The Wake-Up Call Nobody Warns You About

Freelancer taxes for beginners is the topic nobody hands you a guide on when you quit your job and start working for yourself. I found that out the hard way.

My first year of freelancing felt like straight-up winning. I left my office job in March, picked up three clients by May, and closed out December having earned more money than I ever had on a salary. I was genuinely proud of myself.

Then April showed up.

My accountant, who I only hired because my dad threatened to disown me, looked at my numbers and quietly told me I owed just over $9,400 in federal taxes. I had saved exactly $1,800. She did not laugh. But I could tell she was working hard not to.

That moment cracked something open in me. I spent the next year obsessively learning how freelance taxes actually work, and I have not had a nasty surprise since. What follows is everything I picked up along the way, written the way I needed someone to explain it when I was sitting across from that accountant with an empty savings account and a very red face.

Quick Note: This article covers US freelancers specifically. The rates, forms, and deadlines are all American. If you are outside the US, the exact numbers differ, but the core logic of setting money aside and paying on a schedule applies almost everywhere. This article is for informational purposes only. For advice specific to your situation, consult a licensed CPA or enrolled agent.

How Freelance Taxes Actually Work

When you had a regular job, taxes were boring in the best possible way. Your employer pulled money from every paycheck, handled the paperwork, and by April you probably got a small refund dropped back into your account. Taxes just happened. You were barely involved.

Freelancing removes that entire system in one move.

Nobody withholds anything from your payments. Whether you are a freelancer, independent contractor, or gig worker, when a client sends you $3,000, you receive $3,000. It feels great in the moment. But the IRS still expects its cut, and you are now responsible for calculating that cut and sending it yourself, on a schedule you also have to manage.

Three things need to live in your head before anything else in this article makes sense.

First: you pay two separate taxes. Regular income tax, the same one every working American pays, plus a self-employment tax that covers Social Security and Medicare. Most new freelancers do not know the second one exists until they get their first tax bill.

Second: you pay four times a year. The IRS runs on a pay as you go system. You send estimated payments throughout the year, not just in April. Miss those payments and you owe a penalty on top of whatever you already owe.

Third: you report everything on Schedule C. As a sole proprietor, which is the default structure for most freelancers who have not formed an LLC or corporation, Schedule C is the form where you list your business income and subtract your business expenses. Think of it as a profit and loss statement attached to your Form 1040. Less intimidating once you see it.

Also worth knowing: most clients who paid you $600 or more in a calendar year will send a 1099-NEC form in January. Platforms like PayPal or Upwork may send a 1099-K instead. Both report income you are required to claim on Schedule C. The difference matters for how you reconcile the numbers but not for whether you owe tax.

The Self-Employment Tax (The Sneaky Extra One)

This is the part that blindsided me personally, and it catches almost every new freelancer off guard at least once.

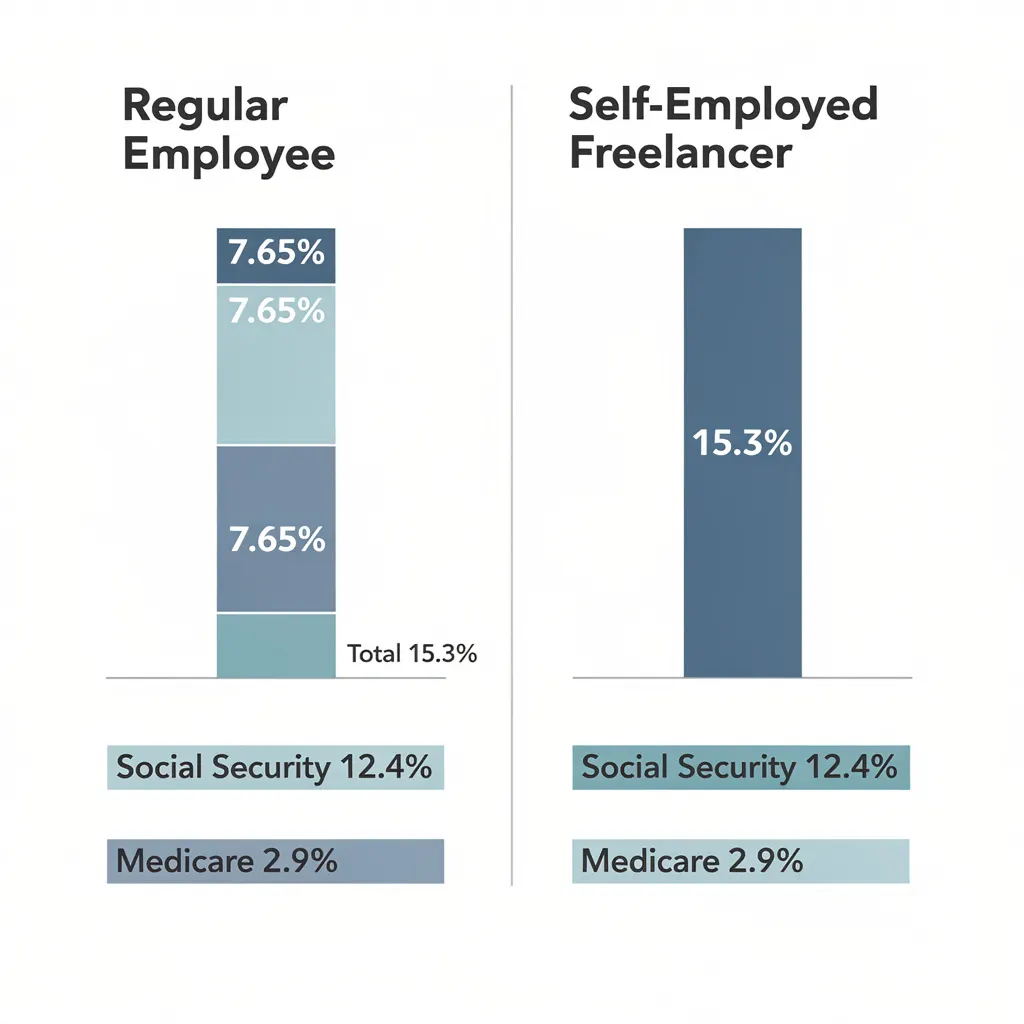

When you worked a regular job, your employer paid half your Social Security and Medicare taxes. Those are called FICA taxes, and freelancers must cover them in full, unlike salaried employees who split the cost with their employer. You paid the employee half, 7.65%, and it vanished from your paycheck so quietly you probably never thought about it.

When you are self-employed, you pay both halves. That is the self-employment tax, and the IRS sets it at 15.3% of your net earnings on top of your regular income tax, per IRS Publication 334. It is composed of 12.4% covering Social Security and 2.9% covering Medicare.

Three numbers you need to know cold: the SE tax rate is 15.3%. The minimum net income that requires you to file is $400. And roughly half of what you pay in SE tax can be deducted from your income when calculating your regular income tax. That deduction does not erase the pain, but it takes a real bite out of it.

One thing most beginner guides skip: the 12.4% Social Security portion of the self-employment tax only applies to the first $168,600 of net earnings in 2026. Above that threshold, you only pay the 2.9% Medicare portion. High earners see their effective SE tax rate drop meaningfully once they cross that line.

Here is what the actual numbers look like on a real income. Say you earned $60,000 net from freelance work in 2026. Your self-employment tax would be roughly $8,478, calculated as 15.3% applied to approximately $55,400 after the adjustment the IRS allows. On top of that, your adjusted gross income after the SE tax deduction gets hit with federal income tax, which runs most people another $6,000 to $10,000 or more depending on deductions and bracket. Your total tax liability as an independent contractor: somewhere between $14,000 and $18,000 before your state takes its share.

I sat across from my accountant looking at a number in that range with $1,800 in my savings account. Knowing the number exists before it arrives is the entire point of reading this.

Quarterly Taxes: The System That Trips Everyone Up

Most new freelancers hear the phrase quarterly taxes and assume it is some kind of optional early-bird system. Pay ahead, earn a gold star. Skip it, nothing happens.

Nothing happens until the IRS sends a penalty notice. Then things happen quickly.

Missing quarterly payments triggers an underpayment penalty. Not catastrophic on its own, but it compounds, it is completely avoidable, and it tends to land right when you are already stressed about money. The IRS runs a pay as you go system, and because that automatic withholding mechanism is gone entirely when you freelance, you are expected to withhold from yourself throughout the year. If you expect to owe $1,000 or more in federal tax, quarterly estimated payments are required.

To calculate your quarterly amounts, you can use Form 1040-ES, which walks through the estimation math and includes payment vouchers. Then you send the actual payment at irs.gov/payments through IRS Direct Pay, free, five minutes, confirmation number delivered immediately.

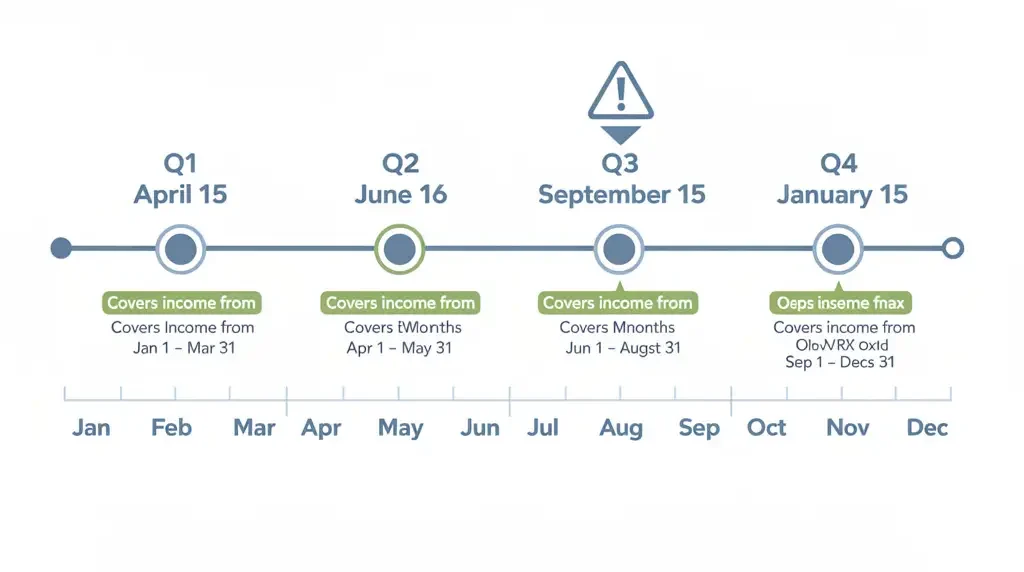

The 2026 deadlines are April 15 for Q1, June 16 for Q2, September 15 for Q3, and January 15 of 2027 for Q4. Q2 covers only two months instead of three, April 1 through May 31. The IRS has always structured it that way and it confuses everyone at least once. Put all four dates in your calendar with two-week reminders in front of each one.

For calculating how much to send, I rely on two methods depending on the year.

The Safe Harbor Rule is my default. Pay 100% of what you owed in taxes last year, split into four equal payments. Prior year tax bill was $12,000? Send $3,000 each quarter. You will not face underpayment penalties no matter what you actually earn this year. Simple, predictable, and requires almost no math.

The estimate-as-you-go approach works better in years when my income is running very differently from the prior year. Each quarter I look at real earnings, project the annual total, calculate roughly what I will owe, and send 25% of that. More precise but requires bookkeeping for independent contractors that is actually current.

My personal system is a hybrid of both. I use the safe harbor baseline to start the year, then bump up my Q3 payment if the first six months ran significantly above expectations. Keeps me protected without locking too much cash away when income is unpredictable early on.

EFTPS.gov is an alternative payment system that is slightly clunkier but preferred by people making frequent payments. Either platform works.

How Much Should You Actually Set Aside?

Everyone who starts freelancing eventually lands on this question. How much of each payment do I hold back? The real answer depends on your state, your income level, and your deductions. But that answer does not help when you are staring at your first client payment and need a number right now.

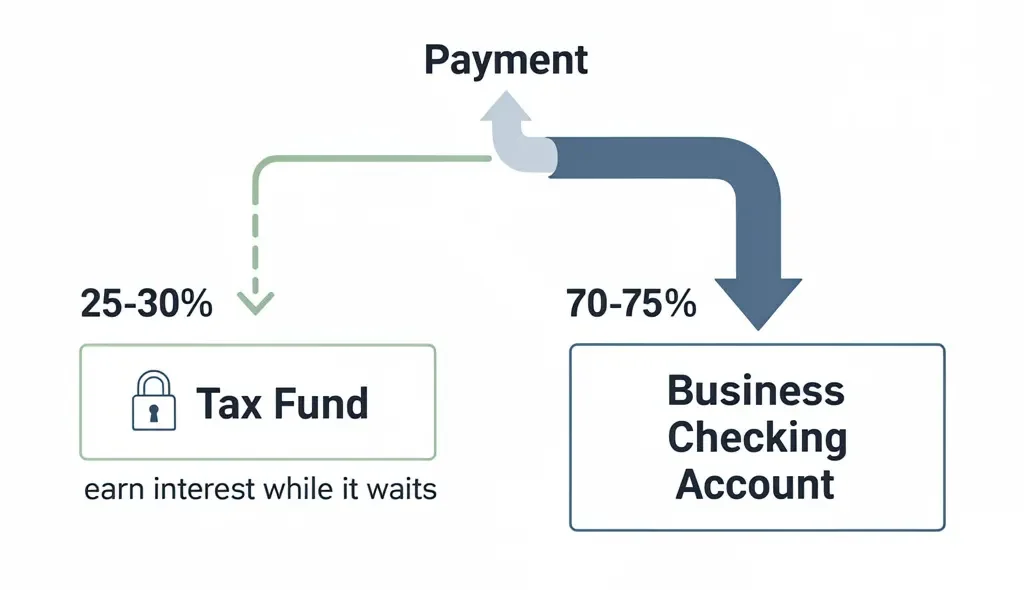

Here is the working number: 25 to 30 cents out of every dollar, moved the same day the payment arrives, into a separate account you do not touch.

The range splits based on where you live. No state income tax, think Texas, Florida, Washington, and 25% usually covers your federal and any local obligations. High-tax states like California or New York push you toward 30% or 32%. My accountant gave me that range after my first-year disaster and I have used it as my baseline ever since.

The single most important behavioral shift I made was treating that fund as money that was never mine to begin with. It is the IRS’s money sitting in my custody temporarily. The moment I stopped thinking of it as savings I was protecting and started thinking of it as a bill I was pre-paying, the anxiety around tax season almost completely disappeared.

I opened a separate high yield savings account and labeled it Tax Fund. Every payment that lands in my checking account gets a percentage transferred out the same day. I have not scrambled for tax money at filing time since.

One more thing worth doing: park that fund somewhere it earns interest. HYSA rates are currently running 4 to 5%. That money was going to the IRS eventually anyway. Might as well earn something on it while it waits.

Deductions: The Part That Actually Feels Good

Let’s get to the part that actually feels good. Deductions cut your net income, which trims both your income tax and your self-employment tax at the same time. One receipt doing two jobs worth of tax reduction. I ignored this entirely my first year and left probably $2,000 sitting on the table. Not making that mistake again.

Health Insurance Premiums

This is the most underused deduction in the freelancer tax code and the one I want to lead with. If you are not covered by a spouse’s employer plan, you can deduct 100% of your health, dental, and vision insurance premiums. Not a partial deduction. All of it. Most new freelancers paying their own premiums have no idea this exists. Claim every dollar.

Retirement Contributions

A SEP IRA or Solo 401(k) reduces your taxable income dollar for dollar. In 2026, the SEP IRA limit sits at roughly $69,000 or 25% of your net self-employment income, whichever is lower. If you have any margin at all to put money away for retirement, this is the most powerful legal tax reduction available to someone in your position.

Home Office Deduction

Any space in your home used exclusively for work qualifies, even a clearly defined corner of a room. The simplified method runs $5 per square foot up to 300 square feet, maxing at $1,500. The actual expense method requires more calculation but typically lands higher. Run both numbers before you choose which to claim.

Equipment and Tech

Your laptop, second monitor, external drive, webcam, and microphone for client calls are all deductible as business expenses. Bought a laptop that is 80% for work and 20% personal? Deduct 80% of the cost. Keep the receipt and note the business use percentage when you buy it so you are not guessing later.

Software Subscriptions

Adobe Creative Cloud, Figma, Notion, Slack, QuickBooks, Zoom Pro, Canva. If you use it for client work, it qualifies. Every qualifying write-off in this category gets claimed. I have written off Coursera subscriptions, a copywriting course, and a stack of industry books every single year. I added mine up once: $2,800 in a single year. That is a meaningful chunk of taxable income most people are just walking away from.

For a complete breakdown of every deductible expense available to self-employed people, the IRS Schedule C Instructions is the authoritative source and worth bookmarking before your first filing.

Professional Development

Courses, certifications, conference tickets, industry memberships, and books that genuinely improve your skills or keep you current in your field all qualify. If you can connect the expense to your ability to earn income as a freelancer, it is worth claiming.

Business Mileage

Driving to client meetings, a coworking space, or business-related errands counts. The 2026 IRS standard mileage rate is 72.5 cents per mile. Use MileIQ or just maintain a running note on your phone. A hundred business miles per month is $87 in deductions. Over a full year that is more than $1,000 generated from nothing but logging where you drove.

One rule applies to every single item on this list: keep documentation. Receipts, bank statements, screenshots, whatever proves the expense was real and business-related. You never mail this to anyone. But if the IRS ever audits you, you need to produce it. A Google Drive folder with monthly expense screenshots is genuinely all you need.

Tools That Make This Way Less Painful

I held onto spreadsheets for embarrassingly long. Told myself they were enough. They absolutely were not.

I eventually learned that proper bookkeeping for independent contractors means having a system that captures income and expenses automatically, estimates what you owe quarterly, and does not require three hours on a Sunday to reconstruct.

QuickBooks Self-Employed tracks income, auto-categorizes expenses, and estimates quarterly taxes. It is the all in one option I recommend to every freelancer who wants everything visible in one dashboard.

FreshBooks is what I switched to when I started managing more than three ongoing clients. The invoicing is cleaner, the expense tracking is solid, and the interface does not feel like accounting software from a decade ago.

TurboTax Self-Employed walks you through Schedule C question by question. If you want to file your own annual return without hiring a professional, this is the tool most freelancers use to get through it without losing their mind.

MileIQ runs silently in the background, auto-detects every drive, and asks you to swipe right for business or left for personal. Thirty seconds a day. That is the full workflow.

Keeper Tax uses an AI engine to scan bank transactions and flag deductions you probably missed. I was skeptical until it surfaced three recurring software subscriptions I had completely forgotten about.

YNAB (You Need a Budget) is not a tax tool. It is a budgeting app. But it fundamentally changed how I manage cash flow in a way that made quarterly payments stop feeling painful.

Under $50,000 a year and just getting started? A spreadsheet plus TurboTax Self-Employed at filing time is a real system. Plenty of experienced freelancers run it that way for years. The tool matters less than actually using it.

The Mistakes I Made (So You Don’t Have To)

Not separating my tax money immediately. Everything lived in one checking account and I spent it like it was all mine. April arrived and I had to scramble. Open a separate account today. Not this week. Today.

Skipping quarterly payments my entire first year. I genuinely did not know they existed. By the time I found out, I had already missed all four deadlines and owed a penalty on top of everything else. The penalty was not catastrophic but it was 100% avoidable.

Not tracking expenses in real time. Reconstructing 12 months of receipts from memory and bank statements in March is a genuinely miserable way to spend a weekend. Fifteen minutes every Sunday. Build that habit early and it costs you almost nothing.

Missing the home office deduction for two full years. I was convinced the deduction only applied if you had an entire dedicated room. You do not. A clearly defined workspace used exclusively for business qualifies. I left real money behind because I misread one rule.

Treating every invoice as take-home pay. I would send a $5,000 invoice and mentally start spending $5,000. After taxes, software, and other expenses, the number actually landing in my pocket was closer to $3,200. Keeping clean books fixed this within the first month I started using them.

Waiting until things got scary to deal with it at all. Tax anxiety is real and I am not dismissing it. But every week I put it off, the number in my head grew larger than the actual number ever turned out to be. The earlier in the year you get organized, the more legal options you have for reducing what you owe.

When Should You Hire an Accountant?

Not everyone needs one. If your freelance income is relatively straightforward, one type of work, predictable expenses, no employees, TurboTax Self-Employed or H&R Block’s self-employed version can handle your return without professional help. I filed my own taxes for three years before my situation got complicated enough to warrant hiring someone.

But certain situations make a CPA worth every dollar of the $200 to $500 fee. If your income jumped significantly this year, if you added a home office, if you bought major equipment, if you have income from more than one source, or if you are considering forming a business entity, get a CPA for at least year one. They almost always save you more than they charge and teach you things that reduce your bill in every year that follows.

When you go looking, find someone who specifically works with freelancers and self-employed people. General tax preparers frequently miss Schedule C nuances that cost you money. Enrolled agents (EAs) are another option worth knowing about. They are federally licensed tax practitioners who specialize in IRS matters and often charge less than CPAs while carrying equal depth of knowledge on tax law. The AICPA’s Find a CPA directory is a reliable starting point for either type.

You’ve Got This

The first time I filed taxes as a freelancer, I genuinely felt like I was navigating a system built for someone else entirely. And honestly, it kind of is. The US tax code was designed around W-2 employees. Self employed people have to do a little more work to find where they fit inside it.

But once the basic mechanics click, and they do eventually click, it stops being this looming thing you avoid thinking about. It becomes another quarterly item on the calendar. Send the payment, log the expense, move on.

The people who panic every April are almost always the ones who did not build the habit earlier in the year. Set aside 25 to 30% from the very first payment. Pay your quarters on time. Track expenses every week. Use a tool that actually fits how you work.

I sat across from an accountant with a $9,400 bill and $1,800 saved. She told me exactly what I just told you. I have done it every year since. It works.

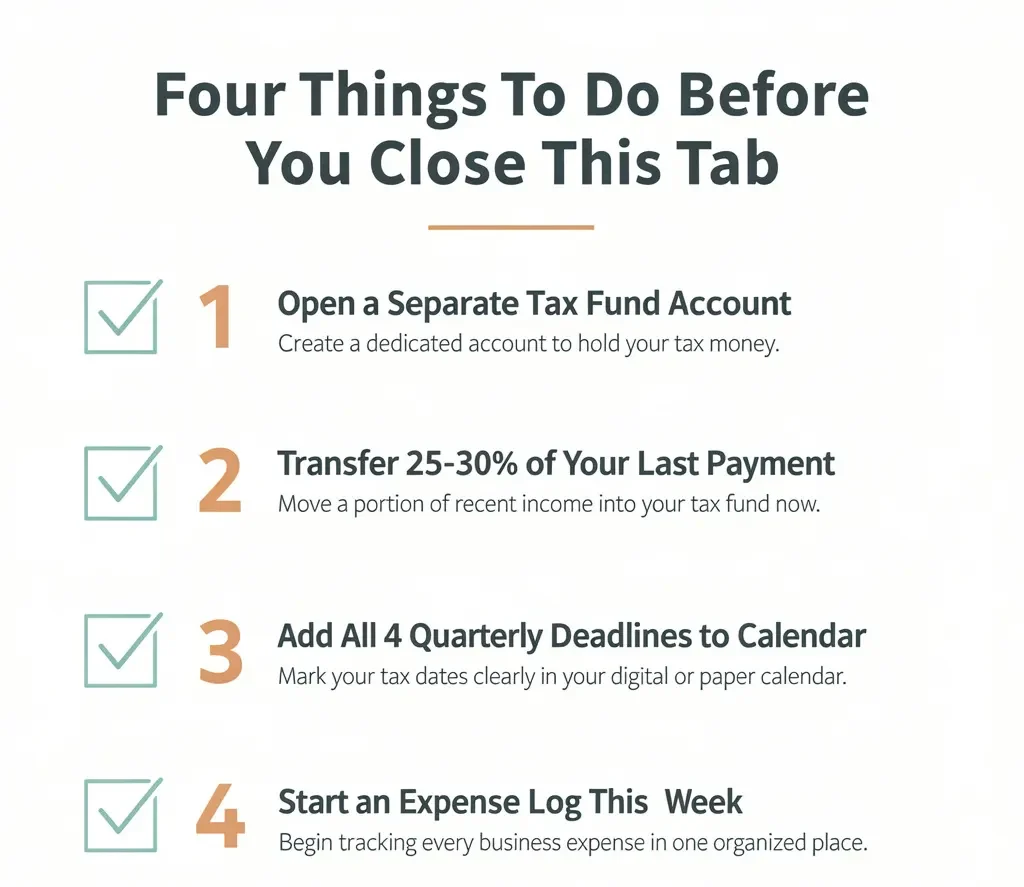

The four things to do before you close this tab:

1. Open a separate savings account today and label it Tax Fund. Do this before anything else. It is the highest-leverage single action in this entire article.

2. Transfer 25 to 30% of your most recent payment into it right now. Not at the end of the month. Right now. Build the reflex from the very first transfer.

3. Add all four quarterly due dates to your calendar with two-week advance reminders. April 15, June 16, September 15, and January 15 of next year. Set them tonight.

4. Start an expense log this week. A note on your phone, a spreadsheet, a folder in Google Drive. The format does not matter. Logging in real time does.

Frequently Asked Questions About Freelancer Taxes for Beginners

Q: Do I have to pay taxes if I only made a small amount freelancing?

Yes, if your net self-employment income was $400 or more in a calendar year, you are required to file a federal tax return and pay self-employment tax on those earnings. This threshold applies even if freelancing is a side hustle alongside a regular job.

Q: What is the self-employment tax rate in 2026?

The self-employment tax rate is 15.3%. It breaks down into 12.4% for Social Security and 2.9% for Medicare. The Social Security portion only applies to the first $168,600 of net earnings. Above that amount you only pay the 2.9% Medicare rate.

Q: How do I pay quarterly taxes as a freelancer?

Go to irs.gov/payments and use IRS Direct Pay. It is free, takes about five minutes, and gives you an immediate confirmation number. You can also use EFTPS.gov. Use Form 1040-ES to calculate your estimated payment amount each quarter.

Q: Do I need to pay quarterly taxes in my very first year of freelancing?

Yes, if you expect to owe $1,000 or more in federal taxes for the year, quarterly estimated payments are required even in your first year. Many first-year freelancers miss this and receive an underpayment penalty when they file their annual return.

Q: Can I deduct my laptop and phone as a freelancer?

Yes, if you use them for work. If the device is used for both personal and professional purposes, you deduct the percentage that represents actual business use. A laptop used 80% for client work? Deduct 80% of the purchase price. Keep the receipt and document the usage split when you buy it.

Q: What is Schedule C and does every freelancer need to file it?

Schedule C is the IRS form where self-employed people report business income and subtract business expenses. If you earned any income as a freelancer or independent contractor, yes, you file Schedule C as part of your annual Form 1040. It is the core of your freelance tax return.

Q: What happens if I skip quarterly estimated tax payments?

You will owe an underpayment penalty when you file your annual return. The penalty rate is calculated on the amount you should have paid and how long it went unpaid. It is not catastrophic but it is avoidable with four payments a year and completely unnecessary to pay.

Q: How do I know what tax bracket I am in as a freelancer?

Your federal income tax bracket is determined by your total taxable income after deductions, not your gross freelance revenue. For 2026, single filers pay 10% on the first $11,600, 12% up to $47,150, and 22% up to $100,525. Most freelancers earning between $40,000 and $80,000 in net income will find the bulk of their earnings taxed at the 22% rate.

Q: What is the difference between a 1099-NEC and a 1099-K?

A 1099-NEC is sent by clients who paid you $600 or more directly during the year. A 1099-K comes from payment platforms like PayPal, Venmo, or Upwork when your total transactions through that platform exceed the IRS threshold. Both report income you are required to claim on Schedule C. You may receive both for the same income if a client paid you through a platform, so always reconcile carefully to avoid double-reporting.

Q: Is it worth hiring a CPA as a beginner freelancer?

For a simple first year with one type of income and basic expenses, TurboTax Self-Employed is genuinely enough. But if your income was higher than expected, you have multiple income sources, you added a home office, or you are thinking about forming an LLC, a CPA for year one is almost always worth the $200 to $500 fee. They save you more than they cost and teach you things that reduce your tax bill for years after.

If you’re looking for more real world insights and practical tips to level up your freelancing journey, make sure to check out our website. We regularly share simple, actionable content to help you land better clients, protect your time, and confidently grow your freelance career.

{kind=link}