months before you plan to apply.

Step 2: Organize two years of complete tax returns.

Pull your federal returns including every schedule for the last two years. Confirm they are filed and accurate. If your most recent tax year has not been filed yet, consider whether accelerating that filing makes sense before you approach any lender. Many lenders will not process an application without your most recently filed return.

Step 3: Realistically estimate your qualifying income.

Using the two-year average method described throughout this guide, calculate what a conventional lender will see as your net self-employment income. If that figure is significantly lower than your actual cash flow because of legitimate write-offs, start specifically exploring bank statement loan options and 1099 loan programs.

Step 4: Collect 12 to 24 months of bank statements.

Even if you believe you will be taking a conventional approach, have these ready. During the underwriting process, paths sometimes shift. Being prepared for multiple documentation approaches saves significant time and prevents delays.

Step 5: Work with a mortgage broker who specializes in self-employed borrowers.

This is the single most important practical step for any freelancer with a complex income situation. A strong specialist broker will review your documentation before formally submitting any application, run a soft credit check that does not affect your score, and honestly tell you which loan types and which specific lenders are most appropriate for your profile as it currently stands. They will also flag any issues that need to be addressed before a formal application goes in.

Step 6: Get a mortgage in principle before house hunting seriously.

A mortgage in principle, also called a pre-approval, tells you your approximate borrowing capacity and signals to sellers that you are a credible buyer. For self-employed borrowers, make sure your pre-approval is based on actual document review rather than just self-reported figures. A thorough pre-approval grounded in reviewed documentation is worth significantly more than a quick online estimate generated from numbers you typed into a form.

Step 7: Submit your full application once you are under contract on a property.

With organized documentation, a specialist broker’s guidance, and a solid pre-approval in place, the full application process becomes significantly more manageable. Expect underwriters to ask follow-up questions about specific deposits, income sources, or business activities. This is completely normal for self-employed applications and does not indicate a problem.

Step 8: Respond to every underwriter request within 24 to 48 hours.

The single biggest source of unnecessary delays in self-employed mortgage applications is slow responses to document requests. Have your accountant, bookkeeper, and financial records accessible and on standby throughout the underwriting period. Delays in responding compound quickly and can push your closing timeline back significantly.

Step 9: Closing day.

You sign what feels like an unreasonable number of documents, funds transfer, and you receive the keys. This part works exactly the same whether you are employed or freelancing.

Mortgage With 1 Year Self-Employed: Is It Actually Possible?

One of the most common questions appearing in Reddit threads and Quora discussions about self-employed mortgages is some version of: “I just went freelance less than two years ago. Am I completely out of luck?”

No. You are not out of luck. But you need to approach this situation with the right strategy.

Getting a freelancer mortgage with less than two years of self-employment history is genuinely possible in 2026, though it requires the right loan type, the right lender, and typically some stronger compensating factors to offset the shorter documentation history.

Prior industry experience is a powerful argument in your favor. If you spent seven years as a salaried software engineer and transitioned to independent contracting 14 months ago, a knowledgeable underwriter can see that you did not change careers. You changed your employment structure while staying in the same field. Some lenders explicitly allow prior industry experience to be counted alongside your self-employment period when assessing stability.

Bank statement loans are often the most accessible path for newer freelancers. If you have 12 months of strong, consistent deposit history, a number of bank statement lenders will work with that documentation even without a two-year self-employed tax history.

A larger down payment compensates meaningfully for shorter history. Bringing 20% or 25% to the table reduces the lender’s exposure and opens up flexibility in how they assess your income documentation.

An excellent credit score opens doors that would otherwise stay closed. If your FICO score is above 740 and your credit file shows a long, clean history, many lenders will extend additional flexibility on income documentation in exchange for that demonstrated track record of financial responsibility.

Working with a specialist broker is especially important in the one-year situation because the lenders willing to accommodate shorter history are not always the most visible ones, and approaching the wrong lender first wastes a credit inquiry.

Contractor Mortgage: Understanding Day Rate Mortgages in 2026

Independent contractors occupy a distinctive and interesting space in the 2026 mortgage landscape, and they deserve specific attention beyond the general self-employed framework.

A contractor mortgage is a freelancer mortgage for someone who works under defined contracts with specific deliverables, timelines, and rates rather than ongoing flexible client arrangements. Contractors often have a characteristic financial profile that creates both challenges and opportunities in the mortgage application process.

They frequently operate through an LLC or S-Corporation for legitimate tax efficiency, keeping their formal personal income through salary plus dividends at a level that looks understated relative to their actual generating capacity. Their work is typically measurable and verifiable, with defined rates and documented deliverables. Their actual earning power, when you look at the contracts themselves, can be substantially higher than their tax return figures suggest.

Mortgage Based on Day Rate: How the Calculation Works

The day rate mortgage method is specifically designed to address this gap between what a contractor earns and what their tax-optimized income documents show.

Rather than relying on tax return net income, lenders using this approach calculate an annualized income equivalent from the contractor’s daily or hourly rate.

The typical formula is: Daily rate multiplied by 5 working days multiplied by 46 or 48 working weeks equals annual income equivalent.

If your verified day rate is $600, that calculation produces: $600 x 5 x 48 = $144,000 as the annual qualifying income figure.

For a contractor whose tax-efficient compensation structure might show $55,000 to $65,000 on their return, this difference in qualifying income is transformative for their borrowing capacity.

Requirements for day rate mortgage qualification:

An active contract or one completed within the last three to six months as documentary evidence. At least two years of consistent work within the same professional field, demonstrating that your contracting is an established career rather than a recent experiment. A verifiable, documented day rate supported by invoices, signed contracts, or agency confirmations. Clear professional continuity showing you have remained in your area of expertise.

Umbrella company contractors in the UK market sit in a slightly different position. Working through an umbrella company means you technically receive a payslip as an umbrella company employee. This can actually simplify certain aspects of conventional mortgage qualification, though specialist lenders who understand the umbrella structure are still valuable for maximizing your assessed income.

Self-Employed Mortgage Without Two Years Accounts: Special Situations and Solutions

Let us look specifically at the scenarios where the standard two-year documentation requirement is genuinely challenging and what your realistic options are.

Recently Transitioned From Employment to Freelancing

This is perhaps the most common situation. You left a traditional job, possibly quite a well-paid one, and started freelancing within the last 12 to 18 months. Your income is comparable or better than it was, but your tax history as self-employed is limited.

Your best documentation approach:

Gather your final employment records showing your previous salary and job title. Prepare bank statements from the full period of your freelancing showing consistent client income deposits. Get a CPA to prepare a year-to-date profit and loss statement for your current freelancing activity. Emphasize the continuity of your professional field in any cover letters or broker communications.

The bank statement loan category, combined with a specialist broker who can articulate your transition narrative to the right lender, gives you the strongest realistic path in this situation.

Sole Trader Mortgage Applications

A sole trader mortgage follows the standard self-employed path but with some specific documentation characteristics worth understanding.

As a sole trader, your business income and personal income are legally the same thing. Your tax return, specifically Schedule C in the US or your SA302 and self-assessment return in the UK, shows your business income and expenses in detail. Lenders assess your net profit after all business expenses as your qualifying income.

The consistent challenge for sole traders is the expense deduction dynamic described earlier. Heavy but legitimate write-offs in your Schedule C reduce the net profit figure lenders use, which can create a meaningful gap between your actual financial position and your mortgage-qualifying income.

Some lenders will add back certain non-cash deductions such as depreciation when calculating your qualifying income, which can help restore some of that gap. Ask specifically about add-back policies when evaluating lenders.

Limited Company Director Mortgage Applications

Running your freelancing through a limited company creates a more complex income picture that requires lenders who specifically understand the structure.

The typical limited company director setup involves paying yourself a relatively small salary, often at or just above the personal allowance threshold to minimize National Insurance or payroll tax obligations, and then taking the remainder of your compensation as dividends. This is completely legitimate tax planning but looks unusual to automated underwriting systems that simply see a low salary.

What specialist limited company director mortgage lenders will assess:

Your total compensation including both salary and dividends. Potentially your share of retained profits sitting within the company, which technically belongs to you as the sole or majority director-shareholder. The overall health and trajectory of your company accounts.

Getting a lender who will include retained company profits in their income assessment can significantly increase your qualifying income figure and therefore your maximum borrowing capacity.

Self-Employed Mortgage Deposit: How Much Do You Actually Need?

Deposit requirements for self-employed mortgage applications broadly mirror those for conventional employed borrowers, but the practical strategic reality for freelancers differs in important ways.

The minimum deposit thresholds are:

Conventional loans: 3% to 5% for first-time buyers, 5% to 10% for repeat buyers.

FHA loans: 3.5% with a 580 or higher credit score, 10% with a score between 500 and 579.

VA loans: 0% for eligible veterans and service members.

Non-QM and bank statement loans: Typically 10% to 20% minimum, sometimes higher depending on the lender and your overall credit profile.

The strategic reality for self-employed borrowers is this:

A larger down payment serves two simultaneous purposes. It reduces your monthly payment and eliminates private mortgage insurance at 20% down on conventional loans. But more importantly for freelancers, it compensates for the complexity of your income documentation in the eyes of the underwriter. A 25% down payment opens up significantly more lender options and more flexibility in how they assess irregular income documentation.

If you are currently saving for your deposit, think carefully about whether waiting an additional few months to cross a meaningful threshold, moving from 10% to 15% or from 15% to 20%, is worth the improved option set and potentially better rate that follows.

Government programs worth knowing about in 2026:

The FHA loan program, discussed earlier, remains one of the most accessible government-backed paths for self-employed first-time buyers who cannot bring a large deposit. VA loans continue to offer the zero down option for eligible service members. Various state-level housing finance agency programs offer down payment assistance that can sometimes be layered with FHA or conventional loans. Check your specific state’s housing finance agency for current programs available in your area.

Freelancer Income Verification Mortgage: Building the Strongest Possible Document Package

Freelancer income verification for a mortgage goes beyond simply gathering documents. It is about presenting a coherent, consistent financial narrative that a lender or underwriter can follow clearly without confusion or gaps.

Here is how to build that narrative deliberately.

Consistency across all documents is non-negotiable. Your 1099 totals should align logically with your tax return income. Your bank deposit history should tell a story consistent with your stated client income. Your CPA-prepared profit and loss statement should reflect patterns visible in your banking activity. When these documents tell conflicting stories, even accidentally, underwriters flag the discrepancy and the questions multiply.

Gaps in income need context, not concealment. If you had a quiet quarter during which a major client delayed a large invoice, or if you took three months off for a health matter, document it. A brief explanatory letter from you or a note from your accountant addressing a specific gap is far better than an underwriter sitting with unanswered questions about why your deposits dropped significantly for three months.

Separation of business and personal finances makes everything cleaner. A dedicated business bank account means your business income is clearly traceable without personal transactions muddying the picture. This is valuable both for bank statement loan documentation and for the general clarity of your financial records when an underwriter reviews them.

An accountant who understands mortgage applications is a strategic asset. Some CPAs specifically have experience preparing self-employed clients for mortgage applications. They know which line items lenders scrutinize, they understand the add-back policies for non-cash deductions, and they can prepare supplementary documentation like projections letters or income trend analyses that some lenders will consider as supporting evidence.

Freelancer Mortgage Mistakes That Kill Applications Before They Start

Let me go through the most damaging ones clearly, because I have seen every single one of these either personally or through conversations with other self-employed borrowers.

Applying to the Wrong Lender First and Taking a Hard Credit Inquiry

Every formal mortgage application triggers a hard credit inquiry that shows up on your credit file and can affect your score. If you apply to a lender who was never going to approve you due to their rigid self-employed income criteria, you have taken a credit score hit for nothing and your application history now includes a declined file.

A specialist broker running a soft pre-assessment before any formal application protects you from this entirely. Multiple mortgage hard inquiries within a 14 to 45 day window are typically treated as a single inquiry by the credit bureaus under the rate shopping exception, but this window is narrower than most people assume.

Inconsistent Documentation That Raises Red Flag Questions

Lenders cross-reference extensively. Your 1099 forms against your tax return. Your tax return against your bank statements. Your bank statements against your stated monthly income. Your company accounts against your personal income declarations.

If these documents tell inconsistent stories, even for explainable reasons, underwriters pause the file and ask questions. Enough questions means delays. Enough delays or unresolved discrepancies means denial.

Build your document package so that everything tells a consistent, coherent story before a single piece of it reaches a lender’s desk.

Over-Optimizing Tax Write-Offs in the Years Before Your Application

This is the core freelancer mortgage tension and there is no single right answer. Claiming every legitimate deduction minimizes your tax liability, which is smart financial behavior. But those deductions reduce the net income figure that conventional lenders use to calculate your borrowing capacity.

If you are planning a mortgage application within one to two years, have a specific conversation with your accountant about this balance. Some freelancers choose to be more conservative with borderline deductions in the tax years they plan to use for mortgage documentation. This is legitimate tax strategy applied with your full financial goals in mind, not gaming the system in any problematic sense.

For freelancers who have already heavily optimized their deductions, bank statement loans or 1099 loans offer the path around this challenge.

Changing Your Business Structure Right Before Applying

Moving from a sole proprietorship to an LLC, from an LLC to an S-Corporation, or making any significant structural change to how your business is organized right before a mortgage application effectively resets your business history clock from the lender’s perspective.

You might have been operating productively and profitably for six years, but if you incorporated three months ago, some underwriting systems will treat your LLC as a three-month-old entity.

Plan any structural changes at least one to two years before you want to apply for a mortgage. If you are considering restructuring for tax efficiency, do it now so the history has time to build before you need it.

Assuming One Rejection Is a Final Verdict on Your Borrowing Eligibility

A rejection from one lender, particularly a mainstream one with automated underwriting, is information about that specific lender’s criteria. It is not a universal judgment on your creditworthiness.

The freelancer who got turned down at two major banks and then received approval through a specialist lender or credit union is not an unusual story. It is actually a very common one. The mortgage landscape has multiple tiers of lenders with genuinely different criteria, and the right fit for a complex income profile often exists well outside the institutions you first approached.

One no is a redirect. It is not a verdict.

How to Improve Your Freelancer Mortgage Chances: Practical Steps That Work in 2026

Beyond avoiding mistakes, here are proactive actions that genuinely move the needle.

Build a substantial cash reserve above and beyond your down payment. Having three to six months of projected mortgage payments in accessible savings demonstrates stability to an underwriter. It signals that even if your income dipped for a quarter, you have the buffer to keep meeting your obligations. This is also simply good freelancer financial practice regardless of mortgage applications.

Reduce existing debt before applying. Every dollar of monthly debt payment you eliminate improves your debt to income ratio. Pay down credit card balances particularly aggressively, especially any accounts carrying balances above 30% of their credit limit. Reducing utilization below 30% and ideally below 10% has a measurable positive effect on your credit score as well.

Maintain a diversified and stable client base. Heading into a mortgage application with income coming from multiple established clients looks more stable than relying heavily on one large project or one primary client relationship. Diversified income sources signal business resilience to an underwriter.

Separate your business and personal finances completely. If you are not already using a dedicated business checking account, open one immediately. Clean financial separation makes your income traceable and your documentation credible.

Register on the electoral roll or update your address records across all accounts. Address consistency across your credit file, tax documents, bank accounts, and mortgage application is a small but meaningful factor. Discrepancies in address history slow underwriting and occasionally raise questions you would rather not have to explain.

Consider working with an accountant who understands the mortgage context. A good accountant for a self-employed homebuyer prospect is not just someone who minimizes your tax bill. They understand the balance between tax efficiency and mortgage eligibility, they can prepare clear and lender-appropriate documentation, and they can write a strong accountant’s reference letter when a lender requests one.

Mortgage Protection Insurance: The Coverage Freelancers Cannot Afford to Overlook

One thing that comes up consistently in the mortgage process that freelancers routinely underestimate: the absence of employment-based financial protection once you become a homeowner.

When you work for an employer, you typically have access to disability insurance, paid sick leave, and sometimes life insurance or death-in-service benefits. These protections exist specifically to ensure you can continue meeting financial obligations if something goes wrong with your health or your life.

As a freelancer, you have none of these automatically. If you were ill or injured and unable to work for three months, your mortgage payment still arrives on exactly the same schedule it always did.

Income protection insurance replaces a defined proportion of your income, typically 50% to 70%, if you are genuinely unable to work due to illness or injury. For a self-employed homeowner, this is not optional coverage in any meaningful sense. It is the structural foundation that makes homeownership safe rather than precarious.

Mortgage protection life insurance pays out an amount sufficient to cover your outstanding mortgage balance in the event of your death. Many policies are structured so the coverage amount decreases over time in line with your reducing mortgage balance.

Critical illness cover provides a lump sum payment upon diagnosis of specific serious illnesses. For a freelancer whose income would stop immediately with a serious diagnosis, this coverage can protect both the mortgage and the broader financial stability of the household.

These products are distinct from your mortgage but should be considered alongside it as part of your complete financial picture as a self-employed homeowner.

Using Technology to Make Your Mortgage Application Smoother

Being organized is a competitive advantage in the self-employed mortgage process. The right tools make that organization significantly easier to maintain.

Accounting software creates the clean financial records that support mortgage applications. QuickBooks Self-Employed, FreshBooks, and Wave are all solid choices for freelancers who want organized, consistent financial records. When your profit and loss data is cleanly maintained throughout the year, producing documentation for a mortgage application becomes a matter of extraction rather than reconstruction.

Separate business banking platforms streamline everything. Relay, Mercury, and Novo are business banking options that work well for freelancers and produce clean, detailed statements with clear transaction descriptions. This makes bank statement loan documentation far more straightforward than personal accounts often can be.

NMLS Consumer Access at nmlsconsumeraccess.org allows you to verify that any lender or broker you are considering is properly licensed in your state. Never work with an unlicensed mortgage professional regardless of how persuasive their pitch sounds.

Open Banking tools are increasingly relevant in 2026. Some lenders now accept authorized read-only access to your transaction data rather than requiring physical statement uploads. This technology is more developed in the UK market currently but is expanding in the US and can significantly accelerate the documentation review phase of underwriting.

Remortgaging as a Self-Employed Borrower: What Happens When Your Initial Deal Ends

Getting your first mortgage is the major summit. Remortgaging when your initial deal expires is more like a significant but manageable hike you have now done before.

When your fixed rate period ends, typically after two, three, or five years depending on your initial product choice, you either need to remortgage to a new competitive rate or roll onto your lender’s standard variable rate, which is almost always higher.

For self-employed borrowers, remortgaging requires updated income documentation. Your most recent two years of tax returns. Current bank statements. Any other income verification documents your new lender requires. The process is shorter than the initial purchase because there is no property search or purchase negotiation. But it is not passive.

The good news for freelancers remortgaging: by this point you have a demonstrated track record of meeting your mortgage obligations on time. That track record, combined with potentially stronger income documentation after two to five more years of growing self-employment history and a potentially improved credit score from consistent on-time payment behavior, often puts you in a meaningfully better position than your initial application.

Start actively researching remortgage options three to six months before your current deal expires. Use a specialist broker to compare across the full market rather than simply defaulting to whatever retention product your current lender offers. Lender loyalty is rarely rewarded in the mortgage market.

Self-Employed Mortgage Application Checklist: Everything Organized in One Place

Use this as your complete reference before submitting anything.

Income Documentation

Two years of complete federal tax returns including all schedules. Two years of business tax returns if you operate as an LLC, S-Corporation, or partnership. All 1099 forms for the past two years covering every client source. Year to date profit and loss statement prepared or signed by a licensed CPA. Business license or equivalent proof of business existence where applicable.

Banking and Financial Records

Two to three months of personal bank statements for conventional loan applications. Twelve to 24 months of personal and business bank statements for bank statement loan applications. Investment and brokerage account statements if using assets as income or reserves. Retirement account statements where relevant.

Credit and Personal Identification Documents

Government-issued photo identification. Social Security number for credit authorization. Current proof of address through a utility bill or similar document. Any relevant legal documents affecting income such as divorce decrees or child support orders.

Property and Transaction Documents

Accepted purchase offer or sales contract once you are under contract. Landlord contact details for rental history verification if applicable. Evidence of homeowners insurance arranged or in progress.

Frequently Asked Questions About Freelancer Mortgages in 2026

Can a freelancer get a mortgage?

Yes. Freelancers can qualify for conventional, FHA, VA, bank statement, 1099, and asset depletion loans. The key is matching your specific income documentation to the right loan type and lender through a specialist broker.

How do freelancers prove income for a mortgage?

Through two years of federal tax returns, 1099 forms, bank statements, and CPA-prepared profit and loss statements. For bank statement loans, 12 to 24 months of deposit history replaces tax returns as the primary income verification.

How many years do you need to be self-employed to get a mortgage?

Most lenders require two years. Some bank statement lenders and specialty products work with 12 months of history when compensating factors like a high credit score, large down payment, or strong prior industry experience are present.

What is the SA302 and do US borrowers need it?

The SA302 is a UK-specific HMRC tax document used for self-employed mortgage applications in Britain. US borrowers use Form 1040 with all schedules and business returns as the equivalent income documentation.

How much can a freelancer borrow for a mortgage?

This depends on your verified qualifying income, credit score, debt to income ratio, and down payment amount. Most conventional lenders apply a maximum DTI of 43% to 45%. A specialist broker can calculate specific numbers based on your actual documentation.

Can I get a mortgage with one year of self-employment?

Yes, in some cases. Bank statement loans, specialty Non-QM products, and FHA loans with strong compensating factors can accommodate one year of self-employment history, particularly with prior professional experience in the same field.

Do freelancers get rejected for mortgages more often?

Freelancers face higher rejection rates at mainstream automated underwriting systems. However, many of those rejections are resolved by working with a specialist broker to identify appropriate lenders. A rejection from one institution is not a final verdict.

What is the best mortgage for a freelancer who claims lots of deductions?

Bank statement loans or 1099 loans, because these qualify you based on actual cash flow or gross 1099 income rather than net taxable income after deductions. These Non-QM products were built specifically for this situation.

Is it harder to get a mortgage as a freelancer?

The process requires more documentation and more strategic lender selection than a W-2 application. For a freelancer with two or more years of consistent income, good credit, and proper preparation, approval is genuinely achievable through the right channels.

What credit score do I need for a freelancer mortgage?

Conventional loans require 620 minimum, with 680 to 740 unlocking better rate tiers. FHA loans start at 580. Non-QM and bank statement loans typically require 620 to 660, with some lenders accommodating lower scores given strong compensating factors.

Can a contractor get a mortgage based on their day rate?

Yes. Specialist lenders use the annualized day rate rather than tax return income to calculate qualifying income for established contractors. This requires a verifiable rate, an active or recent contract, and continuity in your professional field.

Should a freelancer use a broker or go direct to a lender?

A whole of market broker specializing in self-employed borrowers is almost always the better choice for complex income situations. They know which lenders are appropriate for your profile before you apply, protecting your credit from unnecessary hard inquiries.

Final Thoughts on Freelancer Mortgages in 2026

I have spent considerable time writing this guide because when I was sitting across from that mortgage advisor years ago feeling completely lost, I would have given a lot for something this specific and honest to exist.

The freelancer mortgage process is harder than it needs to be. The system genuinely was not built for people who work independently, and navigating something that was not built for you requires more preparation and more strategic thinking than following the standard path.

But here is what I want you to hold onto from everything you have read here.

Your income structure is not a liability. It is just a different kind of asset that requires the right interpreter to be properly understood.

The right broker who works with self-employed clients regularly. The right loan type that matches how your income actually appears on paper. The right lender whose underwriting criteria were built with your situation in mind. The right documentation prepared clearly and presented consistently.

Those four things together do not just make freelancer mortgages possible. They make them straightforward.

Start with your credit reports. Organize your tax documents. Find a specialist broker before you start property hunting. And do not let one rejection from one institution with one rigid automated system tell you something untrue about your ability to own a home.

You have already built something sustainable enough that you are in a position to want to buy a house. That is genuinely not easy. The mortgage process will test your patience. But the foundation, a real career with real income that you built entirely for yourself, is already there.

Now go find the people who can see that clearly.

This article is written from personal experience and provided for general informational and educational purposes only. It does not constitute professional financial, tax, or legal advice. Mortgage products, eligibility requirements, lender criteria, and interest rates change frequently. Always consult with a licensed mortgage professional or qualified financial advisor before making decisions related to any mortgage or home purchase. For official US income documentation guidance, visit IRS.gov. For consumer financial protection resources, visit ConsumerFinance.gov.

{kind=link}